Market Analysis

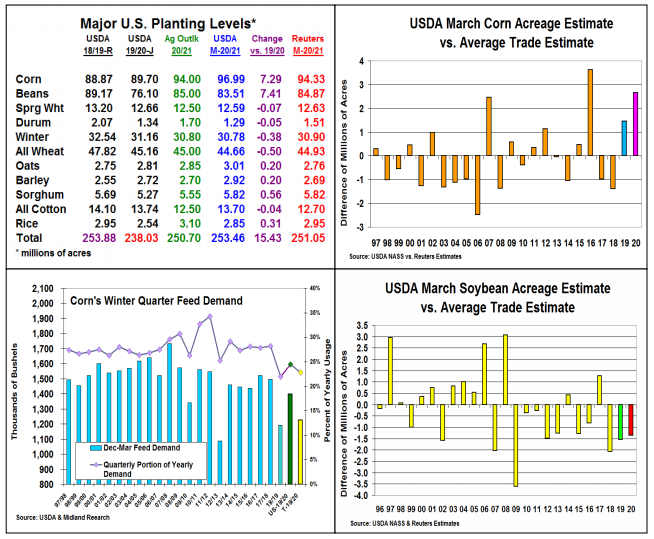

The USDA provided surprises in both US planting intentions & their quarterly stocks reports. DC’s producer survey revealed sharply higher corn plantings & smaller soybean and spring wheat seedings than the trade expectations. Interestingly, corn’s 96.99 million acres were 2.66 million above the trade & 7.29 million above 2019. Higher intentions were voiced across the Central US from Ohio to Nebraska. After hefty PP acres last year, S. Dakota wants to jump seedings 1.65 million – half of the WCB’s 3.35 million higher intentions, The ECB also revealed a larger 3.13 million corn acres vs. 2019 & 1.43 million more acres than 2018. 2020’s US soybean plantings could be up 7.41 million acres to 83.51 million acres vs. 2019. However, seedlings were 1.355 million less than trade’s average. ECB planting ideas are up only 1.7 million while the big bounce-back occurred in WCB where 4.9 million intentions were reported. The biggest jump in intentions occurred in N & S Dakota of 2.9 million after last year’s 3.45 million decline.

Not surprisingly, corn weaken on these 2019 planting intentions, but slowly recovered because of corn’s smaller March stocks. With the survey period beginning on Feb 27, the impact of the recent oil price crash that shut-down ethanol plants and broke cash corn prices weren’t in this report suggesting lower actual spring plantings will occur, too.

The USDA’s quarterly stocks had a mixed output. Corn was sharply lower-than-expected while beans and wheat were near expectations. Corn’s 7.953 billion bu. stocks were 172 million lower than the trade. Using exports & a strong winter industrial usage, this level projects corn’s winter feed/ residual demand at 1.397 billion bu. up 17% from 2018/19. This suggests a likely175-200 million higher feed usage. However, reports of a 20-25% drop in April ethanol output because of unprofitable margins could counter this demand rise. Exports remain vulnerable for a cut too.

Soybeans March stocks at 2.253 billion bu were 12 million higher than trade’s survey. Wheat’s 1.412 billion bu. stocks suggest no change in wheat’s 150 million 2019/20 feed use.

What’s Ahead:

The trade’s focus was on the US planting levels. However, corn’s lower stocks countered this higher plantings short-term. An overestimated of the 2019 corn crop (poor test weight) or a hefty jump in corn’s feed usage are possible resolutions to this corn issue. Energy prices, COVID-19 health trends, and S AM / US weather all are price factors for the next month. Wait for previous sales points.

Comments

Log in or sign up to join the conversation.