(Photo Credit: Don McCullough)

Tuesday, November 3

![]()

![]()

Wednesday, November 4

![]()

Thursday, November 5

![]()

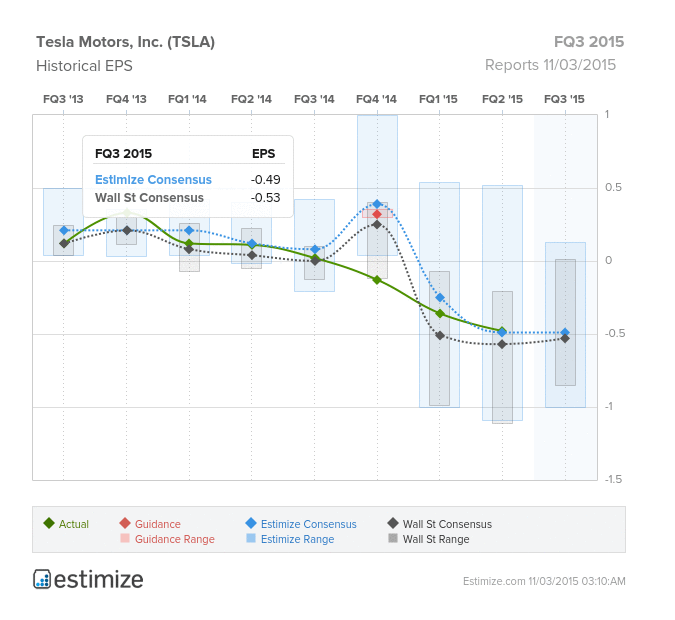

Tesla (TSLA)

Consumer Discretionary - Automobiles | Reports November 3, after the close.

The Estimize consensus calls for EPS of -$0.49, the fourth straight quarter without profitability, but still 4 cents higher than the Wall Street consensus. Revenues are anticipated to come in at $1.233B vs. Wall Street’s $1.214, what would be a 33% increase YoY.

What to watch: Tesla stock took a big hit last quarter after they lowered the number of vehicles it plans to deliver in 2015 to 50,000-55,000 from 55,000. Updates are expected for three models: the Model S, Model X and Model 3. The Model S, which recently became the best selling electric car in the U.S., debuted its latest version, the Model S 70, for $30k less than the original. The Model X, Tesla’s first full size SUV, was released a little over a month ago. The company has poured a lot of money into its production and investors will want to see that sales of the Model X are offsetting those costs. Lastly, the Model 3 will be Tesla’s most cost effective model yet starting at $35k. The company said they will start taking orders in March, we’ll be looking to see if they can stick to that timeline. Beyond its vehicles, Tesla will need to provide an update on its battery segment. The company has been hard at work assembling its gigafactory outside of Reno, Nevada which should produce cheaper batteries, set to be fully operational in 2016. The state of Powerpack and Powerwall, the company’s stationary batteries, is also expected to be addressed. Lastly, China will remain a large focus for the automaker. Weak sales have prompted talks about moving a manufacturing facility to the region, as China is a key market for luxury cars. Tesla’s stock has been all over the place this year, currently down 7% YTD. Any good news out of tomorrow’s report could have a big positive impact for the stock.

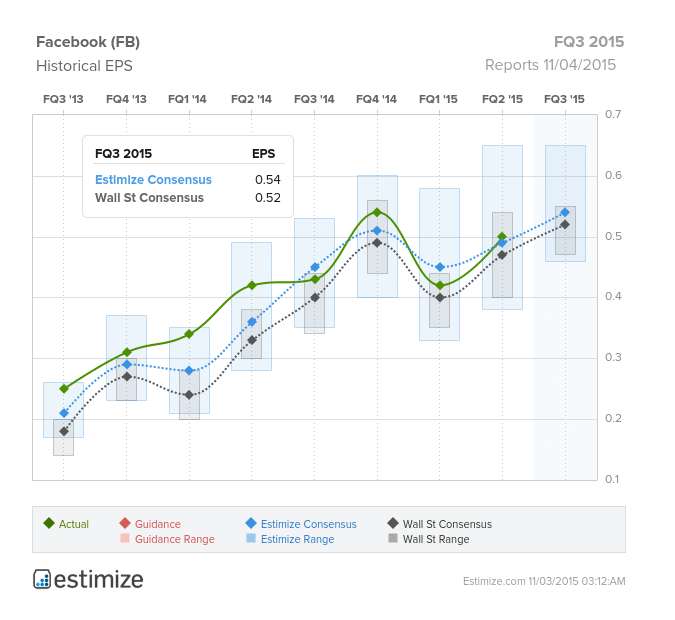

Facebook (FB)

Information Technology - Internet Software & Services | Reports November 4, after the close.

