While Declared Dead, DJII Just Won’t Stay Down

While declared dead, DJII just won’t stay down.

Bond rates continue to tumble as Brexit stokes fear

Equities even more underpriced relative to bonds

Equities fell on Brexit vote but rebounded as bonds soar

Upward pressure from higher dividend-discount value of DJII, offset by domestic and foreign liquidation to raise cash to be reinvested in “safe assets”.

Into bonds perhaps? They have momentum?

Following a week of huge political turmoil in Euroland, being interpreted as financial Armageddon by some traders caught on the wrong foot, the DJII has recovered most of its loss since Brexit. By Thursday last it ended the month at 17,930 up from 17,878 at end of May and 17,682 at the end of March 2016 as well as 17,425 on December 31, 2015.

This is attributed to the enormous and continuing upward pressure on the price of the DJII by the seemingly ever-rising dividend-discount value of the DJII. This has been brought about by the combination of a record DJII dividend and a falling discount rate as measured by the U.S. 30 year T Bond yield, which has fallen in tandem with the U.S. 10 year note.

From turmoil of the PIIGS in Euroland in 2011 to the craziness of negative yields of 2016, U.S. 10 year Treasury rate remained a beacon of stability at approximately 2% but is now under 1.5%. While it does not look as though the USA will voluntarily move to negative interest rates, the Fed has no direct control over the long end of the bond market. Market forces, however, may result in the rate of the 10 year note of falling further. It being seemingly the only game in town for safety-seeking, yield-hungry market participants.

“Buy when there's blood in the streets."

Attributed to Baron Rothschild who bought in the panic that followed the Battle of Waterloo.

Out of the Euro-panic of 2011 by far the biggest winner among those countries that still have positive yields, is Ireland. Since blood ran in the streets in 2011 the 10 year rate has fallen from its peak of 14% to under 0.5%. From disaster and despair to the new financial darling of the post-Brexit EU. This is particularly the case in the eyes of many Britons of Irish descent who want to remain in the EU as evidenced by the overwhelming demand for Irish passports.

It used to be that borrowers paid lenders. The new paradigm requires that lenders pay borrowers. In this topsy-turvy world of new finance, sovereign borrowers are keen to take advantage of not only negative rates in the shorter term but extremely low rates in the very long term.

Since 2011 when Ireland was one of the pariahs of the investment world 10 year rates have dramatically from 14%. On March 30 2016 the Government sold a 100 year bond with a 2.35% coupon. This is effectively a perpetual bond, similar to British Consols that were recently redeemed. At the time of issue, the 10 year bond yielded 0.66%. With the 10 year rate now at 0.48% the buyer of the 100 year bond is sitting on a tidy paper profit. Given the seemingly insatiable demand for any positive yield the buyer may even be able to lock in that profit by selling it. Perhaps the buyer may keep it in anticipation of negative 10 year rates in Ireland in the near future.

