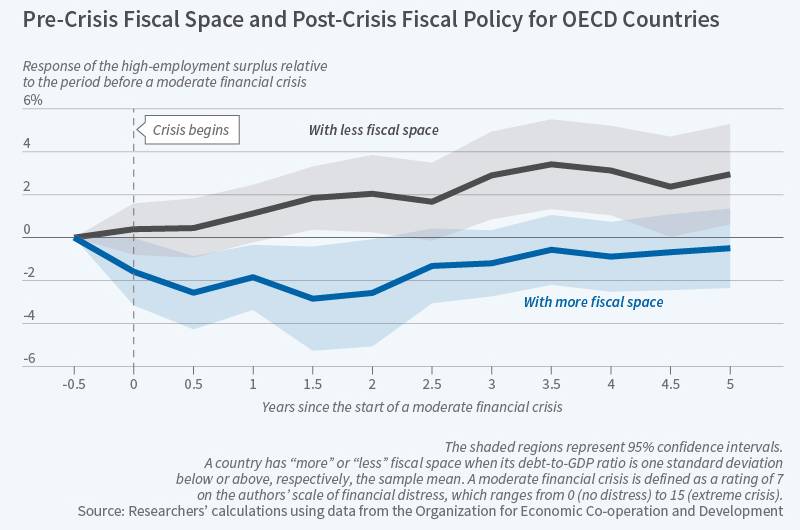

“Over the last four decades, OECD nations with lower debt-to-GDP ratios have responded to financial crises, on average, with more expansionary fiscal policy than their higher-debt counterparts. Recoveries from the crises were also faster, and the lost economic output was smaller, in the nations with lower debt-to-GDP ratios.” (Anna Louie Sussman, NBER Digest, July 2019)

In an excellent analysis of this issue, Christina D. Romer and David H. Romer recently assessed why a country’s debt-to GDP ratio is such a strong predictor of its ability to access fiscal policy in an economic crisis. (NBER Working Paper No. 25768)

In a nutshell, the authors confirmed what the financial markets have always understood, that a government’s ability to access the global sovereign debt market can be limited if the debt-to-GDP ratio is perceived as being too high.

The debt-to-GDP ratio compares a country's sovereign debt to its total economic output for the year. Since the ratio links what a country owes with what it produces, the debt-to-GDP ratio roughly indicates its ability to pay back its debts. In 2017, for example, the U.S. debt-to-GDP ratio was 103%.

While this indicator is not a perfect measure of country risk, it does indicate the relative flexibility a country has with respect to its economic management.

For example, as we note below, Japan seems to have the highest debt-to- GDP ratio among the 36 OECD countries, but Japan has no problem servicing its debt.

Italy, on the other hand, which also has an extremely high debt-to-GDP ratio, has problems servicing its debt

The importance of this indicator is obvious. Rational lenders view the ratio as a measure of default risk and usually charge higher interest rates to compensate for any increased risk.

Embattled governments facing tough economic and fiscal circumstances are constrained in their ability to create even more debt (which ultimately must be repaid) and thus are limited in using increased government spending or reduced taxes to spur their weakened economies.

The Romer’s study examined the data relating to financial distress of 30 OECD countries. Their survey covered debt ratios and market access as reflected in interest rate charges, sovereign credit default spreads, and credit agency ratings. Their findings roughly replicated the financial markets understanding of what is really going on.

There is little question that market access to sovereign debt is constrained by high debt-to-GDP ratios. As the following chart extracted from the NBER Digest illustrates, when a financial crisis hits, countries with a high debt-to-GDP ratio are less likely to pursue offsetting expansionary fiscal measure.

(Click on image to enlarge)

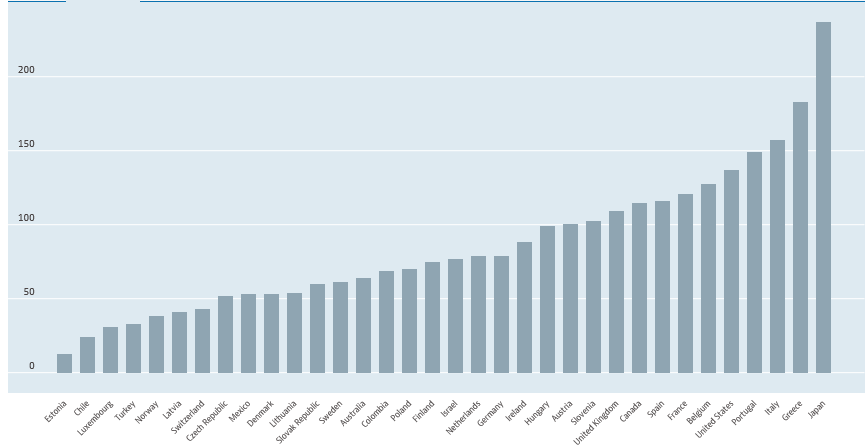

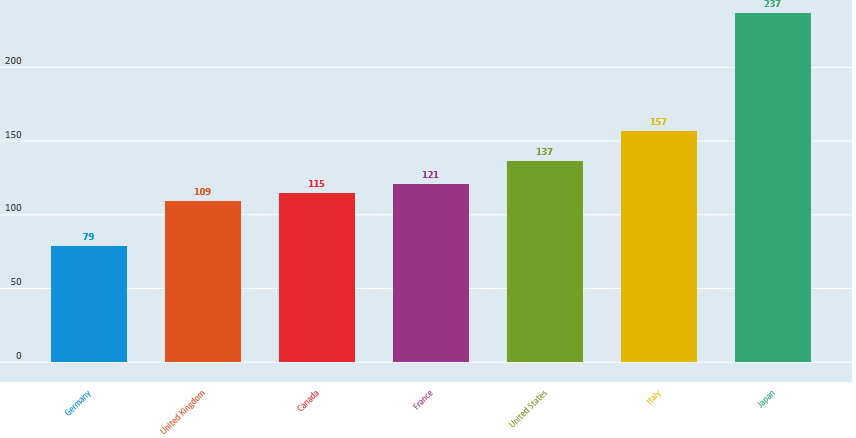

The first chart below compares the debt-to GDP ratios within the G7 group of industrial nations. The next chart broadens the comparison to the 36 OECD countries.

Within the G7 country grouping, Germany is best positioned to withstand and offset an economic crisis because of its extremely low debt ratio. The UK, Canada, France, and the US all have similar debt ratios, under 150% of GDP.

Italy and Japan are clear outliers, though Japan, with the highest debt to GDP ratio has no problem of financing its debt since its mostly internal. Italy is another question, and in that country’s financial problems are clearly worrying the financial markets.

Finally, across the entire 36 OECD nations, Japan, Greece, Portuagal are on the very high side of the debt pyramid.

The General Government Debt-To-GDP Ratio, OECD Countries

(Click on image to enlarge)

The General Government Debt-To-GDP Ratio, G7 Countries

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.