Looking ahead to this week, we have an incredibly important week with respect to earnings reports. Throughout the course of the week, investors will be updated by some of the biggest names in the banking industry.

Reports for Tuesday, July 14

![]()

Report for Wednesday, July 15

![]()

Reports for Thursday, July 16

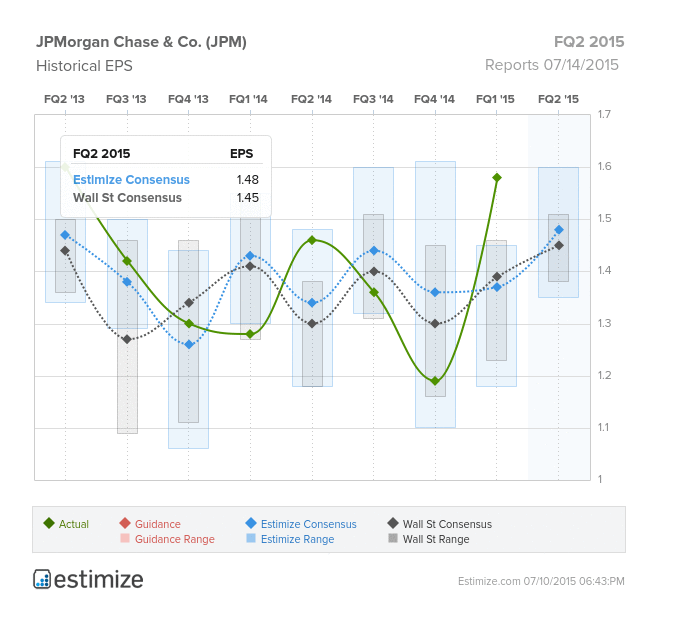

JP Morgan (JPM)

JP Morgan (JPM) reports its FQ2 ’15 results before the opening bell on Tuesday. The Estimize EPS consensus is set at $1.47, 2 cents higher than Wall Street’s expectations. Revenue expectations of $24.6B also surpass the Street’s expectations marginally. These numbers would put both JPMorgan’s year-on-year (YoY) earnings and revenue growth at less than 1%. The company’s stock is up 4.83% year-to-date (YTD), down from its late June high of 11.46%.

After crushing both Wall Street and the Estimize’s consensus on April 14th of this year, JP Morgan experienced a 9.3% increase in price until mid-June. Similarly, after missing expectations by a wide margin on January 14th of this year, JP Morgan experienced a price plunge of 5%. JP Morgan’s stock could fluctuate significantly if their upcoming report delivers any surprises. Make sure to pay close attention before the market opens on Tuesday as JPMorgan looks to beat expectations.

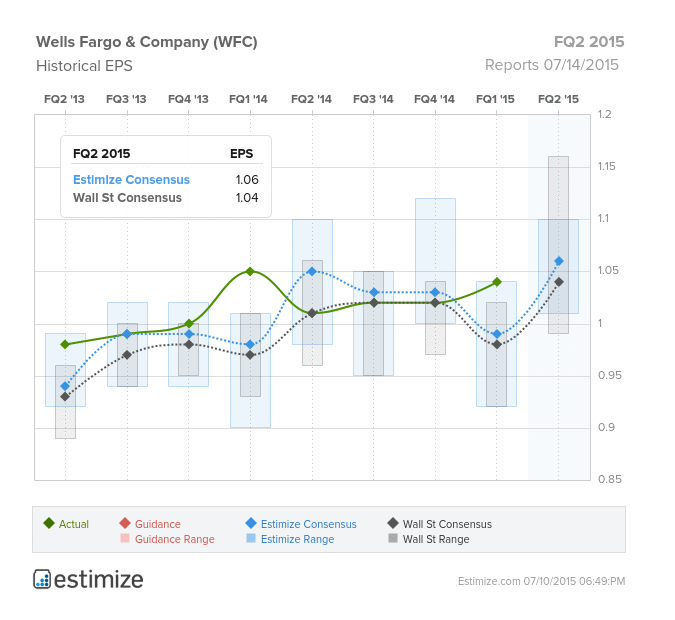

Wells Fargo (WFC)

Wells Fargo (WFC) also reports Tuesday morning when they release their FQ2 ’15 result. Estimize predicts an EPS figure of $1.06 and a revenue number of $21.719B. Wall Street analysts however, assume an EPS figure of $1.04 and forecast revenues of $21.537B.

