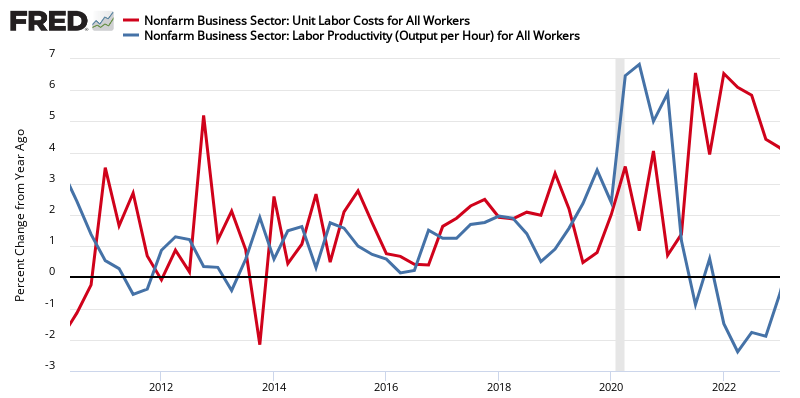

A simple summary of the headlines for this release is that labor costs are growing significantly faster than productivity.

Analyst Opinion of Productivity and Costs

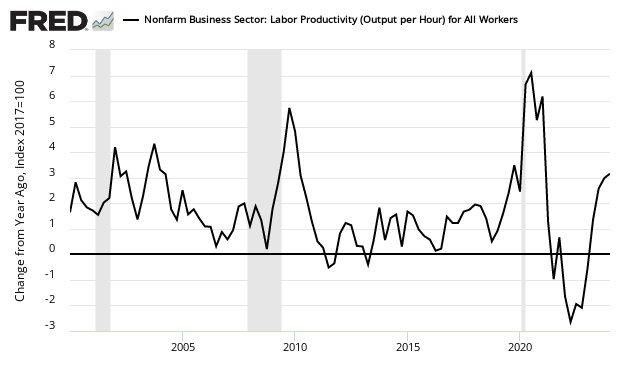

The overall view this quarter is that productivity is up 1.4 % from the same quarter one year ago (last quarter productivity was up a revised 2.3 %), while unit costs are up 3.1 % (last quarter labor costs were up a revised 2.6 %).

Consider that GDP per capita is in contraction year-over-year if one eliminates transfer payments. This down and dirty view suggests there is no productivity growth.

Note the following from the BLS:

In the second quarter of 2019, nonfarm business sector productivity increased 2.5 percent, slightly more than reported on September 5. Unit labor costs increased 2.4 percent during the second quarter, slightly less than previously reported. In the manufacturing sector, productivity was revised down 0.2 percentage point to a decrease of 2.4 percent in the second quarter of 2019. Durable manufacturing productivity decreased 0.8 percent and nondurable manufacturing productivity fell 4.3 percent after revisions. Unit labor costs in total manufacturing increased 6.9 percent in the second quarter of 2019 rather than increasing 6.7 percent as reported September 5.

The market was expecting from Econoday:

| seasonally adjusted quarter-over-quarter at an annual rate | Consensus Range | Consensus | Preliminary Actual | Final Actual |

| Nonfarm productivity | 0.1 % to 1.9 % | +1.1 % | -0.3 % | |

| Unit labor costs | 1.3 % to 2.9 % | +2.2 % | +3.6 % |

Please note that the following graphs are for a sub-group of the report nonfarm > business.

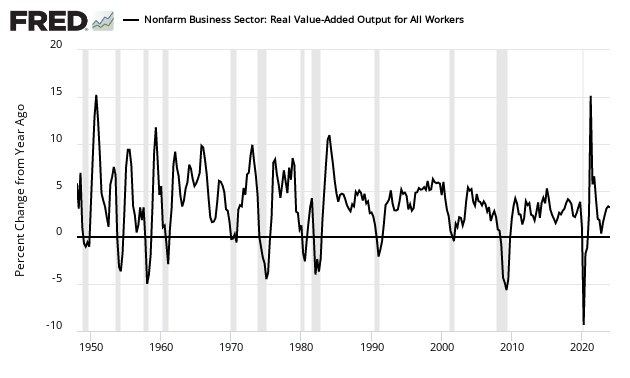

Seasonally Adjusted Year-over-Year Change in Output of Business Sector

Seasonally Adjusted Year-over-Year Change of Output per Hour for the Business Sector

All this is happening while business sector unit labor costs are growing.

Seasonally Adjusted Year-over-Year Rate of Change of Unit Labor Costs

The headlines from the press release:

Nonfarm business sector labor productivity decreased 0.3 percent in the third quarter of 2019, the U.S. Bureau of Labor Statistics reported today, as output increased 2.1 percent and hours worked increased 2.4 percent. (All quarterly percent changes in this release are seasonally adjusted annual rates.) From the third quarter of 2018 to the third quarter of 2019, productivity increased 1.4 percent, reflecting a 2.3-percent increase in output and a 0.9-percent increase in hours worked.

Final Chart for 2Q2019

Preliminary Chart for 3Q2019

My view of Productivity

My view of productivity is very different from the headline view. Productivity calculations are complicated - far too complicated for economists to come to a conclusion satisfactory to this simple Industrial Engineer:

Generally speaking, productivity is, in industrial engineering, defined as the relation of output (i.e. produced goods) to input (i.e. consumed resources) in the manufacturing transformation process.

