Image: Bigstock

After the broader market's impressive rebound over the last two years, finding reasonably valued growth stocks has become increasingly difficult.

That makes companies benefiting from improving earnings outlooks while still trading at discounted valuations and or affordable stock prices particularly attractive.

One group that continues to offer value is the Business Services sector, where several companies have recently earned a coveted Zacks Rank #1 (Strong Buy) based on favorable earnings estimate revisions.

That said, here are three of these highly ranked and affordable business services stocks to consider now.

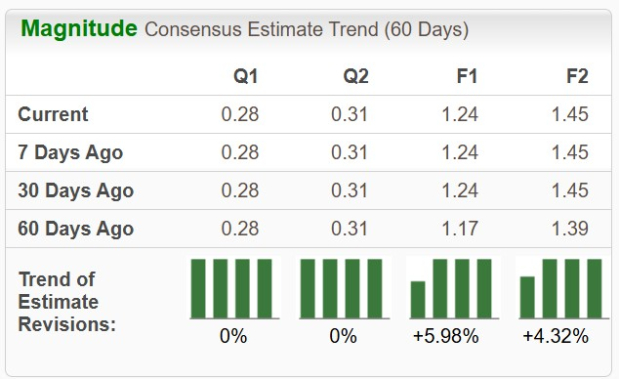

Concrete Pumping Holdings

Concrete Pumping Holdings (BBCP - Free Report) provides concrete pumping and waste management services throughout the U.S. and the U.K, operating under the well-known Brundage-Bone and Camfaud brands.

The company is benefitting from long-term infrastructure spending, commercial construction activity, and residential development while maintaining one of the largest concrete pumping fleets in North America.

Although construction activity has remained mixed due to elevated interest rates, BBCP has produced resilient operating results. Correlating with such, current-year EPS estimates have climbed more than 40% in the last 60 days, while next year's estimates have increased 30%, helping BBCP earn its strong buy rating.

From a valuation perspective, analysts expect earnings growth to accelerate substantially over the next several years, which should eventually make the stock's forward P/E multiple considerably more attractive than its elevated trailing multiple.

Image Source: Zacks Investment Research

Green Dot

Green Dot (GDOT - Free Report) has quietly transformed itself into one of the more diversified fintech companies, offering digital banking, embedded finance, prepaid debit cards, and Banking-as-a-Service (BaaS) solutions.

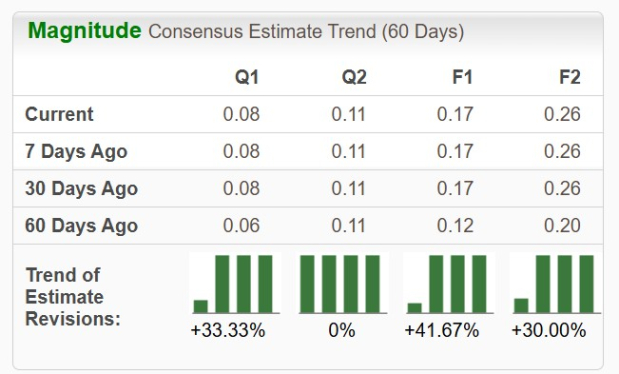

Even more encouraging is the company’s consistency. Green Dot has impressively exceeded earnings expectations for six consecutive quarters, indicating management is executing efficiently despite a challenging consumer spending environment.

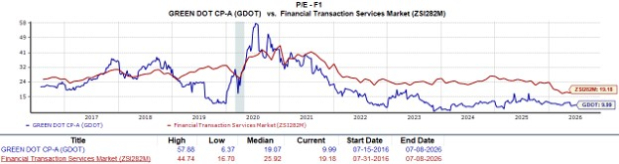

Those results have prompted analysts to lift earnings expectations, resulting in Green Dot’s strong buy rating. Unlike many fintech peers that still command premium valuations despite inconsistent profitability, Green Dot trades at an attractive forward earnings multiple of 9X.

Image Source: Zacks Investment Research

If management continues to expand its embedded finance partnerships while improving operating efficiency, GDOT could have meaningful upside from current levels.

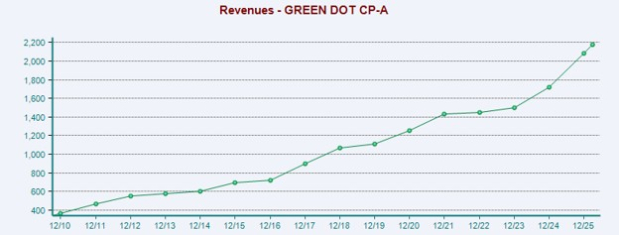

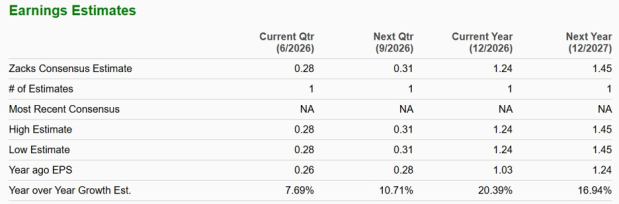

Reassuringly, Green Dot's annual revenue has surpassed $2 billion, and analysts expect full-year EPS to remain above $1.60 for the foreseeable future after posting earnings of $1.41 per share last year.

Image Source: Zacks Investment Research

Priority Technology Holdings

Priority Technology Holdings (PRTH - Free Report) has evolved into an increasingly diversified payment technology platform, providing integrated payment processing, banking, commercial payments, and embedded financial software.

Most attractive is the company’s valuation, with PRTH trading at just 5X forward earnings. Like Green Dot, Priority Technology has one of the lowest valuations among profitable fintech companies, and analysts expect double-digit EPS growth in FY26 and FY27.

Image Source: Zacks Investment Research

Meanwhile, earnings estimates have remained favorable enough to support its strong buy rating, reflecting continued confidence in management's execution.

As electronic payments start to replace cash transactions across businesses of all sizes, Priority Technology could benefit from secular industry growth while trading at a valuation that leaves plenty of room for multiple expansion.

Image Source: Zacks Investment Research

Bottom Line

While mega-cap technology companies tend to command premium valuations and very lofty stock prices, investors searching for overlooked value opportunities may find better risk-reward profiles among smaller business services companies with improving earnings outlooks.

Keeping that in mind, these highly ranked business services stocks appear well-positioned for investors looking to build positions in affordable growth names before broader market recognition catches up.

Comments

Log in or sign up to join the conversation.