The Estimize consensus calls for EPS of $0.54, two cents higher than the Wall Street estimate. Revenues of $4.402B are also slightly higher than the Street’s $4.387B.

What to Watch: Facebook has quickly become one of the most followed stocks on the Estimize platform, garnering over 300 estimates at this point. While it’s important to take EPS and revenues into consideration, the most telling metrics for FB are those that measure user growth and engagement. In the second quarter, the social media darling posted Monthly Active Users (MAUs) of 1.49B, an increase of 13% over Q1 and well ahead of competitors such as Twitter which only has 320M MAUs and LinkedIn with 400M members. Daily Active User (DAU) growth is actually outpacing MAUs with 17% growth in Q2, a good sign that users are on the platform more frequently. Other important things to watch this quarter will be international expansion, especially into India which has huge growth opportunities. Approximately 130 million people in India use Facebook, second to only to the US. Despite expanding geographically, the average revenue per user is lower in these regions. Investors will also want updated on increased spending in the third quarter, with Facebook investing heavily in their mobile businesses such as WhatsApp and Instagram, as well as the Oculus virtual reality business. The stock topped the $100 mark for the first time on Friday, October 23, and is up 30% YTD.

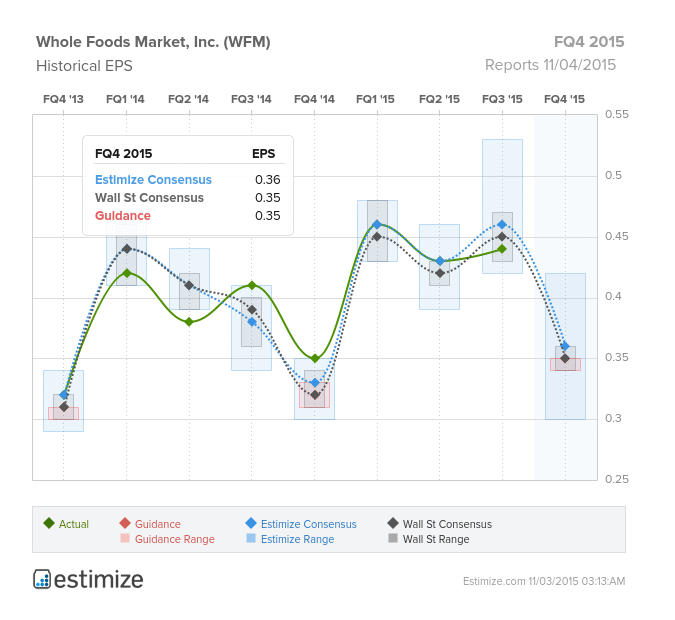

Whole Foods (WFM)

Consumer Staples - Food & Stapling Retailing | Reports November 4, after the close.

The Estimize consensus for WFM stands at $0.36, one penny higher than the Wall Street consensus. Revenues are in-line at $3.5B.

What to watch: It’s been a rough year for Whole Foods, missing or meeting on earnings revenues every quarter this year, seeing the value of its stock fall by nearly 40% and receiving some bad publicity to top it off. Same store sales, one of the most important metrics to consider with the retailers, came in at a measly 1.3% in FQ3 2015, less than half of what analysts were expecting. That miss was partially blamed on an audit gone wrong in New York City. Whole Foods locations in Manhattan were audited earlier this year, the results of which found the supermarket consistently overcharged for prepackaged foods. Despite the backlash, the company maintained guidance for 9% revenue growth in fiscal 2015, paired with SSS in the low single digits. In hopes of shedding it’s “Whole Paycheck” title, the company will be launching a value-focused chain under the name of its “365” store brand. This is in an attempt to stay competitive with other brands such as Wal-Mart, Kroger and Target which are starting to offer organic items at more competitive prices.

