The Conspicuous Consistency Of Curves

It’s not that curves are flattening. It’s where they are. There’s really no mystery surrounding any of this. The “conundrum” arrives only when starting from the Orthodox perspective; the one derived from Economists even though they don’t understand the bond market in the slightest.

Short-term rates tend to “obey” central bank signals because central banks offer more direct money alternatives. If the Federal Reserve offers X on its reverse repo, it makes sense that money market rates would cluster around X given that they have this alternate.

In an ideal world, however, they wouldn’t just cluster they would abide by these intended strictures. If there is one thing we’ve learned over the last eleven years as global hierarchy has broken down, try as they might central banks don’t have as much influence as they once thought they did.

And if any central bank has difficulties down at the short end, what obligation remains for the long end of any curve? Longer-dated maturities are therefore far more fluid in how they process these dynamics; meaning, largely, the consequences of what’s going on at the short end. These tend to be very different from mainstream Economic theory.

The fundamental difference begins where the Economics textbook doesn’t go. For one example, the ECB’s PSPP program (QE) included within its market guidelines specific recognition of practical central bank experience. The Federal Reserve in 2013 realized it was stripping repo collateral out from money markets by buying in OTR issues. They very quietly stopped doing that.

Thus, when the ECB started up its version of QE two years later it made sure to recognize these potential consequences:

The Eurosystem lends securities using the channels for securities lending available under its existing infrastructure, including so-called fails mitigation programmes by international central securities depositories, agency lending and bilateral securities lending.

In other words, like the Fed’s reverse repo the ECB makes available to the market the securities it buys and then holds at each National Central Bank for collateral purposes. It doesn’t do this on its own, rather it merely opens the door for market demand should it ever arise:

The ECB also participates in Euroclear Bank SA/NV’s Securities Lending and Borrowing Programme (SLB) for the purpose of mitigating fails. The terms and conditions of this programme are the standard ones defined by Euroclear. Please contact Euroclear Bank SA/NV for further information.

Therefore, by mainstream definitions, something like May 29 should not have been possible. A global collateral call that struck the European markets more so than any other in theory would never had happened. After all, the ECB reports that up to the end of May 2018 it had obtained €485 billion in just German debt through QE.

And yet, German paper was in such high demand during the second half of May that bund yields plummeted, thereby signaling for yet another time they really don’t know what they are doing. In theory, it all works so seamlessly. In practice, it’s a total disaster. Still.

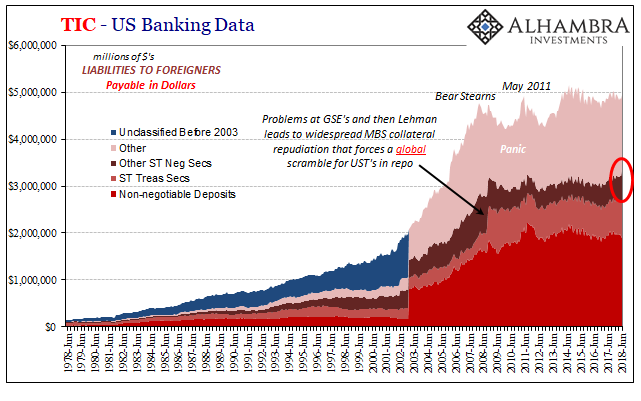

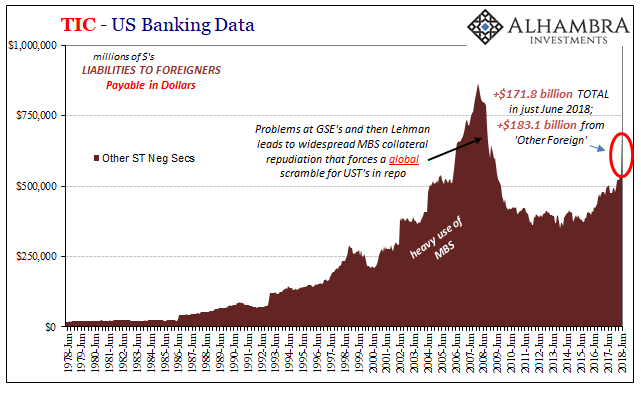

This is what the curves are telling us. Again, they aren’t hard to interpret. If you need some “other” financial market participants to step in with ~$200 billion in “other” ST securities to rescue the system at the last moment, that isn’t a very robust or even reasonably healthy condition.

But this isn’t what you hear on TV or what’s written in every story published at reputable news outlets on the internet. According to this narrative, central banks haven’t just been adequate, they’ve collectively “flooded” the world with liquidity or even money.

It’s just not true.

Staying with Germany’s bond market, you can see that yields bear no resemblance to ECB purchases. When Bill Gross tweeted in April 2015 that German 10s were the “short of a lifetime” what he was really saying was that the PSPP (together with the other major ECB LSAP’s) was going to work well and when it did the selloff in bunds was going to be epic.

That part, the theory, he got right. If monetary policy had triggered a real recovery of substance, the German bund curve would have dramatically steepened in the back end first.

Initially, it appeared that the market agreed as for a couple weeks anyway German as well as US bonds sold off rapidly. It didn’t last simply because effective global liquidity in the eurodollar system was unmoved by anything the ECB had done, was doing, or would ever do.

For over a year, the curve fell and flattened, the exact opposite of what would have signaled successful monetary policy. Many still try to argue that rates are low because central banks are buying, but that’s easily debunked especially by German rate history (like UST’s, bund, bobl, and schaetze rates fell far, far more without ECB buying than with it).

Germany’s curve only began to behave at the start of 2017 during Reflation #3, which wasn’t so much a European event as a lessening of global monetary pressure. Rates rose even though the ECB was still buying a lot of sovereign debt.

But, as you can see immediately above, inflation hysteria last year was predicated on the smallest level of improvement. It truly was a molehill. After nearly €2 trillion in LSAP purchases, that’s all the bund curve had moved. It was practically nothing – because markets continued to bet that over time there was a far greater chance central banks would be shown yet again to have failed than there was any possibility they got it right this time.

The long end is where the skeptics are when in the mainstream these are treated as heretics.

Now the curve is flattening again but at a level not significantly different than when Europe’s QE savior was launched. The lesson of May 29 simply reinforced the liquidity risks that are always present.

The curves throughout that past three years (and long before that) have been consistent in a way central bankers never will be. They are saying, without ambiguity, there is no recovery and there really isn’t likely to be one well beyond the foreseeable future. It really is that simple.

Nothing central banks do are able to push curves off this verdict because theirs is only an illusion of control further fostered by a media that gets all its monetary information and interpretations from Economists working for central banks.

German bunds or UST’s, the message is the exact same. Flattening at low nominals means liquidity risk remains paramount. This overrides every other concern, including hostility to either government’s fiscal outlook. The US may be technically insolvent given its long-range liabilities, but UST’s are going to be bid so long as the real and effective global money system continues to be a malfunctioning mess.

Liquidity risk is today, right now. A US default is some way off event that just doesn’t matter when faced with that call to put up more collateral. Since nobody’s getting marginal collateral from these rigid government silos, and without the proper money dealing facilities to facilitate flow and redistribution, May 29 is what you get.

(Click on image to enlarge)

It’s not the absence of bank reserves or even collateral held by central banks, it’s the lack of dealer capacities especially in times of stress.

Disclosure: None.

The only thing I disagree with is that I believe the central banks know exactly what they are doing. They don't want the conundrum to end. Too much collateral at stake.