Still Easy After All These Years

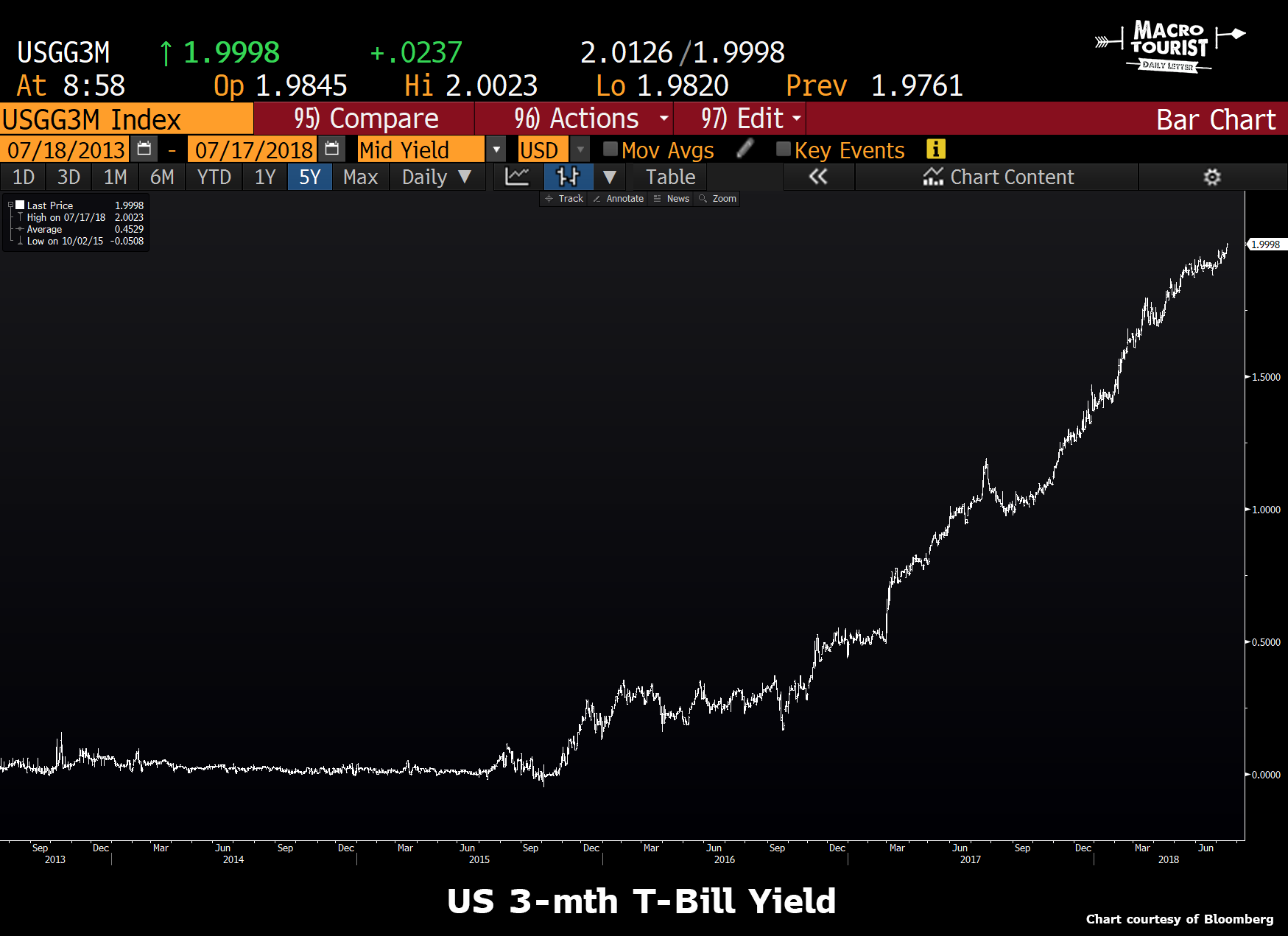

The other day I was listening to some hedge fund manager or market strategist making the bearish argument for risk assets. He went through his points and then finished with what he deemed as the final knife to the heart of the bulls - “to top it all off, you are now getting paid 2% in cash. We haven’t seen that level in years.”

Sure. No denying that fact. USD cash has gone from yielding zilch in years following the Great Financial Crisis to a rate where an investor might actually notice the interest in their account. Maybe that bearish pundit is onto something. Maybe investors will pile out of risk assets into cash. Maybe this is the tipping point where investors retreat from out the risk curve back to safe assets.

Then again, maybe not… Like Paul Simon used to sing, I think these bearish forecasters are leaning on those old familiar ways. They are listening to the whispering in their ears about the next 2008 crisis that is just around the corner.

