Collateral Silos And The Deflationary Gold Rush

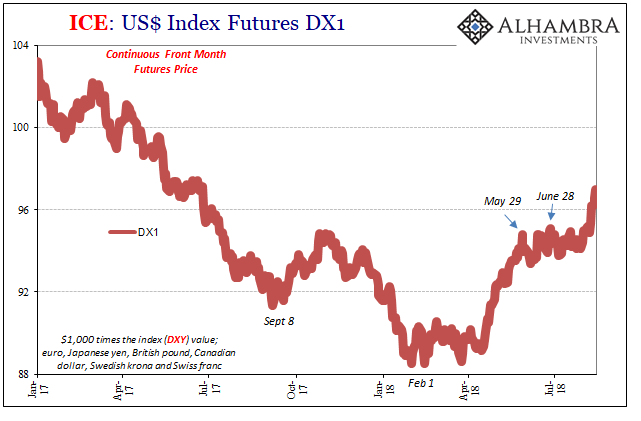

It was never really all that much. The best that might have been said was that it was a pause in the building of renewed deflationary pressures. The dollar had “risen” again especially in April and May but then traded sideways through July. It wasn’t a rebound or even much that was positive, just less immediate heaviness.

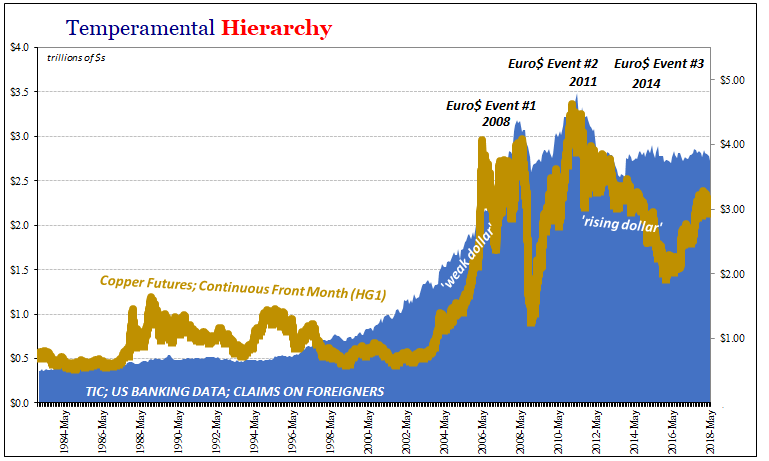

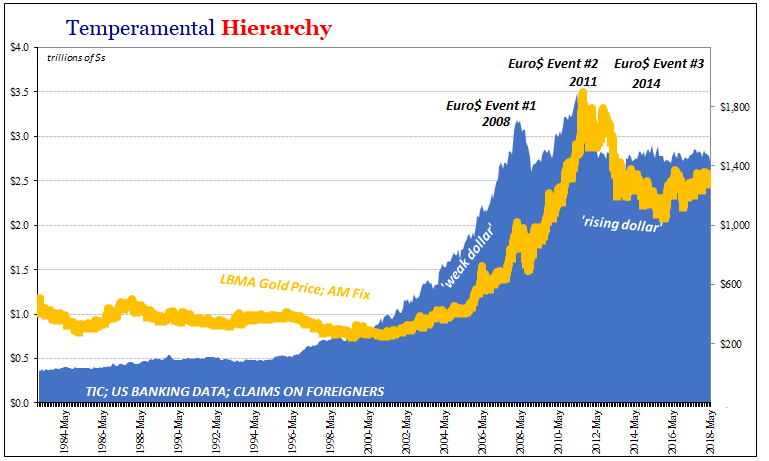

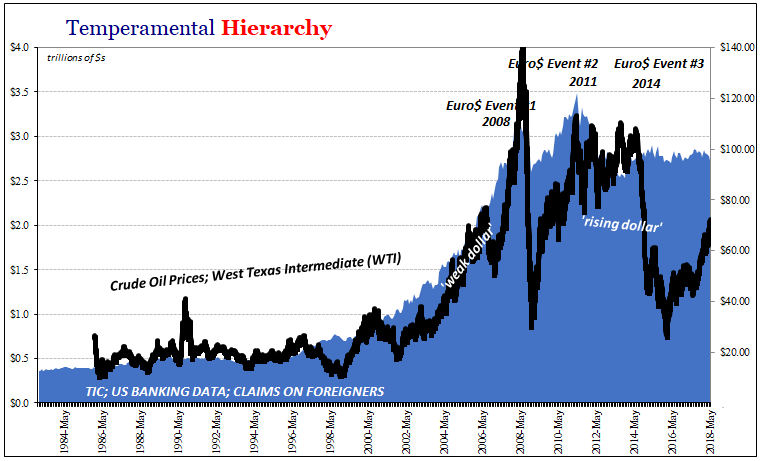

That appears to be over with now in August; always August. The dollar is on the move which means the eurodollar is deficient. The squeeze is back and it is being felt almost across the board. Copper is down again as is gold. The metals are and have been for years, quite clear as to what all this is.

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

QE has merely clouded the issue. People believe central banks have printed money so how can there be any small levels of deflation let alone year after year of it? You hear it all the time how monetary officials have “flooded” the world with liquidity, yet when you step outside that purposeful narrative you see it cannot have been true.

That’s not enough, however. We want to know how and why. Unlike central bankers, we strive to be competent about money and therefore the economy. It is the Ben Bernanke’s of the world who are content to draw simple diagrams and believe in singularly isolated correlations without investigating the actual mechanics behind this world.

