Market Analysis

The USDA provided surprises in both their US acreage & corn’s quarterly stocks reports again this week. Their latest producer survey revealed sharply reduced corn, spring wheat & cotton plantings while their stocks survey found virtually all the missing corn supplies of the past 2 quarters.

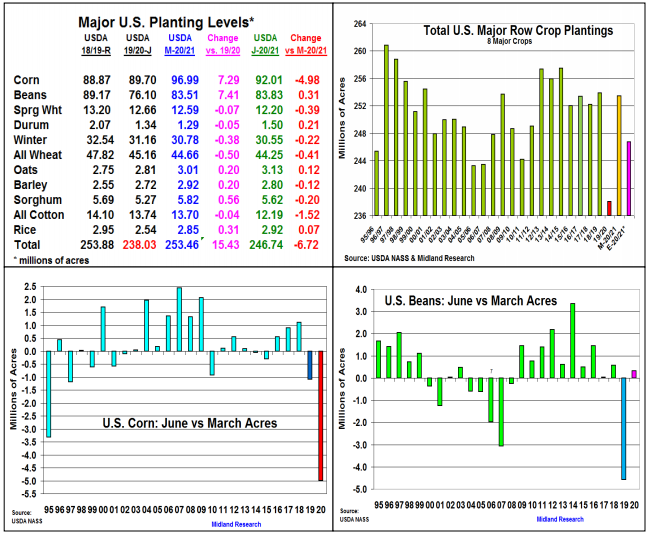

Interestingly, US farmers changed course & cut their 2020 corn planting from March’s 96.99 million intentions to 92 million acres, a 5% cut and the largest March to June decline known in the data. This reversed the 7.29 million March increase. Smaller plantings occurred virtually across the US as producers reacted to Covid-19’s impact on ethanol demand & US Plains spring soil conditions were poor. Cold & wet May conditions in ND, SD & MN slipped their plantings 1.7 million. SW dryness sliced KS & TX by 300,000 each while NE dropped 700,000 acres. The ECB also cut 1 million from their intentions as hefty rains hurt IL & IN plantings.

2020’s US soybean plantings increased from their March intentions, but only by 315,000 acres. Prevent planting revenues from corn must have been more attractive than more bean seedings given the US flair up with China over Hong Kong & the coronavirus. Spring conditions in ND & SD also sliced 800,000 bean acres from their intentions.

Overall, US seedings are still 7.73 million higher than 2019. Overall, June’s 6.7 million less US acres including 390,000 less spring wheat & 1.5 million smaller cotton plantings will be the smallest 8 major crop area since 2011/12 and the reason for the market’s strength.

The USDA’s quarterly stocks were mixed. Corn’s 5.224 billion level was 273 million higher than expected suggesting a smaller feed demand than the current 5.7 billion bu. forecast. However, heavier spring slaughter weights don’t compute with this idea. Soybean stocks at 1.386 million bu. were near the trade average. 2019/20’s wheat ending stocks were 64 million larger than expectations as cheap corn likely cut into its feed demand.

What’s Ahead:

The trade’s focus is on the US 2020 planting levels. Corn’s stocks remain a head-scratcher given our spring slaughter weights. However, corn’s pollination period is fast approaching beginning July 10 for 3-4 weeks. Given the chance for weather price volatility, utilize Sept & August strength to $3.60 & $8.90 to have 90% old-crop sold & advance new-crop hedges to 25% & 15% at $3.65 & $9.00-10.

Comments

Log in or sign up to join the conversation.