I don’t know if stocks will crash. I am not sure if risk assets are overpriced. But I know one thing - the cash return is not nearly as attractive as these bearish pundits are making out.

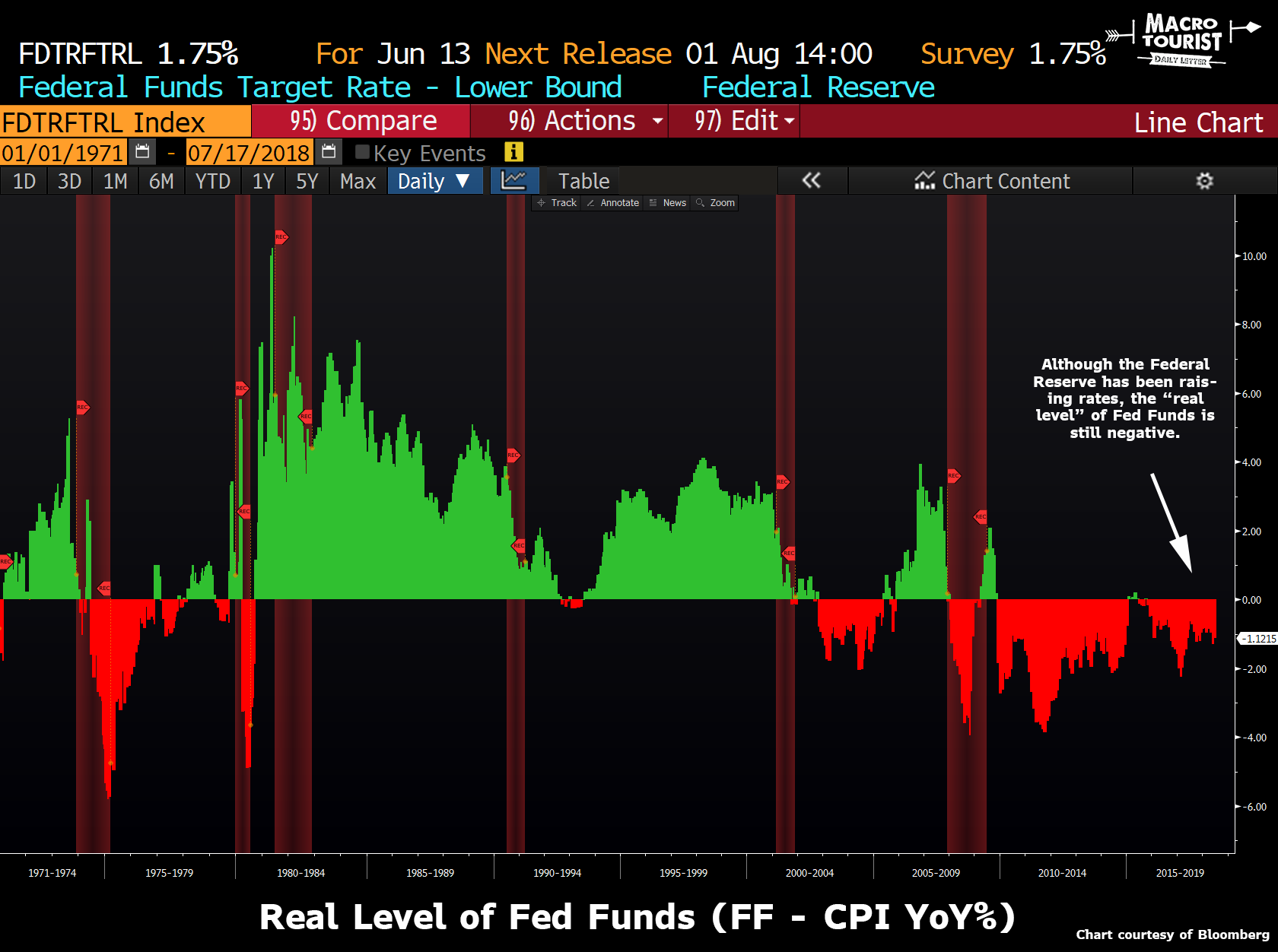

Just looking at cash without taking inflation into account is disingenuous. I know we haven’t had any meaningful inflation for a long time, but that doesn’t mean investors should stop thinking about the real level of interest rates.

Although the Federal Reserve has been steadily raising the cost of borrowing, the real level of Fed Funds is rising nowhere near as quickly as the angst amongst investors.

Accounting for inflation, Fed Funds are still firmly negative! So yeah, maybe nominal short rates are much more positive than a year ago, yet on a real basis, the Federal Reserve is barely keeping up with inflation.

