Facebook (FB) had a really tough year in 2018. There were negative news headlines coming out each month about privacy issues, election interference and other abuses of their platform.

Even though most of the news stories were hyperbolic and made things seem worse than they really were, the stock got absolutely hammered. In fact, it dropped over 40% from peak to bottom.

After the latest Q4 2018 earnings report, patient holders of the stock were rewarded because the numbers were incredible.

The stock has started a turnaround, which could continue well into 2019 and beyond unless there is some other unforeseen event.

Here are 10 reasons why Facebook stock is a great investment.

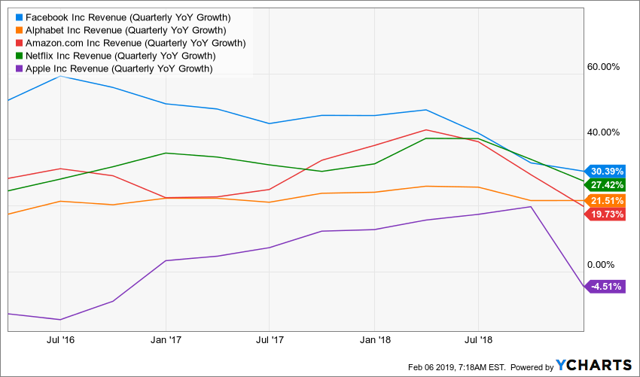

1. Revenue growth is still strong

In Q4 2018, Facebook's revenue grew 30%, or 33% in constant currency.

For the full year 2018, revenue grew by 37% while earnings per share increased 40%.

Their ongoing share buybacks should ensure that EPS growth will continue to outpace revenue growth.

Keep in mind that Facebook has guided for a continued moderate slowdown in revenue growth, which is not surprising given how massive the company already is.

The graph below shows that Facebook was, and still is, the fastest growing of all the FAANG stocks:

2. The core Facebook platform is still growing, despite the negative headlines

Despite all the hate from the media, the core Facebook.com platform actually showed impressive growth in Q4. Not only did they continue growing fast in Asia-Pacific and Rest of World, but they also managed new all-time records in their most saturated markets.

A new record for daily active users in US & Canada was set, at 186 million, up from 185 million in the past three quarters. They also set a new record for monthly active users in Europe at 381 million, showing that they are still growing there despite the recent GDPR regulations.

3. The Facebook family of services now reaches 2/3rds of global internet users

Facebook owns more than just the core Facebook platform. They also own Instagram, Whatsapp and Facebook Messenger, which are all massive platforms on their own.

According to Facebook's best estimates, 2.7 billion individuals use at least one of their services each month. About 2 billion of these people are daily users.

Given that global internet users are estimated around 4 billion, this means that Facebook reaches 2/3rds of internet users each month, and half of all global internet users each and every day.

4. Regulation could cement their (and Google's) strong position

Part of the bear thesis against Facebook is that governments around the world want to regulate them, for example by changing the laws on data collection, privacy and ad targeting.

However, this does not necessarily have to be a bad thing, as these laws would also apply to Facebook's current and future competitors.

It's the big giants that have the resources to deal with all sorts of regulations and this could be a major deterrent to new competitors. Many startups simply won't have the financial strength to deal with all the bureaucracy.

5. Facebook has a multi-decade runway of growth in emerging markets like India

It is true that the Facebook is close to having saturated the market in North America and Europe, which are the most lucrative markets for ad revenue, by far.

However, Facebook is also dominant in emerging markets like India, Indonesia and various countries in Asia.

It is predicted by many experts that India will become the next China, a massive economy with a population that dwarfs the US.

Given Facebook's, Instagram's and WhatsApp's strong position in these markets, it could potentially provide a multi-decade runway of growth for Facebook as these countries become wealthier.

6. Most of the privacy issues are based on old problems

The majority of the negative news headlines about Facebook in 2018 were based on old news, for example the Cambridge Analytica fiasco which happened in 2013-2016.

Facebook has already fixed most of these problems, or is actively working hard on fixing them. So the news coverage should quiet down once the media can't find any more old "dirt" to dig up.

Although there is still some headline risk in 2019, I don't think it will be nearly as severe as 2018.

7. Facebook has 40 billion in cash and is actively buying back shares

Facebook is one of the most profitable companies in the world, with 15 billion in free cash flow last year despite heavy investments in safety and security.

They now hold 40 billion in cash, which is about 8% of their market cap.

A lot of the cash is now being deployed for share buybacks, which means that EPS grows faster and patient holders of the stock are rewarded because their shares will now represents a greater percentage ownership of the company.

8. Facebook has many massive untapped opportunities

Facebook's core business revolves around online advertising, in which they are better than anyone due to their powerful ad targeting. Given that their sales are less than 10% of global advertising spending, there is still a long runway of secular growth in that core business.

But Facebook isn't stopping there. They are also pursuing other business opportunities, including mobile payments in Whatsapp and Messenger, as well as commerce on Instagram and Facebook Marketplace. These could end up becoming massive businesses on their own in the next few years.

And let's not forget that Facebook also owns Oculus. This year, the Oculus Quest is going to launch, which is a potential game-changer for the VR market.

9. The stock is very cheap relative to its growth rate

Despite the stock rallying 38% off of its bottom in late December, it still looks cheap if you consider its growth rate.

Facebook's trailing PE ratio is only 22, but their EPS growth last year was 40% This would give them a PEG ratio of 0.55, which is incredibly low and implies that they are highly undervalued relative to their growth rate.

10. Expense growth will decrease after 2019

One of the main negatives from their Q4 2018 and full year 2018 earnings reports, was that expenses have increased significantly in 2018.

This led to a drop in operating margin from 50% in 2017 to 45% in 2018.

Although their margins are still ridiculously high compared to most companies, if this trend would continue then it would be a cause for concern.

However, Facebook's management has claimed that expense growth should moderate after 2019 and become more in-line with revenue growth after that.

Mark Zuckerberg is a fantastic CEO and he doesn't run the company just focusing on the next earnings report.

He is running the company with a long-term vision and he's willing to sacrifice short-term profits for long-term growth and market share gains.

Comments

Log in or sign up to join the conversation.