Weak demand for mortgages has restricted Wells Fargo’s revenue growth for a considerable amount of time. However, mortgage applications have slowly been making a comeback recently and are coming off a very low base. As the property market continues to regain momentum and the demand for mortgages increase, Wells Fargo should be at the forefront to benefit financially. Wells Fargo has the second largest loan book amongst the major banks and therefore will likely expereience an uptick in revenues as demand for domestic mortgages rise.

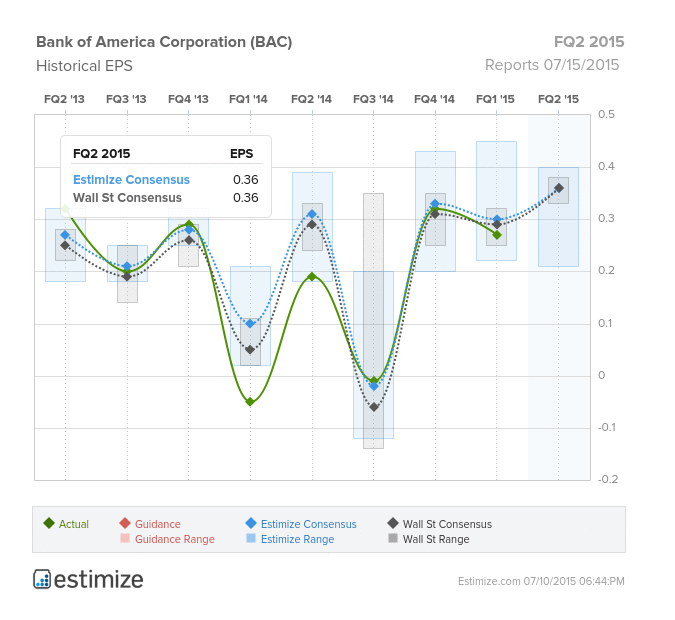

Bank of America (BAC)

Bank of America (BAC) also reports its FQ2 ’15 results this week before the opening bell on Wednesday. Both Estimize and Wall Street are predicting an uplift in EPS QoQ to reach a figure of $0.36. Estimize predicts a revenue figure of $21.475 and Wall Street forecasts $21.339.

If the Fed increases interest rates in the medium-term, as expected, then it can be assumed that Bank of America will benefit significantly due to an expected increase net revenue. This is due to Bank of America’s balance sheet, which is highly leveraged to rising interest rates and a steepening of the yield curve caused by its large mortgage book. Specifically with segment revenue performance, the Consumer Banking unit generates the highest revenuefor the bank, almost 36%.

The report from Bank of America will be one to watch carefully as investors will get a good understanding of not just the company’s performance, but also management’s outlook for interest rate moves and the overall strength of the housing sector.

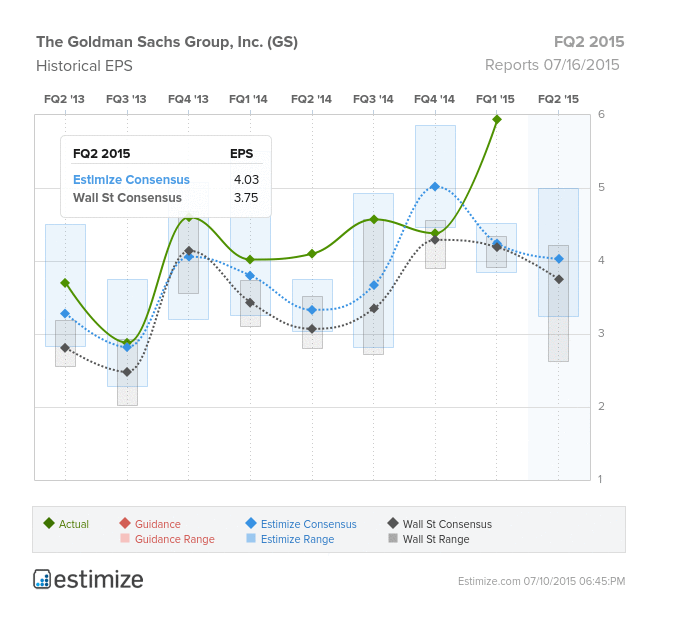

Goldman Sachs (GS)

