Just Who, Exactly, Is So Optimistic?

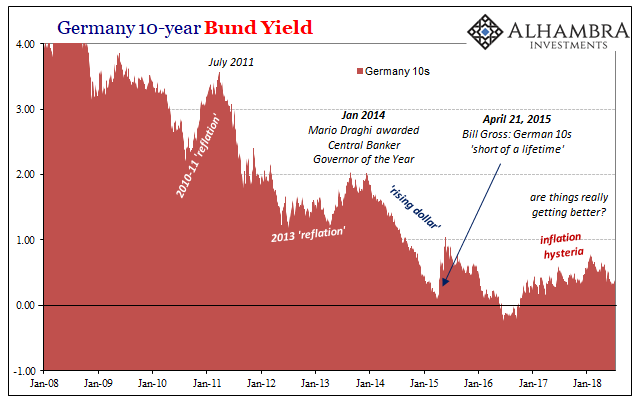

BNP Paribas is apparently calling for an epic rout in German bunds. According to Bloomberg (who else?) it’s a mini-revival of Bill Gross’ ill-fated tweet advertising the “short of a lifetime.” In April 2015, the man many called the bond king said it was going to be better than the pound in 1993.

Gross: German 10yr Bunds = The short of a lifetime. Better than the pound in 1993. Only question is Timing / ECB QE

— Janus Henderson U.S. (@JHIAdvisorsUS) April 21, 2015

Gross advertised waiting until later in 2016 before transacting, though that wasn’t really any better. Bund yields did rise toward the end of that year, starting out from negative rates, but they haven’t yet gotten too far. Now this year yields are on track to be lower all over again. Who keeps buying all these bonds?

Banks especially those in Europe remain undeterred. BNP Paribas is hardly unique in its bond bear stance. They are all bond bears, every single firm has rates higher in 2018. This one firm only stands out for its recent prediction for how far this presumed rout will hike rates (in a way the Fed can only dream of). Behind each of these negative bond predictions lies the same rationale:

…suggesting bunds will slump before the end of the year as the euro-zone economy picks up steam.

Never mind the recent bout of haranguing weakness, it’s all transitory or decoupling, right?

What we see on display again is some seriously misleading context. The Bloombergarticle treats as is convention the published forecast from analysts as if it was the same position taken by BNP Paribas throughout the bank.

In the mainstream, the answer to constant bond buying is the ECB. What about UST’s, then? Eurodollar futures? The mainstream, as usual, is wrong.

This is yet another uninvestigated topic that requires serious attention at some point. It’s a bit further down the list of priorities, somewhere well after getting central bankers up to speed about the 1960’s. Still, it’s an important enough subject given the chasm of mistrust that grows every day after all these banks claim recovery and then in the aggregate trade it very differently.

The phenomenon is not new, and it has been confirmed to me personally on several occasions. It was something the FOMC raised in its discussion before there ever was a crisis. All the way back more than eleven years ago in March 2007, Bill Dudley (who else?) was searching for ways to dismiss the negative signal produced by eurodollar futures (what else?).

The “banks” were all as positive on the economy at that time as the Federal Reserve was (pure confirmation bias, since Economists at the big banks all start from the Fed’s forecasts to produce their own). When pressed on the alarming difference between the market position and what “the banks” were supposedly saying, Dudley uncorked the uncomfortable truth:

MR. DUDLEY. Well, another explanation is that the economists who make the dealer forecasts are not the traders who execute the Eurodollar futures positions.

In the mainstream sense of it, dealer banks were positive about things in early 2007 (and later 2007 and early 2008, for that matter) but betting internally coming from starkly different perceptions and projections. Which one, then, is the bank’s real position if it says one thing in public but does the opposite or substantially so in markets?

It’s a rhetorical question. We hear the unbreakable optimism of bank Economists and analysts year after year after year each one echoing the unbreakable optimism of central bankers year after year after year. And the whole time people wonder, who in the hell is buying all these eurodollar futures, German bunds, and US Treasuries, keeping rates down year after year after year? Who would ever defy so much uniform sunny opinion being put out by the bank sector?

The banks. That’s who.

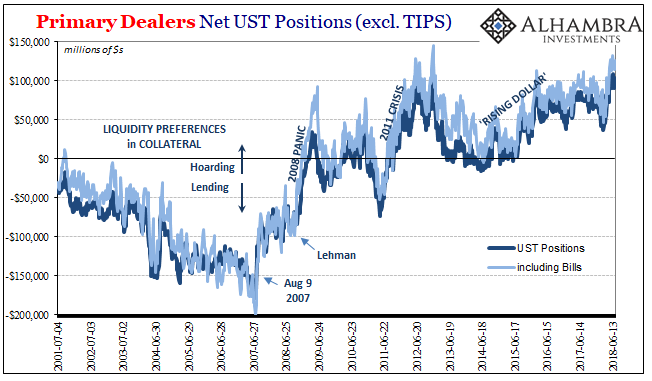

Sometimes it’s straight pessimism but most times it’s one element of liquidity risk or another, the very things no central banker takes any real interest in. Like collateral shortages (May 29).

Germany’s 10s had reached a high (yield) of no more than 79 bps earlier this year. In the middle of May, they were down again (price, meaning up in yield) reaching 65 bps in yield on May 18. That’s the day after UST 10s put in their multi-year high of 3.11%.

What followed was a huge buying spurt that crested on through May 29 – global collateral call. Who was it that was calling, and being called, on collateral?

Not Economists.

Disclosure: None.