War On Short Selling; The Last Hope

If the PBOC was desperate last week, the catalog of words describing their likely stance this week is unbelievably short (pun intended). In the handbook of central bank operations, when conditions truly spiral out of control the first entry in that chapter says to blame speculators. Primary among them, subchapter one in the handbook, are the short sellers. If you think back to 2008, even the supposedly steady and omniscient Federal Reserve encouraged the SEC to ban short selling on bank stocks (first naked that July; then outright on September 19). As if it needs to be pointed out, it doesn’t work.

What short selling bans amount to are acts of proclaimed exhaustion; the central bank or central financial authority has no other options left and short sellers make a good and public target. Increasingly, it seems the PBOC in calling for increased “flexibility” (read: despair) the past few weeks (subscription required) has more and more focused on those speculators supposedly short selling yuan. Because of China’s dual market for currency, CNY and CNH (offshore), any distance between them supposedly opens arbitrage opportunities which can only further destabilize an already precarious position. Thus, by targeting speculation of that kind the PBOC claims to be working back toward good order.

So the behavior of the “dollar” is much like a short squeeze, and now the PBOC has used its state run banks to enact a short squeeze in yuan – fighting a short squeeze with a short squeeze. How could it possibly fail?

The arb between onshore and offshore RMB has the effect of moving “dollar” transactions to Hong Kong and away from onshore China; a “speculator” might “buy” CNH in Hong Kong and then “sell” in CNY in Shanghai, all using “dollars” as the funding mechanism. It displaces dollar activity and volume that is obviously needed and necessary onshore where the PBOC clearly believes it has legitimate interests. In other words, this is not the center of China’s “dollar” problem so much as it makes it that much more difficult and unsteady.

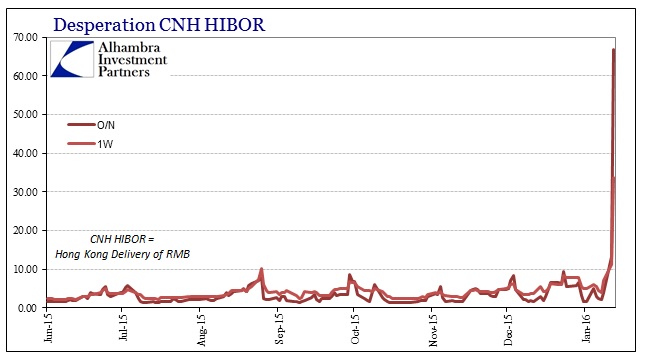

To be more specific, these damned “speculators” are believed not so much “buying” CNH and “selling” CNY but rather “borrowing” CNH and “lending” CNY. The jargon and technicalities get confusing because intent matters in these affairs more so than the actual arrangement of transactions. By tasking state banks to “buy up” CNH, that left little liquidity with which speculators might “borrow” and short it. The results:

Overnight HIBOR (CNH) hit a ridiculous 66.815%, while one-week HIBOR spiked to 33.791%! Even the 3-month maturity blasted to a record, jumping to 10.42%.

If you think the problem is shorts, in this case CNH speculative shorts, then 66% borrowing rates should work – for a time. If, however, you have some appreciation for the Asian flu and Thailand’s role in it, there is an eerie rerun taking place except in China rather than Thailand. As I wrote two and a half years ago (and then updated last week) in trying to argue why Brazil would almost certainly follow Thailand (which they did):

In terms of the proximate currency problem in Thailand 1997, the Thai central bank did what the monetary textbook says to do. Unfortunately, economics and economists rarely understand finance, speculators in particular. To defend the baht, the Bank of Thailand sold dollars into the spot market and then engaged derivatives trades, dollar swaps, to protect their reserve stash…

But swaps, particularly when engaged with the “market” instead of with another coordinating central bank, actually fuel the currency’s demise. Because of the leverage obtainable in currency speculation, the only real means to reduce speculative selling pressure is to make the currency more expensive to short (since it must be borrowed, reduce the availability). Engaging in swaps, which amount to forward selling of dollar reserves, reduce the pressure on interest rates in the short-term funding markets. It’s like sterilizing the impact of selling dollars in the spot market – the central bank selling dollars buys the local currency, making it less available and thus theoretically driving up the cost to borrow it. If you pair the spot intervention with a swap/forward, you’ve given speculators a huge alternative access point to borrow/short your currency.

