Powell Praises The Fed, Discusses The Stars (Literally), Defends Goldilocks

(Click on image to enlarge)

In Jackson Hole, Jerome Powell gave his first speech as Fed Chairman. It was little more than a defense of Fed policy.

In the Jackson Hole Wyoming symposium, Jerome Powell discussed Monetary Policy in a Changing Economy. Here are some snips:

Thank you for the opportunity to speak here today. Fifteen years ago, during the period now referred to as the Great Moderation, the topic of this symposium was "Adapting to a Changing Economy." In opening the proceedings, then-Chairman Alan Greenspan famously declared that "uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape".

In keeping with the spirit of this year's symposium topic--the changing structures of the economy--I would also note briefly that the U.S. economy faces a number of longer-term structural challenges that are mostly beyond the reach of monetary policy. For example, real wages, particularly for medium- and low-income workers, have grown quite slowly in recent decades. Economic mobility in the United States has declined and is now lower than in most other advanced economies. Addressing the federal budget deficit, which has long been on an unsustainable path, becomes increasingly important as a larger share of the population retires. Finally, it is difficult to say when or whether the economy will break out of its low-productivity mode of the past decade or more, as it must if incomes are to rise meaningfully over time.

- With the unemployment rate well below estimates of its longer-term normal level, why isn't the FOMC tightening monetary policy more sharply to head off overheating and inflation?

- With no clear sign of an inflation problem, why is the FOMC tightening policy at all, at the risk of choking off job growth and continued expansion?

These questions strike me as representing the two errors that the Committee is always seeking to avoid as expansions continue--moving too fast and needlessly shortening the expansion, versus moving too slowly and risking a destabilizing overheating.

I see the current path of gradually raising interest rates as the FOMC's approach to taking seriously both of these risks. While the unemployment rate is below the Committee's estimate of the longer-run natural rate, estimates of this rate are quite uncertain. The same is true of estimates of the neutral interest rate. We therefore refer to many indicators when judging the degree of slack in the economy or the degree of accommodation in the current policy stance. We are also aware that, over time, inflation has become much less responsive to changes in resource utilization.

While inflation has recently moved up near 2 percent, we have seen no clear sign of an acceleration above 2 percent, and there does not seem to be an elevated risk of overheating. This is good news, and we believe that this good news results in part from the ongoing normalization process, which has moved the stance of policy gradually closer to the FOMC's rough assessment of neutral as the expansion has continued.

Shifting Stars, Nautical Metaphors, Other Nebulous Concepts

Powell also discussed navigating by the stars, the ridiculous Phillips curve, the natural rate of inflation and other nebulous ideas.

The FOMC has chosen a 2 percent inflation objective as one of these desired values. The other values are not directly observed, nor can they be chosen by anyone.

These fundamental structural features of the economy are also known by more familiar names such as the "natural rate of unemployment" and "potential output growth." The longer-run federal funds rate minus long-run inflation is the "neutral real interest rate." At the Fed and elsewhere, analysts talk about these values so often that they have acquired shorthand names. For example, u* (pronounced "u star") is the natural rate of unemployment, r* ("r star") is the neutral real rate of interest, and Π* ("pi star") is the inflation objective. According to the conventional thinking, policymakers should navigate by these stars.3 In that sense, they are very much akin to celestial stars.