I know, I know - we are late-cycle and the economy is about to roll over… I know all the bearish arguments. Well, based on current fiscal and monetary policy, I just don’t see the ominous storm clouds on the horizon.

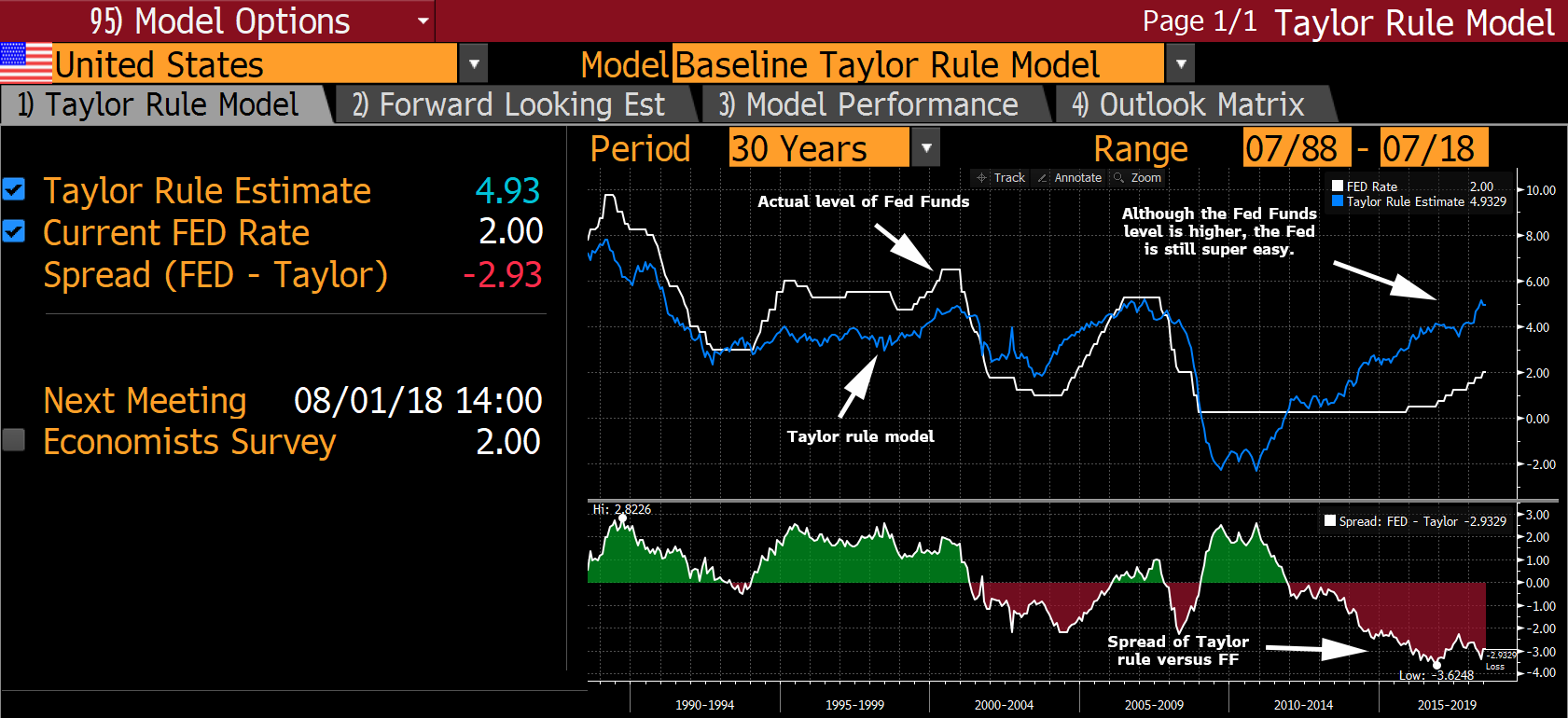

The Taylor Rule is by far from perfect and many economic academics have tried tweaking it to make it better, but no matter which iteration you are partial to, the Federal Reserve is still extraordinarily easy.

The Federal Government’s fiscal policy is as loose as it’s been in ages, and when you combine that with real rates, I just don’t see any reason to assume the economy is about to roll over. Of course, I have learned long ago to never say never. But what always intrigues me is the disconnect between what the market believes and what is the most likely outcome. For these bearish pundits to be correct, it will mean the rate-hike cycle tops out without the real level of Fed Funds ever going positive. Can it happen? Yup - you betcha. Is it the correct bet? I don’t think so.

Even though a 2% return for cash sounds high, too many are assuming we are stuck in a post-GFC world where interest rates hover around zero forever. Meanwhile, in the real economy, these rates are low measured in real terms. The Federal Reserve is still easy after all these years…

Disclosure: None.