COT Black: Term Oil Means Turmoil

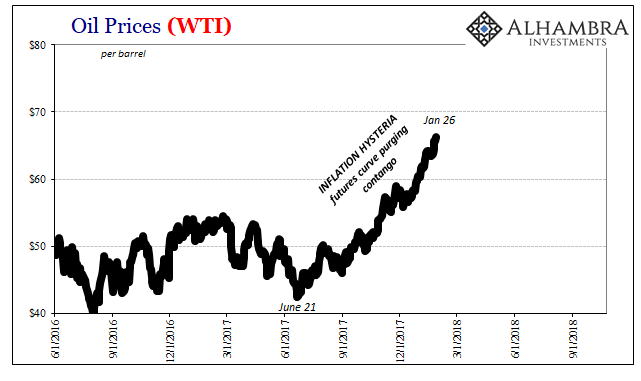

Inflation hysteria was as much crude oil as anything else. After all, it was the sudden spike higher in oil prices that would eventually push the US CPI, PCE Deflator, Europe’s HICP, and even Japan’s moribund inflation index. Central bankers were giddy, as was mainstream commentary extrapolating these trajectories into actual economic acceleration. For a time, even the unbreakable skepticism of the global bond market was set aside.

If there was to be something real behind globally synchronized growth, oil sure would have pointed the way. After the economic disaster of 2015-16, demand not crude supply glut, for economic normalcy to be possible for the first time in a decade the energy sector would first have to reset.

It did, enthusiastically. Contango was purged from the futures curve indicating that supply and demand for oil was equalizing. Since it hadn’t been a supply glut, rising demand was as visible as it was welcoming.

Markets ran into a bit of a bump in the road to globally synchronized growth in late January. On January 29, stocks were liquidated and the whole global economy shook from the earthquake (in global money, not the share liquidations which merely registered one effect). There would be another perhaps greater aftershock on May 29.

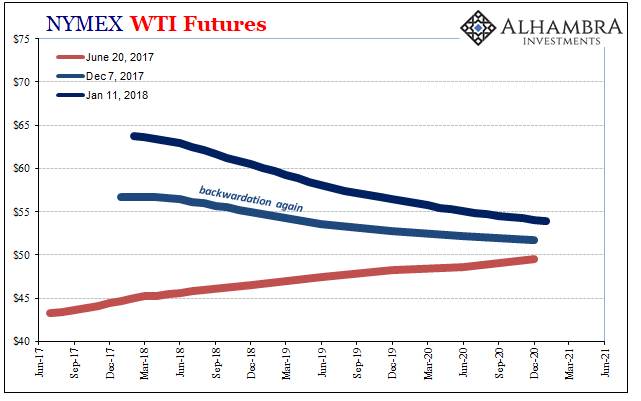

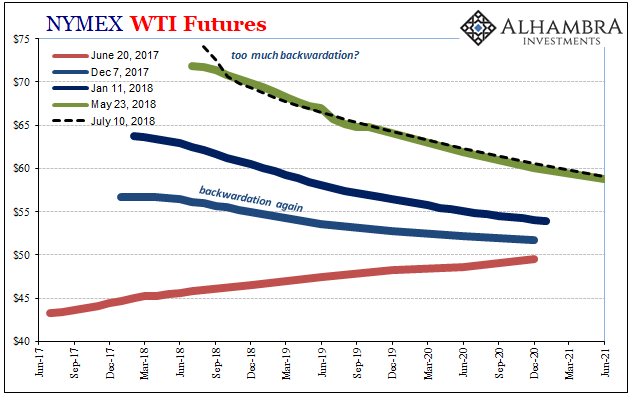

The oil patch, however, appeared unconcerned at least in terms of oil prices and backwardation. Crude benchmarks continued to rise despite growing nervousness elsewhere. And backwardation would by July become extreme.

The Commitment of Traders (COT) report tells a little different story behind all that. The futures market did not ignore January 29. Rather, the oil space processed the unfolding deflation a little differently at least as far as timing.

Money Managers had been record long, by a long shot, the week of January 30. The bet on globally synchronized growth was intense, the market corroboration of the coming global recovery the world sorely needed; central bankers most of all for reasons of inflation.

