When Will Chasing The Hot Stock No Longer Work?

If someone had asked me to name the driving factors influencing US stock market performance return over the past year, I might have guessed the cut in the tax rate, but I would then be at loss to further explain what has been moving stocks.

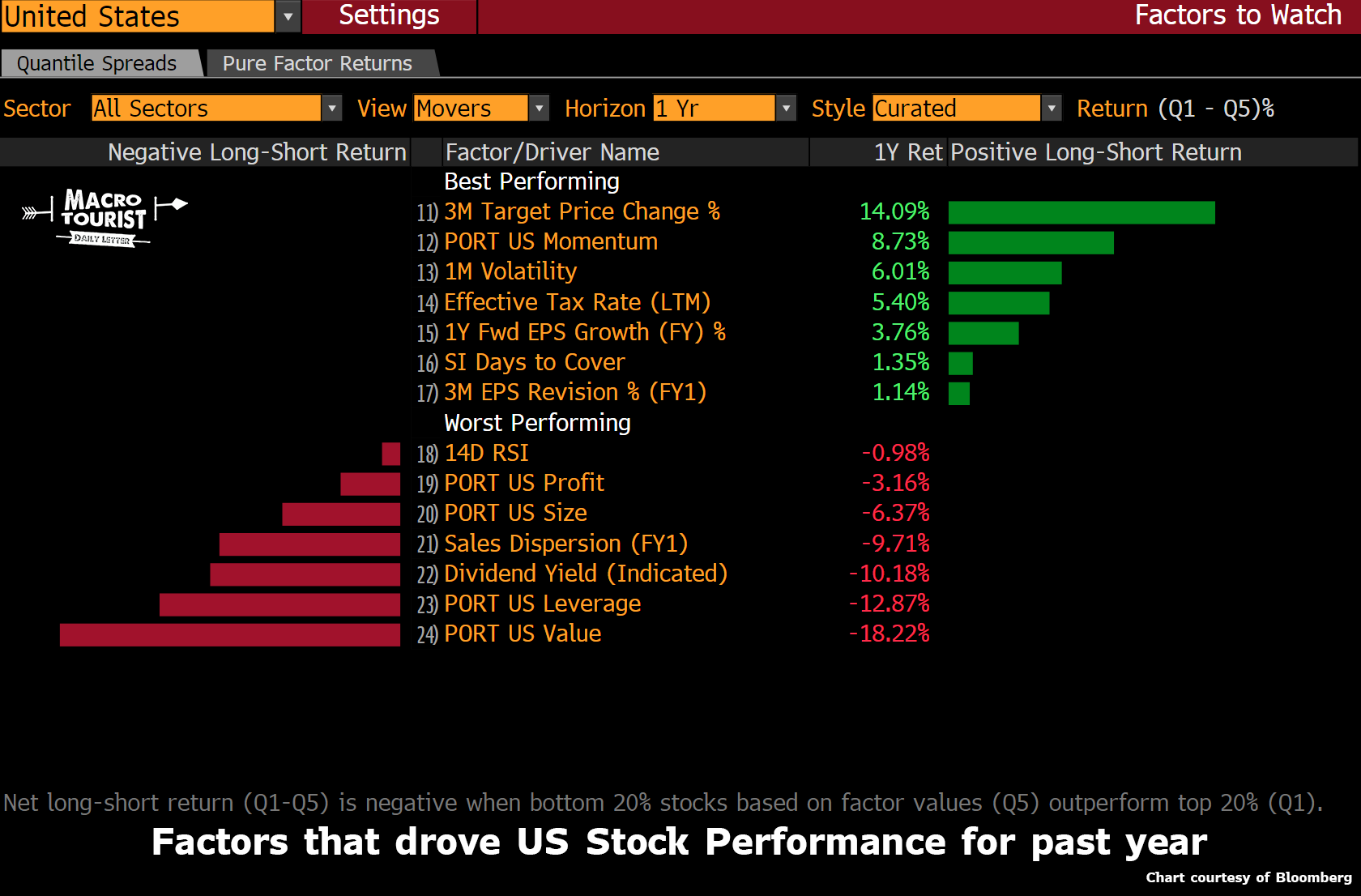

Lucky for me, Bloomberg has this great function that allows us to examine how various portfolio factors have performed over different time frames. It works by taking the stock market universe, then ranking the companies by the requested factor (whether it be P/E, cash flow, etc…) into five quintiles. Using the average return of the top quintile during the requested period, minus the average return of the bottom quintile, gives a great sense of the sensitivity of that factor in individual stock market performance.