Goldman Sachs (GS) is scheduled to report FQ2’ 15 earnings before the market opens this Thursday. The Estimize EPS estimate is set at $4.02, 27 cents higher than the Wall Street consensus of $3.75. In terms of revenue forecasts, the Estimize community forecast $9.069B compared to Wall Street which predict $8.858B.

Similar to its competitors, Goldman Sachs is expected to be negatively affected by the lack of trading volume which has taken place over the past three months. Despite having a relatively small bond-trading desk when compared to its peers, the fall in bond trading volume will still likely have a negative effect on Goldman Sachs’ revenues and earnings. Similar to previous quarterlies, investors will be interested in hearing Goldman Sachs’ management discuss their strategy to reduce volatility in earnings throughout the course of the entire business cycle.

Goldman Sachs has performed relatively well compared to its peers year-to-date recording a capital gain of 6.73%. Only JP Morgan has posted a higher return gain to shareholders (YTD).

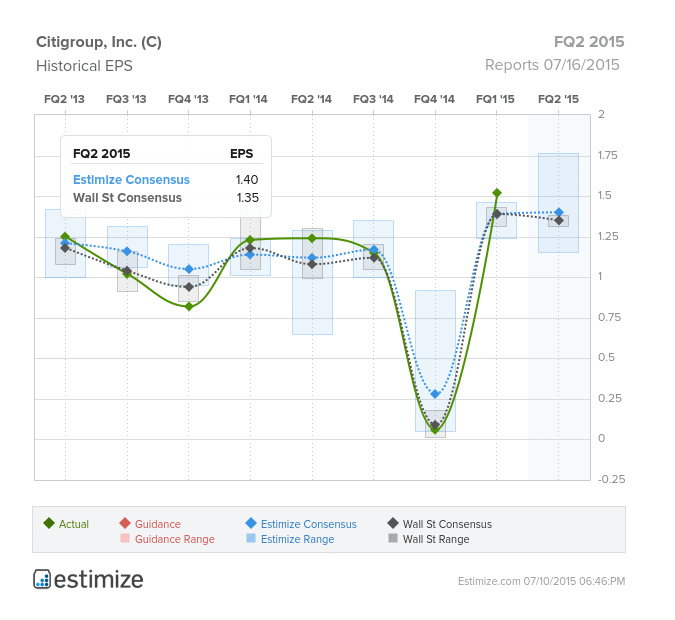

Citigroup (C)

Citigroup (C) will also report Thursday morning when they release to the market their FQ2 ’15 results. Year-to-date (YTD) Citigroup’s stock has traded sideways providing investors with a slight capital gain of 0.79% relative to the S&P 500 index which has appreciated 0.59%.

For the upcoming quarter, the Estimize community is predicting an EPS figure of $1.41 and a revenue target of $19.595B. Wall Street expects EPS coming in at $1.35 and a revenue figure of $19.161B.

A problem for Citigroup may emerge from its Institutional Business. Due to the lack of stability in global capital markets, it has been assumed that Institutional clients may have reduced their trading materially over the past quarter. This expected fall in institutional activity has led analysts to predict a potential 14% fall in QoQ revenues from Citigroup’s fixed income and equities businesses.

On a positive note, Citigroup is in the middle of a cost cutting campaign in an attempt to improve efficiency throughout the firm. Citigroup’s efficiency ratios are expected to improve this quarter and be within the upper band of 49%-52%. If achieved, Citigroup’s expenses will continue to fall relative to revenues and provide upside to earnings.

Comments

Log in or sign up to join the conversation.