Productivity assessments, even within a single company, are very complicated. When one goes beyond the individual company, they are impossible to accurately forecast when discussing an entire sector or economy. Industrial engineers do not use costs as a component to determine productivity. Industrial Engineers count processes and manhours - and are able to isolate improvements as elements change. So to generalize about sectors, economists have to make too many assumptions which not only make the calculations inaccurate - but their productivity conclusions jump around like a Mexican Jumping Bean.

A Better View Of Productivity

There are some rough tools that will get one into the ballpark of productivity improvement. These are monetary-based views, and likely are correct only in trends (but not in calculating an exact productivity change).

The following graphs on manufacturing, investment, retail trade, and health care are comparing inflation-adjusted growth of that sector to employment growth in that sector - as well as for the economy overall.

Economy Overall

In the case of the economy overall, for the last two years - it appears output (blue line) is now growing faster than employment.

The problem with this analysis is that it is a gross generalization - but it does estimate that we are looking for a positive productivity increase in the last year.

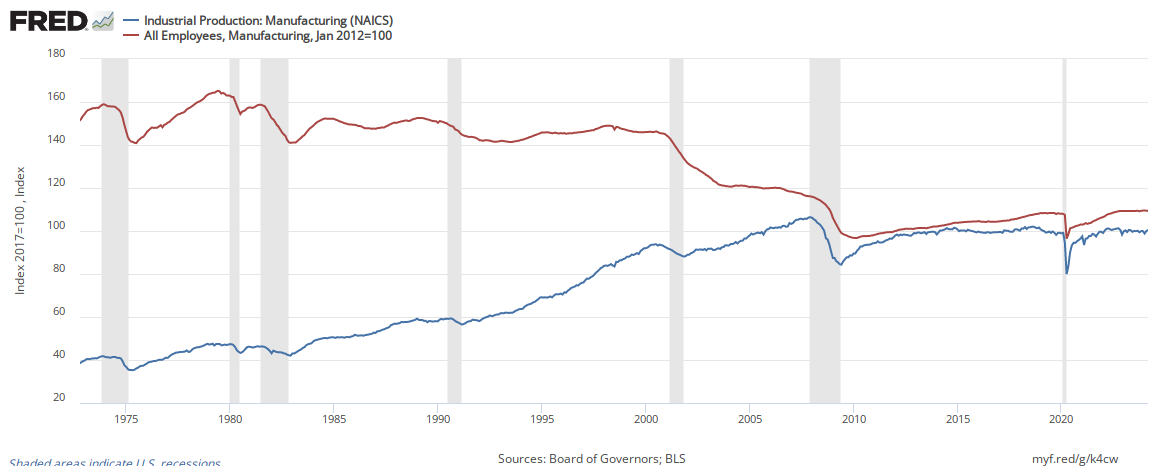

Manufacturing

In the case of manufacturing, output (blue line) is now growing slower than employment.

It should come as no surprise that manufacturing's productivity is contracting.

Construction

Since 2012, construction output and employment are also growing at nearly the same rate implying there is little productivity growth.

Services

The only significant productivity growth I can find is in the services sector.

Beginning with the retail sector, the obvious gain in productivity is seen throughout the graph below and continues today.

There also is an improvement in the health care sector.

Another Alternate View Of Productivity Removing Transfer Payments

Another way of looking at productivity is the year-over-year rate of growth of GDP normalized to employed population - red line) vs. GDP per capita (blue line). This metric is partially showing how well businesses are utilizing the labor force - and in a rough way looks at productivity growth if one eliminated government transfer payments from GDP. (see red line in the graph below):

The red line in the above graph suggests there is little overall productivity growth.

Overall Conclusion On Productivity

If you want to be entertained with a diatribe on productivity - Yves Smith carved up this subject well looking at it from an entirely different angle. In economics and life, a little knowledge [on a subject] is a dangerous thing.

This proverb 'A Little Knowledge Is A Dangerous Thing' means a person is sharing his views with others and doesn't have enough knowledge of a particular subject, especially medical, religion, or education field, it can lead to dangerous situations. People with limited experience can often mislead people. Innocent people or people with a lack of information may easily believe the person pretending to know everything because most of the time, they are very convincing. A person with a little information and knowledge can also become a cause of suffering and even death due to their overconfidence.

The problem really is that economists seem to only understand money flows - and they use money to measure productivity. Productivity is an extremely nuanced calculation which is never totally accurate as there are shifting technology and/or methods. The core of industrial engineering productivity is a measure of labor hours for a specific task Vs. the output of those labor hours - and that detailed data is not available to anyone outside of a company.

The economist's methodology of measuring productivity overstates productivity when outsourcing is increasing and understates productivity when outsourced production is returned.

Caveats Relating to Productivity

Productivity is determined using monetary criteria and does not recognize outsourced man-hours - in other words, if a business cuts half of its workforce by outsourcing a sub-component or sub-service, this would be a 50% productivity improvement.

These productivity measures describe the relationship between real output and the labor time involved in its production. They show the changes from period to period in the amount of goods and services produced per hour. Although these measures relate output to hours at work of all persons engaged in a sector, they do not measure the specific contribution of labor, capital, or any other factor of production. Rather, they reflect the joint effects of many influences, including changes in technology; capital investment; level of output; utilization of capacity, energy, and materials; the organization of production; managerial skill; and the characteristics and effort of the work force.

Econintersect believes a better measure (if you must use monetary tools to track productivity) would be competitiveness.

Looking at productivity/output long term - output fall below 0% year-over-year change is a good sign that a recession is underway. Another way to look at it - if productivity rate of gain is falling, this could be an indicator a recession is coming.

Comments

Log in or sign up to join the conversation.