(Photo Credit: Sergio Uceda)

Monday, December 14

Wednesday, December 16

Friday, December 18

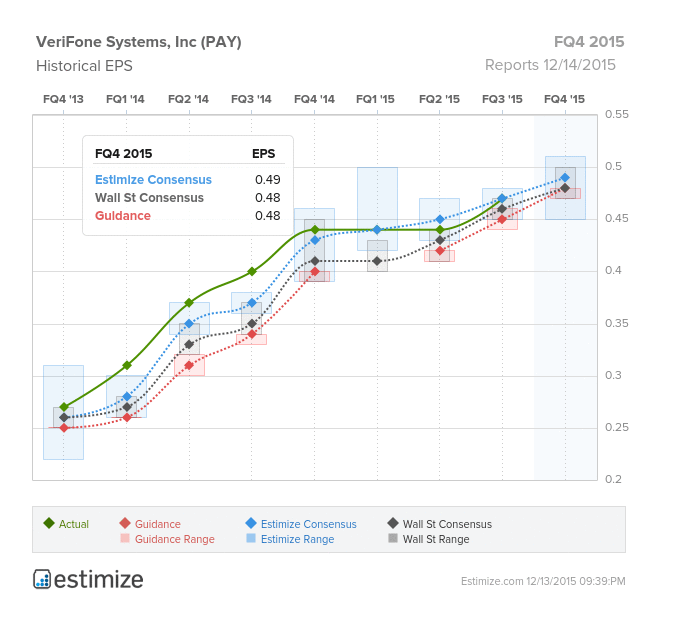

VeriFone Systems (PAY)

Information Technology - IT Services | Reports December 14, after the close.

The Estimize consensus calls for EPS of $0.49, just a penny higher than Wall Street and company issued guidance. The Estimize community is looking for sales of $516.9M, above the Street’s estimate for $513.4M and guidance of $511.5M.

What to watch: Verifone is the maker of electronic payment terminals, including Europay, Mastercard, Visa (EMV) systems which accept credit cards with chips. As of October 1, merchants using non-EMV compliant terminals began assuming liability for fraudulent transactions, a liability previously held by the credit card companies. The shift in this liability should be profitable for Verifone as merchants scramble to update their payment terminals (at last read in 2014, the percentage of EMV enabled devices only reached 27%). Gas stations get a two year extension, however. None of the more than 1 million gas stations in the US have EMV capable devices at this point, due to the high cost of updating self-service gas pumps. Also worth watching on Monday is progress in Near Field Communication (NFC) technology, which allows electronic devices to exchange radio communication with each other when brought into close proximity – technology used with such apps as Apple Pay, Android Pay and Google Wallet.

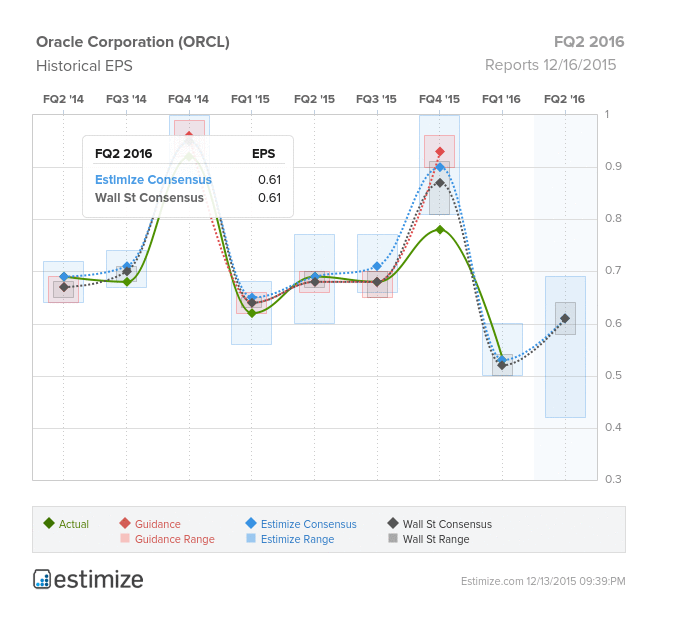

Oracle (ORCL)

Information Technology - Software | Reports December 16, after the close.

The Estimize consensus calls for EPS of $0.61, in-line with Wall Street. Revenue estimates are also quite close, with the Estimize community calling for $9.113B and the Street slightly lower at $9.094B.