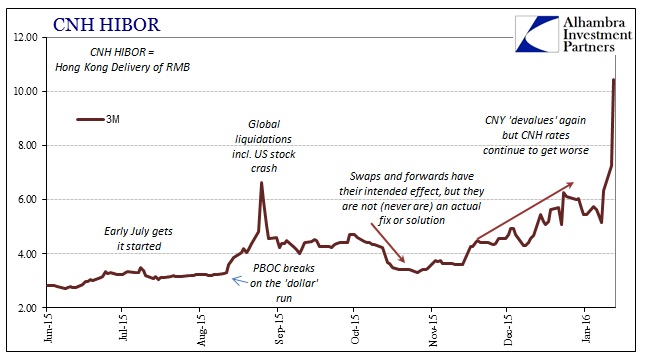

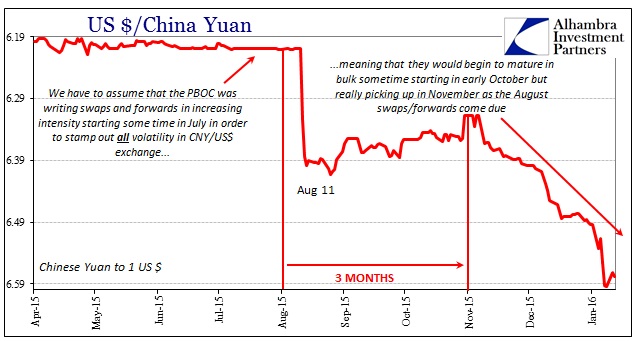

We know that PBOC has been taking swaps and forwards as a primary measure for intended CNY stability; they confirmed as much months ago, though they needn’t have done so given the obvious trajectory in the currency exchange rate (3-month intervals are insanely prominent). The actions this week in CNH money markets confirms the second part, as the central bank now goes about making CNH (and CNY by indirect proxy) almost impossible to short.

If those swaps and forwards were intentioned toward stopping prior “devaluation”, or at least reducing it, that meant the PBOC was essentially selling dollars (in derivative form) immediately, or putting the PBOC short the dollar/long CNY. At maturity, the PBOC then has to reverse (or roll, which isn’t a clear cut option) meaning that it will have to “buy” dollars by “selling” CNY – exactly the opposite position as it is staking out this week. The actual mechanics can and will be much more complex and intricate, but in general terms that is what takes place. Therefore you can see how these efforts in many ways undermine each other; the PBOC on the one hand this week is making it more difficult to borrow yuan while at the same time past derivative arrangements are coming due with which the PBOC is providing yuan to the “speculative market.”

The only hope is that the geographical distinction offshore vs. onshore becomes something of a positive rearrangement as the PBOC’s derivatives have it supplying yuan in CNY. The fact that such fragmentation has already arisen suggests the problem with all of this to begin with (below).

Typically, the timing of these legs are lagged so that there isn’t a direct cancelation of one to the other. In Thailand, for example, the efforts appeared to have worked but only for a short while until the forces of repression simply returned with a vengeance (in Brazil, Banco do Brasil bought more time that Thailand managed but ultimately it didn’t matter either). That means the PBOC’s attempts exhibit undoubtedly the same frailty; it is only to “buy time” with the hope that the primary problem of repression somehow just goes away. In the context of speculators, that would mean that the PBOC, as Thailand and Brazil, is trying for an ultimate display of monetary power so that they “get the message” and just take their dastardly schemes someplace elsewhere. Unfortunately, speculators never seem to cooperate in that respect because speculation is never really the problem.

In attacking the speculative aspects of these currency repressions, central banks never answer the question that should be addressed from the very start: why are speculators “attacking” in the first place? Why would the Thai baht in 1997, Brazilian real in 2013 and Chinese CNY (or CNH) in 2015 seem a good place to make a currency killing? Speculation is but one mechanism by which imbalance is brought back to a steady state. It is a violent, messy and disorderly method, but cuttingly effective which is why short speculation makes for such a good, public target. Nobody likes disorder but the orthodox economics textbook has made it exponentially more undesirable by treating market forces as the enemy when in fact it is markets that, when allowed, produce needed efficiency in the long run. Central banks trade short term outbreaks of calm for long run continued problems of inefficiency and imbalance. Market forces, including speculation, is trying to trade short run disorder and turmoil, sometimes very nasty, in order to find a more suitable long run balance.

China is untenable in its current financial position. That is the primary problem, and so long as it remains so whatever the PBOC does will have but a fleeting impact. In more immediate terms, that is being recognized by the “dollar” run which continues to savage not just China but South America (more than just Brazil), Africa, Asia (more than China) and you might even argue Canada and Mexico. From that, we see that it isn’t China that is the problem with the “dollar”, it is the whole damn system.

I think we are well past the point of no return where ever major adjustments can be undertaken in order to preserve that past functionality. Volatility itself will ensure that, because once volatility becomes significant the world’s mathematical models start flashing uncontrollable warnings (for resource providers, the money dealers, the warning is to get out or get out even quicker; for speculators, the warning is to attack the volatility as a huge opportunity) which then become self-reinforcing. Imbalance no longer able to be maintained becomes a paradigm shift or reset. Unfortunately, 2008 was an attempted reset which is increasingly revealed (past 2011) as an aborted one.

Disclosure: None.