Equities Grossly Underpriced Relative to Bonds

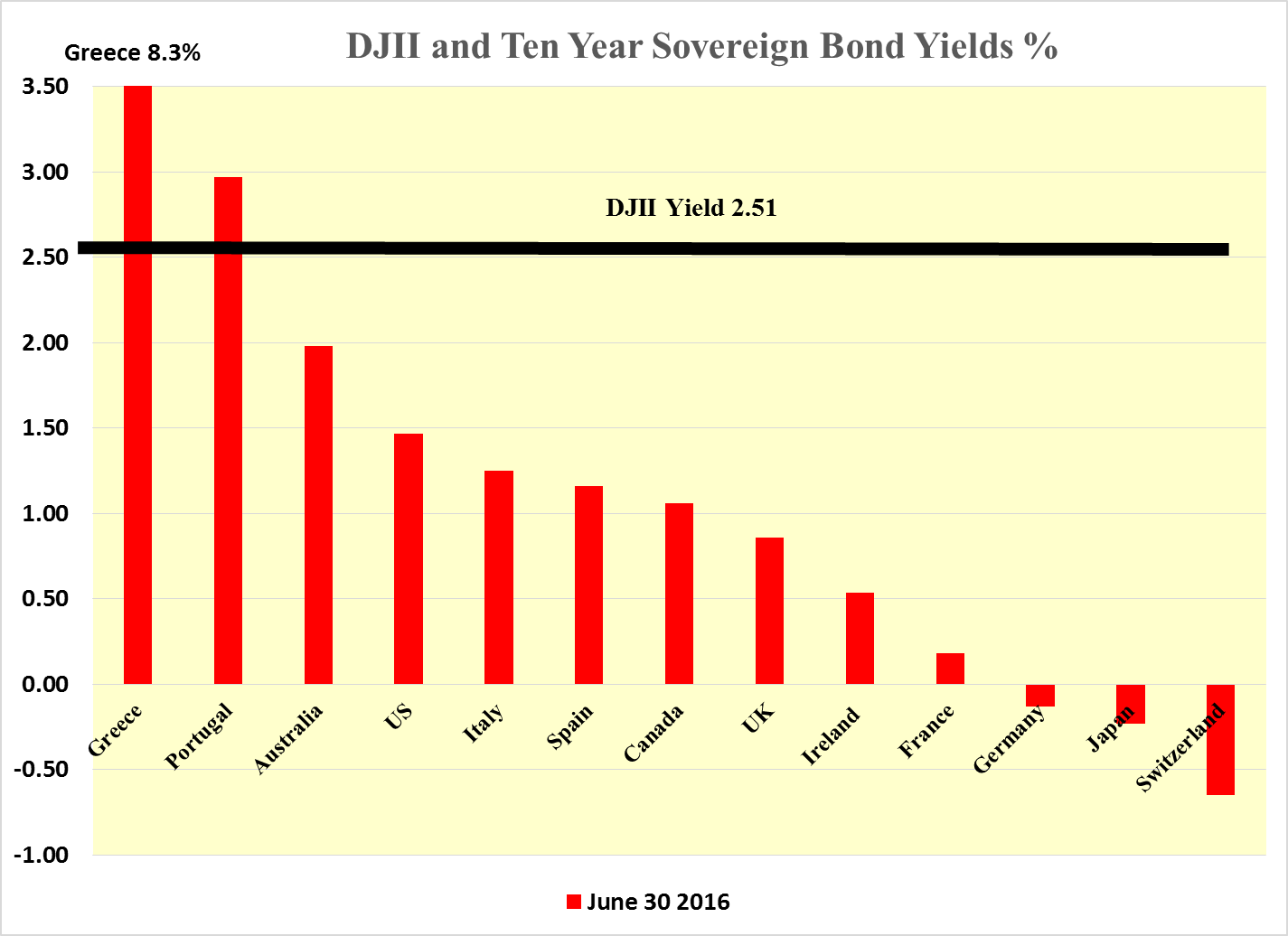

There are fortunately, alternatives available to overpriced bonds with their low positive and even negative yields. Some alternatives also have growing coupons. This is particularly so on an after-tax basis. In a word “EQUITIES”. The yield of the DJII on June 30 stood at 2.51%. It seems market participants would rather play the greater fool theory and ride the bond bull as rates disappear into the never-never land of negative yields.