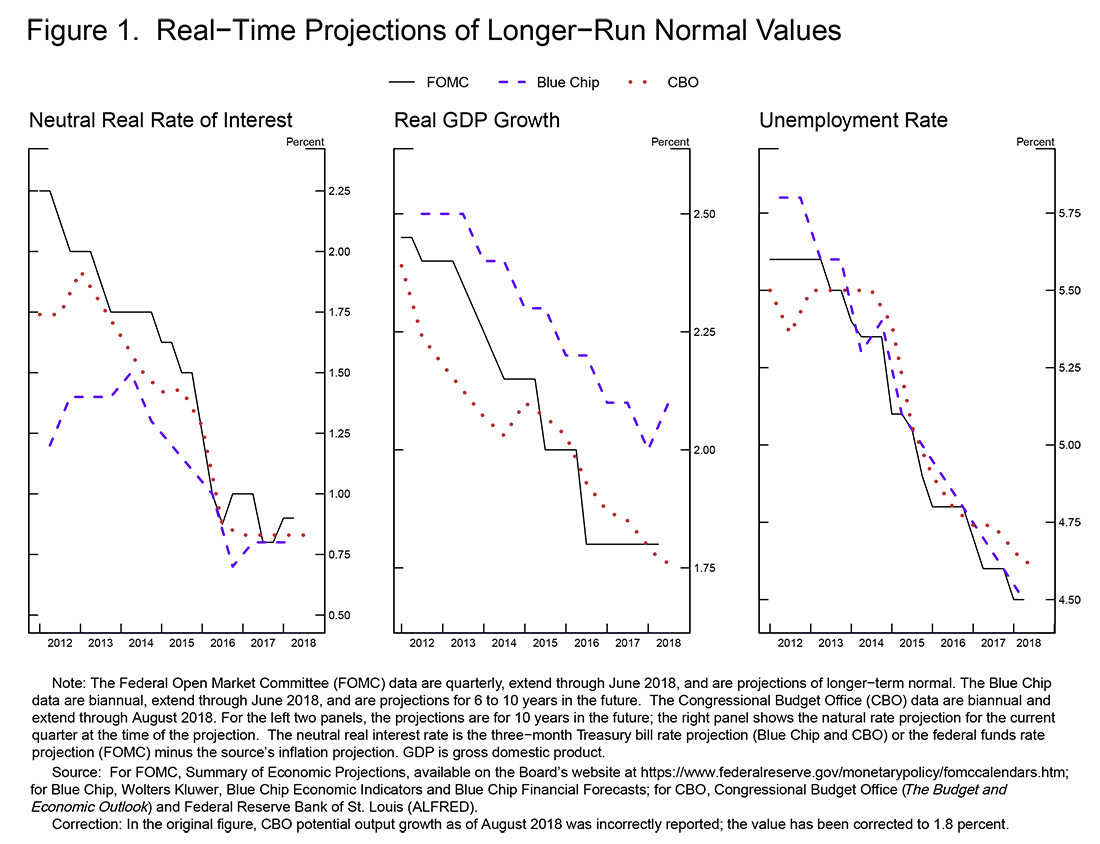

In December 2013, the FOMC began winding down the final crisis-era asset purchase program. Asset purchases declined to zero over 2014, and in December 2015, the FOMC began the gradual normalization of interest rates that continues to this day. As normalization has proceeded, FOMC participants and many other private- and public-sector analysts regularly adjusted their assessments of the stars (figure 1)

Assessments of the values of the stars are imprecise and subject to further revision. To return to the nautical metaphor, the FOMC has been navigating between the shoals of overheating and premature tightening with only a hazy view of what seem to be shifting navigational guides. Our approach to this challenge has been shaped by two much discussed historical episodes--the Great Inflation of the 1960s and 1970s and the "new economy" period of the late 1990s.

Natural Rate of Unemployment

(Click on image to enlarge)