(Click on image to enlarge)

(Click on image to enlarge)

One thing we do know is that gold is leaving the custody of the Bank of England again. It is a pretty reliable signal that commercial banks are using the metal for other means. What other means? Collateral as last resort.

It is one part for the mechanisms of deflation that have on and off plagued the global money system since it broke down eleven Augusts ago. A credit-based monetary system requires credit-based institutions to do credit-based things. In the modern version, it is heavily reliant upon interbank funding.

This type of management system is quite different than its depository ancestor. These interbank markets are really the means for redistributing monetary characteristics wherever market signals suggest they are demanded and often necessary. Sometimes that means cash, sometimes more esoteric forms of liquidity like collateral.

(Click on image to enlarge)

The most obvious strain in this area has been its past relationship to subprime and mortgages. That is, the list of acceptable high quality or pristine securities has been dramatically pared over the last decade plus. At one time before August 2007, the repo market was overflowing with MBS and agency paper as well as UST bills. It’s not any longer, those former two have been largely expunged.

(Click on image to enlarge)

While that presents an overarching bottleneck, this doesn’t fully explain renewing difficulties along the way. If there is a cycle to these things, reflation to deflation, then there has to be something else going on beyond the redefinitions of pristine. Those are mostly in the past, the last big alterations to the list around 2011.

The collateral “list” is only part of the repo story. We might tend to think of money markets as they were before the crisis. Prior to the panic period, they operated in what seemed like a monolithic, seamless whole with the central bank in the middle. What the breakdown beginning in 2007 proved was that it was a literal breakdown; money markets fragmented, a Humpty Dumpty sort of situation where no matter what all the central bank’s horses and men tried they couldn’t put it all back together.

That was true on the inside of them as often as between different ones. Taking the repo example, the precrisis operative conditions might have made it seem as if there was some giant singular pool of collateral that might be accessed easily, and cheaply, on demand. That’s not really how it worked.

(Click on image to enlarge)

Rather, there were and are various separate pools of collateral that only became available through some concerted effort. Given the name collateral silos by Manmohan Singh years ago, these are static portfolios that in traditional money systems mean very little. Insurance companies like AIG had some of the largest otherwise untapped holdings of securities that for an enterprising financial firm represented tremendous potential.

Systemically, there is a benefit to this kind of redistribution so long as there are realized risks (financial discipline). In the building eurodollar system, these were largely absent (perceptions of only risklessness, perpetuated by things like the mythical Greenspan put).

These idle securities might, therefore, be “lent out”, meaning that collateral could flow from collateral rich pools like pension and investment funds or prime brokers (including those like MF Global who had access in arcane contracts to customer assets) to collateral poor pieces where funding risks were primary considerations.

(Click on image to enlarge)

There were money dealers who were responsible for this high degree of collateral redistribution. Banks and other financial firms found profit in an almost constant flow of thermodynamic money chaos. Based on various spreads and arbs, the money dealers would ensure the system operated more smoothly. It wasn’t perfect by any means, but by and large, everyone came to the conclusion that there was little risk in repo because of these institutional dealers.

(Click on image to enlarge)

And it wasn’t always just straight up securities lending, either. There were a range of services these dealers provided so as to match demand for collateral with the possible supply. At times, it even seemed economical to manufacture supply. One of the more onerous, and unwise, activities was collateral transformation – the very thing that nearly ended AIG (it wasn’t CDS, AIG’s last liquidity gasp was due to its securities lending business).

(Click on image to enlarge)

In other words, there are only static pools of collateral that require very real effort to mobilize particularly if conditions change. Money dealers are the necessary component to redistribution, including transformation which is both the manufacture of collateral as well as its reallocation.

Take away the money dealers, and the potential for periodic collateral disruption rises. If dealers become shy for whatever reasons, such as those that squeeze the dollar higher, it stands to reason that what used to be taken for granted as riskless redistribution could become frowned upon by these essential mechanisms for animation.

(Click on image to enlarge)

Over these years of “recovery”, the business has become even more complicated by the changes to the silos themselves. No longer are insurance companies so willing to engage with dealers even when dealers are willing and able to pay for securities. In their place, the largest portfolios often belong to official institutions such as the Federal Reserve and the PBOC.

The Fed, for its part, has its reverse repo program which theoretically is a way for anyone to tap SOMA for UST’s if the need should arise. It has never once worked out that way regardless of any outside conditions, showing that bottlenecks inside the collateral system are often two-way in today’s eurodollar stunted world.

Thus, one part of the deflationary sequence is the same as all the others. In other words, in the collateral system, the shyness or even absence of dealers works to defeat good flow and function in the same as it does in other parts like FX or general liquidity.

When we say balance sheet capacity is in short supply, we mean the effects of it on everything including where you might not think it a requirement. Without eurodollar capacity, all the things that used to make it work including collateral redistribution tend to break down.

Central banks aren’t central. Dealers and their capacities have been instead as long as the eurodollar has been the dominant monetary format in the world. In other words, a half century or so (Great Inflation, Great “Moderation” that wasn’t so moderate, and now the ongoing Great “Recession” that hasn’t been a recession).

A monetary breakdown, especially across so many key components, is textbook deflation. It may not happen all at once, fickle as banks and dealers might be at times, but by and large, that’s the basis for these reflation/deflation cycles.

Gold’s down again, and the dollar is up. Eurodollar squeeze or economic boom?

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

Disclosure: None.