What to watch: Cloud competitors have their eyes on Oracle as the company continues to rapidly build out its SaaS and PaaS product offerings. To put this in perspective, Oracle’s human capital management (HCM) SaaS product secured three times as many new customers as competitor Workday’s similar HCM product. This focus on the cloud has led Oracle to expect approximately $1.5-$2 billion in new SaaS and PaaS purchases this year alone. Oracle’s SaaS and PaaS revenues experienced a 54% increase last quarter as a result of the shift of 95% of its services to the cloud. While the cloud has been gaining traction, it hasn’t been enough to offset weakness in Oracle’s bread and butter software licensing division, which dropped 16% last quarter. For that reason, Oracle has not been able to beat analyst estimates on the bottom-line for the past eight quarters, missing in five of those quarters and meeting in the other three. Revenues have been even worse, missing expectations in six of the past eight quarters. Year-to-date the stock has dropped nearly 15%.

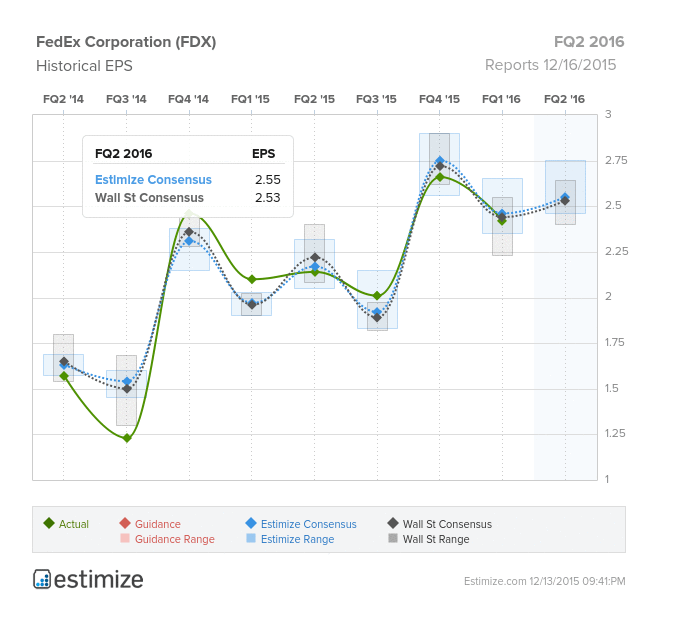

FedEx (FDX)

Industrials - Air Freight & Logistics | Reports December 16, before the open.

The Estimize consensus calls for EPS of $2.55, two cents above the Wall Street consensus. Revenues are a little more muted, with Estimize looking for $12.447B, only $12M above the Street’s expectation.

What to watch: This year has not been kind to FedEx and other transport names. While it was initially thought that the decline in oil prices last year would give the transports a boost, lower fuel surcharges have instead hurt them. Adding to this is the fact that FedEx is seeing lower package weights, a fall in demand for higher-end services and decreased international revenue per package due to currency headwinds. However, the holiday shopping season is upon us, and next week’s report will reflect how FedEx did through Cyber Monday (November 30). The company has already forecast a record number of shipments between Black Friday and Christmas Eve thanks to a consumer shift toward e-commerce shopping. FedEx is prepared for the increased shipping volume and has bulked up with 325,000 team members to help deliver. A move to dimensional weight pricing at the beginning of the year should help to inflate profits this season, something that previously only applied to packages greater than three feet. If shippers decide to right-size their packaging, FedEx will be able to take more packages per trip, if shippers do not adapt and continue to use boxes that are too large, they will just have to pay up for it. Either way, FedEx wins.

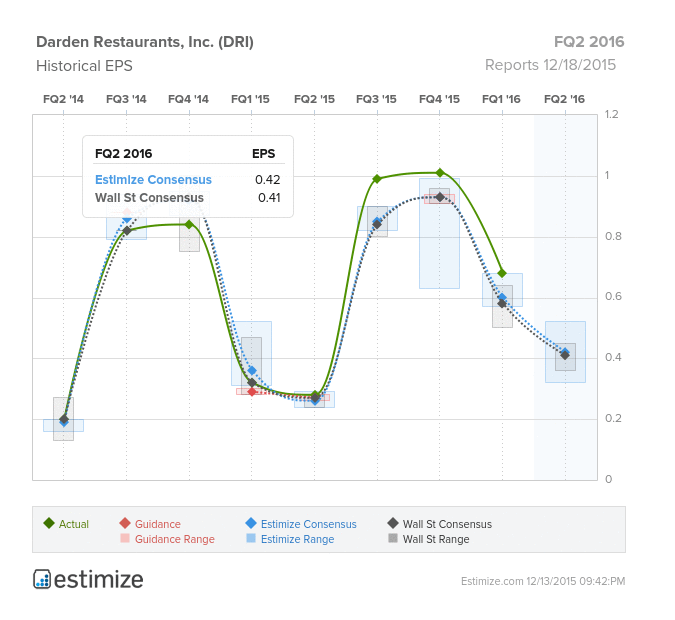

Darden Restaurants (DRI)

Consumer Discretionary - Hotels, Restaurants & Leisure | Reports December 18, before the open.