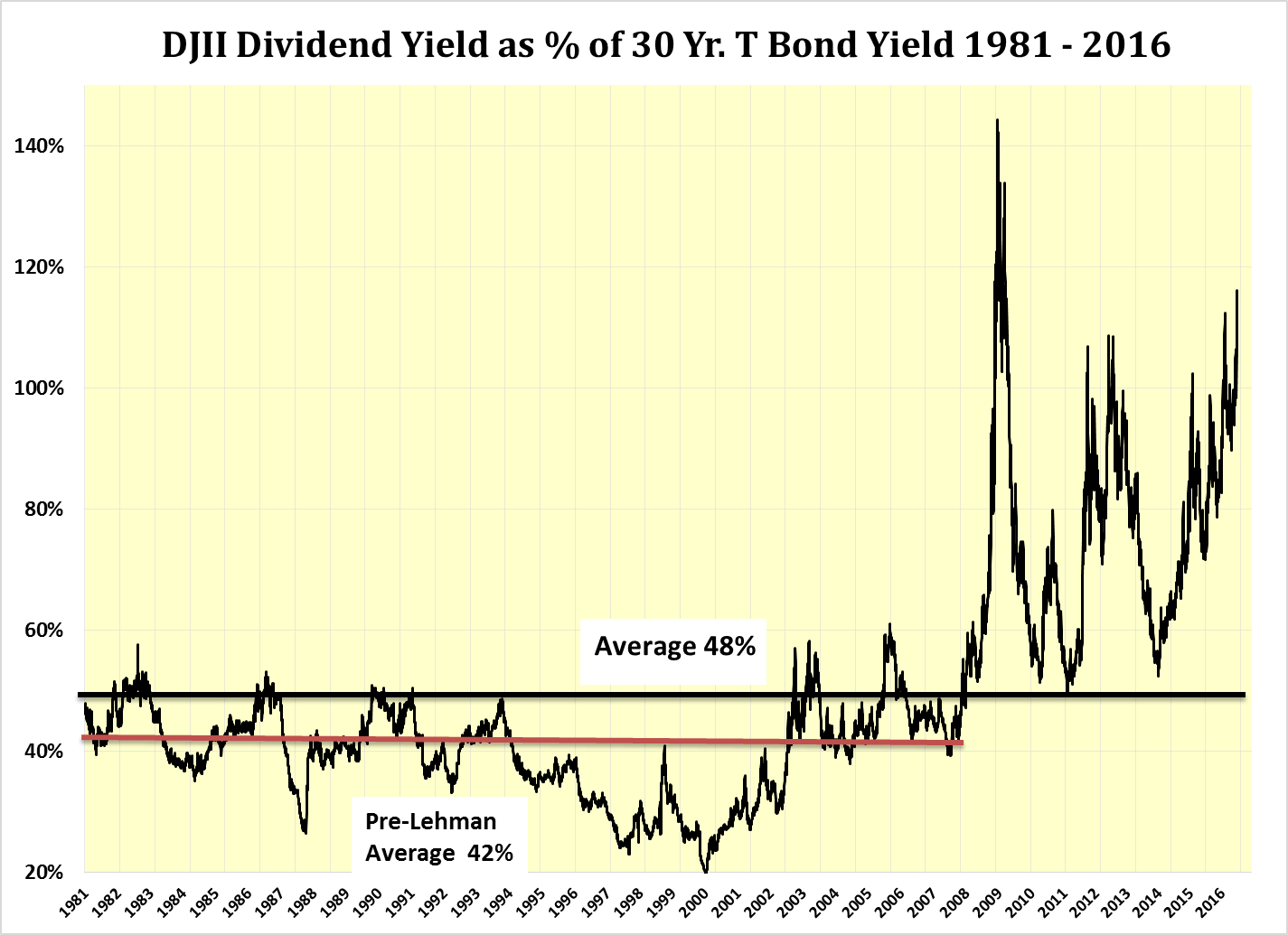

The yield of the DJII stands at 112% of the yield of the 30 Year T Bond compared to the long-term average of 48% and the pre-Lehman average of 42%.

Just as Ireland was seen as one of the pariahs of the investment world in 2011 so too has the DJII been avoided by irrational pessimism since Lehman in 2008 and for the third time since Lehman we are in the territory of sheer terror.

With the benefit of hindsight Irish 10 year government bonds have turned out to be a champion investment. Looking ahead the same sort of outstanding DJII price performance that has already been seen since March 9, 2009 when the Price closed at 6,547 today we are already at 17.949 with more to come.

The dividend- discount value of the DJII, which stands at 48.063, has been in excess of its price ever since Lehman. It has been by far the most important reason for remaining bullish on the DJII, likewise the S&P 500, and it remains so as it shows how terrified market participants are relative to sovereign bonds.

As a couple of examples of the wholesale dumping of equities for reasons other than logic has been the selling of $200 billion of U.S. equities by China and OPEC nations to raise cash. Selling US equities such a manner shows an even greater level of ignorance about foreign markets than about their own markets having thought that they could support a grossly overpriced domestic markets by government dictum.

The dividend-discount value of DJII is 30,000 points above its price and the naysayers conclude that the model must be wrong and the price is correct. To justify this stance it is claimed that the market is discounting a return to normal interest rates at both ends of the debt spectrum. Surely this should hold true for the debt markets as well. However, rates continue to fall and market participants continue to ride the bond bull.

Until Lehman, the dividend-discount model stood the test of time and it is extremely useful in determining value, which being so far above its price gives a great deal of comfort to any buyer of the DJII. So why has the price of the DJII been stuck around the 18,000 level for the past year and a half?

In a word “desperation”. Desperation of impatience, by momentum player that have switched from the stock market to the hot bond market. Desperation from the need to raise cash by the likes of China to support the Yuan and oil producing nations who are suffering from low prices. This selling has taken place on a scale never seen before. Unfortunately the selling could well continue as the Japanese Government Pension Fund now turns about face on last year’s decision to increase its equity weightings and move to safer investments. Bonds?

From the following chart it can be seen that previous bouts of reduced buying have tended coincide with falling markets. Since 2012 the DJII has risen. While there was net buying in 2013 there has been liquidation by foreigners since the start of 2014 and this has reached a series of record ever lower levels.

The fundamentals of the DJII are positive. Last Friday the DJII dividend hit yet another new record of $450.16. The payout ratio remains below 50%. U.S. economic activity while mediocre, is still positive and expected to remain so for the foreseeable future. Hence, the dividend should remain safe and could well rise as earnings recover from their recent setback.

Seemingly the only thing that is holding the DJII price back is foreign liquidation and desperation among the impatient who seem quite happy to buy high-priced and ever-lower-yielding bonds as they ride the bond bull in the hope that they will be bailed out by greater fools than they.

On musing further, it seems as though the aversion to equities is akin to the antithesis of the Tulip Mania and the South Sea Bubble, which ended disastrously. Perhaps the outcome of today's underpricing will be a sharp and substantial increase in the price of the DJII back towards its dividend-discount value. The triggering of such an outcome could be the recovery of earnings and with them the realization that the DJII dividend is safe and its yield is so much more attractive than the low and negative yields available on bonds.

more