Let’s have a look at the best and worst factors during the last year:

At the top of the list are momentum-type factors and then volatilty. Who’d thunk it?

But what does that really mean?

The top-performing factor - by a rather large margin - was “3M Target Price Change %”. Bloomberg defines this as “Percent Change in the Best Target Price over past 3 months. When an analyst jumps out ahead of the pack and cranks his/her target, this puts that stock to the top of the list for this factor. This means that mindlessly following analyst 3-month target price changes was the smartest strategy over the past year from this list.

Really? That’s kind of mind-boggling. It implies analysts are actually adding value with their calls. When did that last happen? I am an old-school institutional trader who likes to rib my analyst pals of a famous line often recited on trading desks - “research analysts: in a bull market - who needs them? In a bear market - who can afford them?”

Well, the laugh is on me. Chasing these analysts’ boldest calls is a top-performing strategy.

And the next top-performing factor, “PORT US MOMENTUM”, is another one of those it-can’t-be-that-simple strategies. Bloomberg defines this little gem as the “arithmetic average of weekly return for trailing 52 weeks lagged by two weeks. So basically, you buy what’s been going up for the past year while shorting what’s been declining.

Huh? What about stuff like Price/Earnings or Price/Book ratios? Where are those fundamental factors? Surely, just chasing the hot stock can’t be a portfolio strategy.

Yet that is exactly what the market is telling you has been working.

The next one - “1M Volatility” is really an offshoot of the previous two. If investors are chasing faster growing stocks (which are typically more volatile), then we would expect to see volatility outperform as a factor.

Now let’s examine the bottom three factors that have been doing the poorest job over the past year.

“Dividend Yield (Indicated)” has returned a whopping minus 10%. Obviously the market has stopped rewarding investors hiding in supposedly safe higher-yielding dividend stocks. Given the fact that since the Great Financial Crisis a torrent of yield-starved money has flowed into these companies, it makes sense that eventually we would hit a point where they stop rising. 2018 seems to be the point where that trade reverses hard. Blame it on the Fed raising rates, or maybe it was just time, but this strategy is no longer working.

Next up - “PORT US Leverage”. Could this be the same deal? Are higher rates hurting companies with too much debt relative to equity? Both of these factors could be a function of the market’s concerns about higher interest rates in the future.

But finally we get to the factor that has crushed many a hedge fund manager over the past decade. Value. Even though value has underperformed since the GFC, 2018 has offered no respite. In fact, the relative peformance of this strategy has accelerated to the downside.

Bloomberg defines “PORT US VALUE” by averaging the following fundamental metrics:

- Book Value to Price

- Cash flow to Market Cap

- Net Income to Market Cap

- EBITDA to Enterprise Value

- Earnings to Price

- Sales to Enterprise Value

You know - all those good things that go into determining the fundamental value of a company.

One might think buying cheap companies relative to the underlying business would be a good strategy, but that’s not what has been working.

Great. I have now shown that fundamentals don’t matter and that chasing the hot stock is all one needs to do to outperform.

But nothing lasts forever.

Let’s have a look at the of this phenomenon to get a sense of whether there are any signs of this trend changing.

First up, here is a long-term chart of the “Momentum” strategy.

The uptrend of the past couple of years is evident, but look at the recent action.

“Momentum” is no longer being rewarded quite as heavily, and in fact, during the latest equity market sell off, the stocks that had performed the best over the past year led the move to the downside.

Is this a change is trend? Or merely a pause to refresh?

Not sure.

And how about value?

No trouble defining a trend here. Value has dramatically underperformed growth for years.

And recently?

Yeah, value got a bid versus growth, but we are a long way from a change in trend.

Although I would love to be able to tell you that the days of “momentum” and a return to “fundamentals” are imminent, I have no such confidence.

Never told you I have any answers, but hopefully this helps explain a little bit of what’s been going on behind the scenes. If someone knows when this madness will end, please let me know. I would love to return to a market where chasing the hot stock no longer works…

Disclosure: None.