But WTI wouldn’t get back anywhere near $100 because since the week of January 30 Money Managers have become less passionate about the idea. And they had been balanced all along by Swap Dealers, both in providing liquidity for those building long positions but also clearly an additional bet against them.

As economic concerns mounted, this renewed “overseas turmoil” no one can adequately explain, the record long has faded often quickly. The shorts piled up against it have receded, too, but not nearly to the same extent. Where managers have shed 283k contracts (fewer net long) since the week of January 30, dealers have come back just 196k (fewer net short).

It is reminiscent of mid-June 2014 when a then-record net long for money managers began to disappear while at the same time dealers started covering their shorts. The only thing missing to this point in 2018 is the futures curve indicating term physical shifting as well as dollar imbalance. Meaning, an alarming flip back to contango in the curve.

It’s not absent any longer. During this latest oil selloff that began on October 3 the futures curve, like the eurodollar futures curve, is now twisted the wrong way.

Why October 3? On the surface, it wouldn’t seem a likely candidate for turning the very basis for the reflation story upside down. That was the day of that big BOND ROUT!!!! in especially US Treasuries. The yield on the 10s spiked by more than 12 bps in just the one session. This was supposed to be consistent with more of what Jay Powell has been talking about, higher inflation because of roaring economic demand.

That particular session, however, didn’t feel at all like the usual reflation BOND ROUT!!!!, though. There was more to it, more panicky and disorder. I’m speaking about gut feeling more than numbers and narrative. I wrote on October 2:

For now, it’s another warning about how things are getting serious, and just getting started. [S]ince August 9, 2007, the dollar will eventually come for everyone. Eurobonds as well as eurodollars.

If only globally synchronized growth and worldwide recovery had been a real thing.

This warning was, for once, Indian rather than Chinese. A major shadow financier in the Indian system had blown up and been bailed out by the state. IL&FS had been borrowing heavily in offshore dollar markets for years, especially during the binge of the last few. Bailouts are as unpopular there as they had been here, and yet a struggling Modi government that had pledged not to do it ended up doing it.

That’s the main thing about bailouts. It’s not that governments are rescuing their cronies, which in a lot of cases they are, it’s the unusually clear signal for markets about how bad things must have become for cronies to receive such unequivocal public support.

But that was just India. Why would it matter, on October 3 and the UST rout, no less? From last week:

If India suffers the tidal wave of deflation as one of the last untouched inland economic outposts, then the worldwide economic “L” will truly be global. It would finally be synchronized, but in every way abhorrent to the original idea.

This is why, I believe, India matters in 2018 whereas it might’ve skirted along under the surface three years ago. People rightly focused on China in 2015 since the Indian economy remained largely stable. If India gets the worst of the eurodollar, too, then there is nothing left but risk.

I also think that’s what hit global markets on October 3. The IL&FS fiasco forced Indian authorities, or financial agents acting on their behalf, to pony up and subsidize that country’s more limited “dollar short.” That was the day the UST market experienced its last “big” BOND ROUT!!!!, the one that took the 10s yield to its highest since 2011. Rising risk surely spread to other susceptible eurodollar participants.

Most of the decline in the net long of money managers has taken place since the week of October 3. Between the week of September 4 and October 2, that position was reduced by a little more than 48k contracts, from net long 377k to 329k (already inconsistent with reflation). Between the week of October 2 and the latest figures for last week, the net long has collapsed by 130k contracts, now underneath 200k total for the first time in more than a year.

If India is being driven down by this latest eurodollar squeeze, a fourth in a series dating back to August 2007, you can understand why the oil futures curve has shifted back into contango. There is rising risk to demand therefore undercutting everything; from normalizing oil supply and demand to financing risk (contango is also a negative “dollar” indication) to the general collapse of the idea behind globally synchronized growth.

It may be that the reappearance of contango ultimately proves to be nothing more than a transitory factor that the market will sort out in good time. Then again, it might be like the summer of 2015.

Contango is term oil. The comeback of contango right now, at this critical juncture, is turmoil.

Disclaimer: All data and information provided on this site is strictly the author’s opinion and does not constitute any financial, legal or other type of advice. GradMoney, nor Jennifer N. ...

more