Volatility Bets Hanging On

As equity market implied volatility grinds lower it's worth throwing a couple more charts into the mix. In this post we look at ETF bets on the VIX and cross-asset volatility. ETF market bets on the VIX are hanging on despite the headwinds that such products face, it goes to show there are still holdouts despite the continued grind-down in implied volatility. And it's not just equity market volatility that's compressing, our measure of implied volatility across asset classes is also falling.

It's almost a certainty that volatility will rise, it's really just an issue of timing. The ETF products that go into the chart below provide a lottery ticket type bet in that a spike in the VIX has the potential to return massive and rapid profits, but the deck is stacked squarely against these products with the return since inception for most long-VIX ETFs often printing at around -99%. They can be useful tactical/dynamic hedges, and given the rising risk of a correction there's probably some case for more diligent risk management now. Just be careful what you wish for, and how you wish for it!

ETF market bets on the VIX are hanging in there as new money flows in to take the place of the value eroded by the futures roll costs and indeed the falling VIX itself.

(Click on image to enlarge)

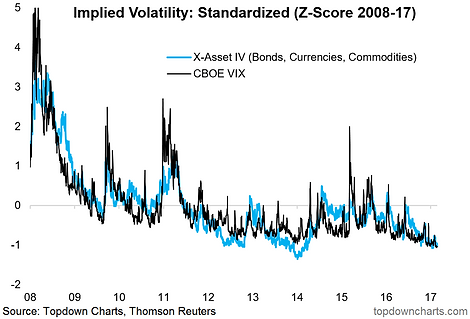

Implied volatility has broadly compressed across asset classes. Our gauge of cross-asset implied volatility measures IV for bonds, currencies, and commodities.

(Click on image to enlarge)

For more and deeper insights on the global markets, good charts, and actionable investment ideas you may want to more

Comments

No Thumbs up yet!

No Thumbs up yet!