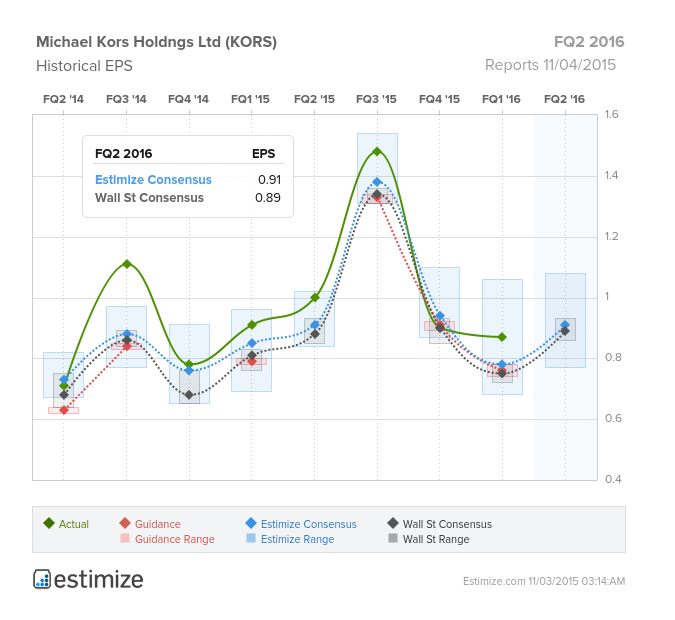

Michael Kors (KORS)

Consumer Discretionary - Textiles, Apparel & Luxury Goods | Reports November 4, before the open.

The Estimize consensus is expecting EPS of $0.92 as compared to Wall Street’s expectation for $0.89. Revenues are just slightly higher at $1.080B vs. Wall Street’s $1.073B.

What to watch: Michael Kors has seen profit growth slow as of late, even turning negative last quarter. There are a slew of reasons for this, starting with the failure of their lower-end brand which has been limiting the cache of the Michael Kors label, and making the brand too accessible. The company’s watch business, at one point its fastest growing segment, has quickly turned into a sore spot . Add to that foreign exchange headwinds and a slowdown in North American traffic, both which have all been detrimental to Michael Kors’ underlying business. The company’s store count experienced an explosion of growth from 2013 where its products were available in close to 2,913 stores globally compared to today’s figure of over 4,133 locations. Although more stores typically results in increased revenues, it can harm the brand and cause long term problems as growth slows, which is what is currently happening. In an effort to reach more customers, KORS has invested heavily in its men’s segment as well as its ecommerce platform. The company still has an advocate in well-known investor, David Einhorn, who believes the fall product line is very strong and should be enough to drive results going forward. Even so, KORS stock price has collapsed by almost 50% YTD.

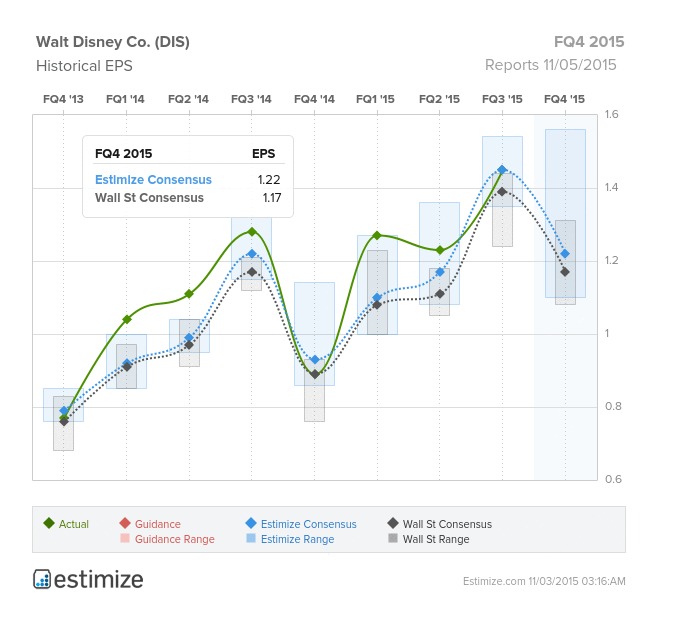

Walt Disney Co. (DIS)

Consumer Discretionary - Media | Reports November 5, after the close.

The Estimize community expects EPS of $1.22, a nickel above the Wall Street consensus. Revenues are also higher at $13.617B as compared with the Street’s $13.561B.

What to watch: Parks and Resorts continue to be one of Disney’s fastest growing segments, with earnings up 20% in fiscal Q1, but dropping to 6% and 4% in the following two quarters. Parks are doing well domestically, as consumers allocate more to travel and leisure. Tokyo Disney continues to report a record number of visitors, but analysts suspect Shanghai Disney will be the most popular yet, but expenses from the project will hit the bottom-line in the meantime. Studio Entertainment is anticipated to post robust sales as well, already crossing the $4B mark at this point of the year, and expecting a very healthy FQ1 2016 due to the release of the highly anticipated Star Wars: Episode VII The Force Awakens. The same can’t be said about the media side, due to higher programming and production costs. Cash cow, ESPN has found difficulty competing in the current Pay TV landscape, leading to a drop in subscriptions and the need for company-wide layoffs.

Comments

Log in or sign up to join the conversation.