S&P 500 Earnings Growth In An Uptrend

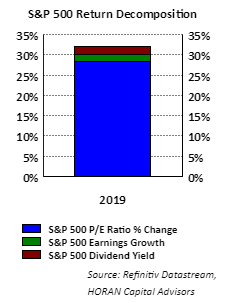

The strong return achieved by the S&P 500 Index in 2019, up 31.5%, occurred in an environment where earnings growth was nearly flat, i.e., up 1.7%. This flat rate of growth in earnings was below analyst expectations at the beginning of 2019. At that time I/B/E/S data from Refinitiv projected 2019 S&P 500 earnings to be up 7.2%. Consequently, the market's strong return in 2019 was driven almost entirely by the increase in the market's price to earnings ratio (P/E.), i.e., multiple expansion. The below chart displays the breakdown of the 2019 market return with the P/E ratio expansion noted by the blue shading on the bar chart.

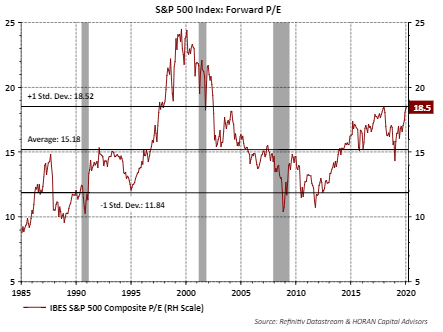

The below chart shows the S&P 500 Index forward P/E ratio where it currently equals 18.5 times. The higher P/E is the result of nearly no earnings growth, yet the index itself rose significantly. Clearly this ratio is elevated and is up from 14 times earnings at the beginning of 2019.

With an elevated market valuation, and I would say fully valued and not necessarily overvalued given the level of market interest rates, favorable stock returns in the coming year need to be driven by growth in earnings in my view.

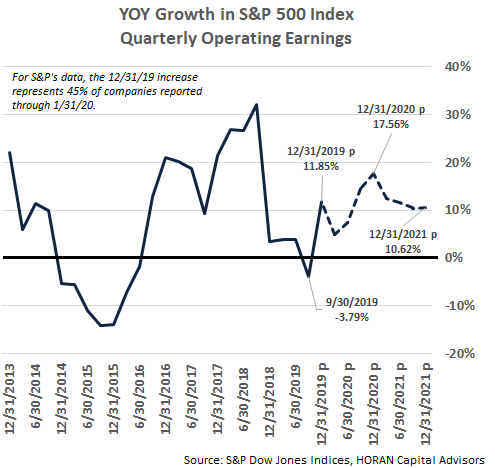

S&P Dow Jones Indices tracks earnings data on a regular basis and below is a chart showing the year over year change in quarterly operating earnings. S&P's January month end report shows fourth quarter 2019 operating earnings are up 11.85% versus the same quarter in 2018. Again, this growth rate represents operating earnings and not 'as reported earnings' which tend to be lower. More information on the difference between these two earnings measures can be found at S&P's site in an article titled, Earnings Per Share 101.

In looking at reported earnings for S&P 500 companies, below is a table comparing 2019 sector returns to YTD 2020 returns. Also detailed in the table are analyst earnings growth expectations for Q4 2019 that were made at the beginning of 2019 and compared to actual results reported to date for Q4 2019. At the beginning of 2019 analyst expected S&P 500 earnings for Q4 2019 to increase 11.8%. With 64% of S&P 500 companies having reported earnings as of 2/7/2020, Q4 earnings are up only 2.3%. Two of the worst performing sectors this year are materials and energy. Both of these sector's earnings results are far below earlier expectations.

Much of a stock's return can be attributed to the company's financial results compared to market expectations. In the above table, the weak earnings results in the energy sector versus expectations, i.e., -40.1%, make comparison for the coming year of 2020 easier. This follows a period where energy stock returns have been weak so might there be opportunities in this space, i.e., buy low? The utility sector is the second highest returning sector so far this year. With a slowing of the growth rate in the utility sector, 2020 returns may become more challenging as utility sector valuations are elevated too.

Factset's Senior Earnings Analyst, John Butters, notes in the Earnings Insight report for the week ending 2/7/2020,

- "What is driving the increase in the earnings growth rate since December 31? In aggregate, positive earnings surprises reported by S&P 500 companies have led to a net $8.5 billion increase in earnings for the index since December 31 (as higher actual earnings replace estimated earnings in the growth rate calculation)."

- "The Information Technology sector is the largest contributor to this increase in earnings, accounting for $5.4 billion of the net $8.5 billion increase (or about 63%). The positive earnings surprises reported by Apple ($4.99 vs. $4.55), Microsoft ($1.53 vs. $1.32) and Intel ($1.52 vs. $1.25) were substantial contributors to the increase in earnings for the index during this time. As a result, the blended earnings growth rate for the Information Technology sector has improved to 5.1% today from -1.9% on December 31."

- "Outside of the Information Technology sector, the positive EPS surprises reported by Alphabet ($15.35 vs. $12.49) and Amazon.com ($6.47 vs. $4.04) were also significant contributors to the increase in earnings for the index since December 31."

Importantly, S&P 500 earnings expectations continue to improve and are accelerating.

The one potentially significant factor that could be a headwind for earnings growth is the impact of the coronavirus on corporate profitability. Many companies have supply chains that begin in and/or run through China and China is limiting manufacturing activity in an effort to stem the spread of the virus. Fortunately, the long term impact of these epidemics has historically had a limited long term impact on the equity markets.

All else being equal then, corporate earnings are in an improving trend. This type of earnings trend is generally favorable for equities and is important that it continues given current stock valuations in the U.S.