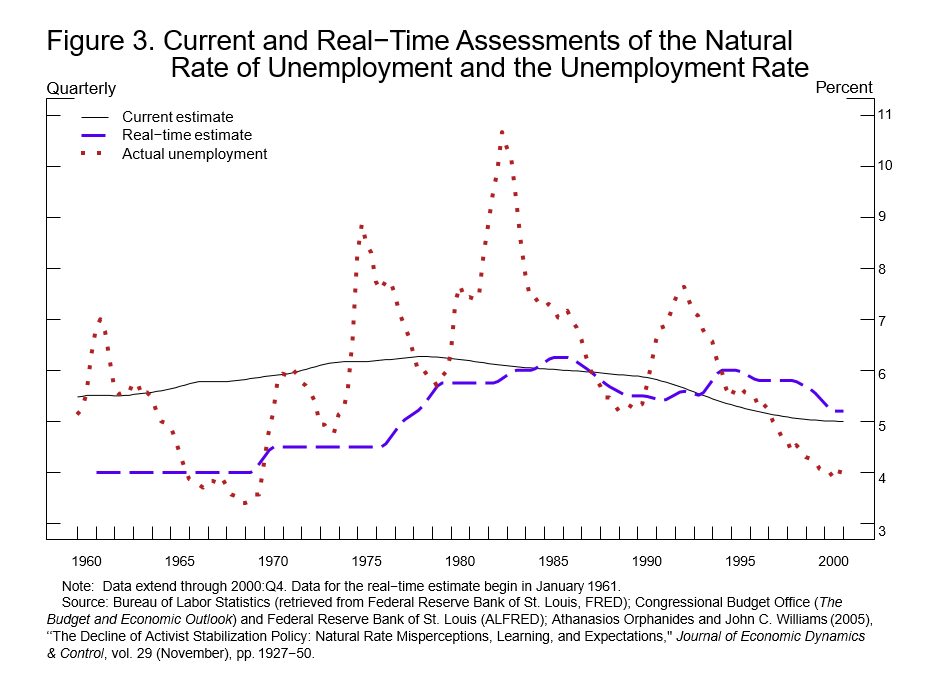

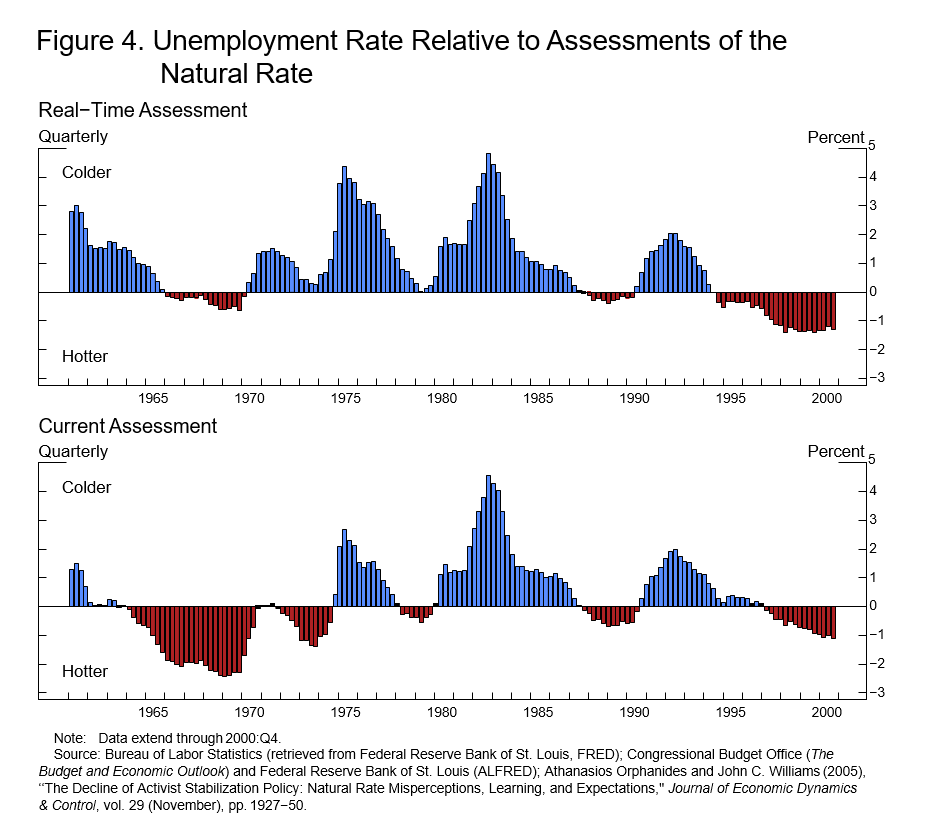

Figure 3 compares the CBO's current view of the natural rate of unemployment in that era with an estimate by Athanasios Orphanides and John Williams of the rate as policymakers perceived it in real time. From 1965 to the early 1980s, this real-time estimate of u* was well below where hindsight now places it. The unemployment rate over this period was generally well above the real-time natural rate, and contemporary documents reveal that policymakers were wary of pushing the unemployment rate even further above u* (figure 4, top panel).7 With the benefit of hindsight, we now think that, except for a few years in the mid-1970s, the labor market was tight and contributing to inflation's rise (figure 4, lower panel).

Powell claims "shifting stars help explain the performance of inflation under Alan Greenspan, which many had seen as a puzzle."

It is now clear that the FOMC had placed too much emphasis on its imprecise estimates of u* and too little emphasis on evidence of rising inflation expectations. The Great Inflation did, however, prompt an "expectations revolution" in macroeconomic thinking, with one overwhelmingly important lesson for monetary policymakers: Anchoring longer-term inflation expectations is a vital precondition for reaching all other monetary policy goals

Whereas during the Great Inflation period the real-time natural rate of unemployment had been well below our current-day assessment, in the new-economy period, this relation was reversed (figure 3).

Translation

We do not know where the stars are and nor does anyone else. Powell even admitted as such.

Yet, the Fed thinks a "2% rate of inflation" is a fixed star. It never moves.

Of course, the Fed does not know how to measure inflation in the first place. Powell praised Greenspan, but he never discussed the Greenspan Fed housing bubble.

Heck, Powell did not mention the word "bubble" at all in any context.

So here we are, navigating by moving stars with a constant eye on the North Star, a 2% inflation target that is our guiding light.

Yes, it's absurd.

Disclosure: None.

{kind=link}

{kind=link}

{kind=link}