The Estimize consensus calls for EPS of $0.42, one cent above the Wall Street consensus. Revenues of $1.628B are slightly above the Street’s expectation for $1.625B.

What to watch: The consumer appetite for casual dining has given a much needed lift to Darden Restaurants. Over the past four quarters the restaurant operator has seen EPS results surprise analyst estimates by an average of 11.5%, leading to double-digit, and even triple-digit growth in the latest quarter. This comes after three consecutive quarters (FQ3 2014 - FQ1 2015) of earnings misses and negative growth which can be mostly tied to Darden’s struggling Red Lobster franchise which was shed in July 2014. Despite recent success, revenues over the last four quarters have been rather muted, beating by a much narrower margin of 0.3%. The main reason for selling Red Lobster last year was so that Darden could focus on its Olive Garden business, a move that seems to be mildly paying off. While Olive Garden has the company’s highest volume of traffic, growth figures are lagging behind other Darden-owned restaurants. In the latest quarter, same store sales for the Olive Garden came in at 2.7%, below the overall company increase of 3.4%, and behind other restaurants such as The Capital Grille (7.2%) and LongHorn Steakhouse (4.4%). There are also concerns around stagnating traffic patterns at Olive Garden, which only increased 0.3% in FQ1 2016. The stock is down around 2% year-to-date, but up nearly 30% since the completion of the Red Lobster sale.

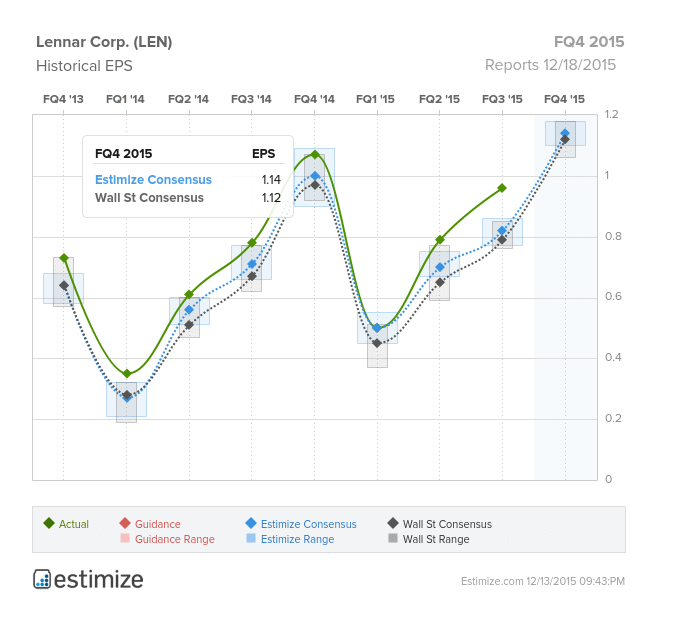

Lennar (LEN)

Consumer Discretionary - Household Durables | Reports December 18, before the open.

The Estimize consensus calls for EPS of $1.14, two cents above the Wall Street consensus. Revenues of $3.02B are slightly above the Street’s expectation for $2.99M.

What to watch: Next week we get a read on the health of US consumers and their willingness to purchase large ticket items such as homes when Lennar releases its Q4 report. After posting strong numbers throughout the summer, housing metrics came in mixed this fall. After plummeting in September due to lack of supply, New Home Sales made a bit of a recovery in October, yet still missed analyst estimates. Housing Starts on the other hand were strong in September, but fell in October as a result of a big drop in multi-family homes. The bright spot of that report, however, was that Permits were up 4.1%, pointing to strength for near-term construction. Unlike other more regionally focused homebuilders, Lennar operates all over the US and will feel the pinch of lower home sales in the Northeast. However, unseasonably warm weather in that region, as well as in the Midwest, should be a boon for construction, with the expectation for a mild winter, as well. The homebuilder reported robust results throughout 2015 and believes 2016 will be just as promising.

Comments

Log in or sign up to join the conversation.