Yet Another Lesson In Nightmares

I don’t know how many different ways I can write this. Reserves are not insurance against monetary reversal, they are the calamity. If you have them, that only means you have a problem. And if you have a lot of them, well.

The Financial Times yesterday writes again about Argentina. No matter what’s thrown at that country, nothing will staunch the monetary bleeding. The following is a good enough summation for 2018:

Argentina may have reluctantly fallen back into the embrace of the International Monetary Fund, but the biggest aid package in history has not managed to inoculate the country from an onslaught of market pain.

But why? The global economy is booming, or at least on the verge of one. That’s what everyone says. “They” made it their entire point to add “synchronized” to the narrative for a reason. This one unlike the other false dawns wasn’t going to leave anyone behind.

Except maybe Argentina. And Brazil. Turkey. Indonesia. India even. And then China. As I wrote yesterday, “If things are going so well, why aren’t they going so well?”

The process of recognizing an “L” isn’t straightforward. Nobody believes in them, not at first. We are all taught that recessions are temporary and that when they end growth simply resumes as a matter of science. That’s what everyone keeps expecting after each downturn, no matter how severe.

In fact, the worse the contraction the greater you think the recovery will have to be. The world is conditioned to expect just that sort of symmetry. Economic history, at least in the postwar era, is conclusive on that score. What goes down must come back up.

One reason for the pervasiveness of the belief is modern Economics. We are taught that Economists have it all figured out. They learned from the big mistakes of the past so that they would never be repeated. The global monetary disruptions that were almost always the cause of worldwide hardship just don’t happen anymore.

Except one did. And another. Then another.

Money and currency markets are discounting mechanisms. Once it looks like a good bet that the worst has passed, or is about to, it is on to the future. If the common belief is grounded in symmetry the expectation is that over time the economy will live up to it. That’s reflation, the precursor to recovery.

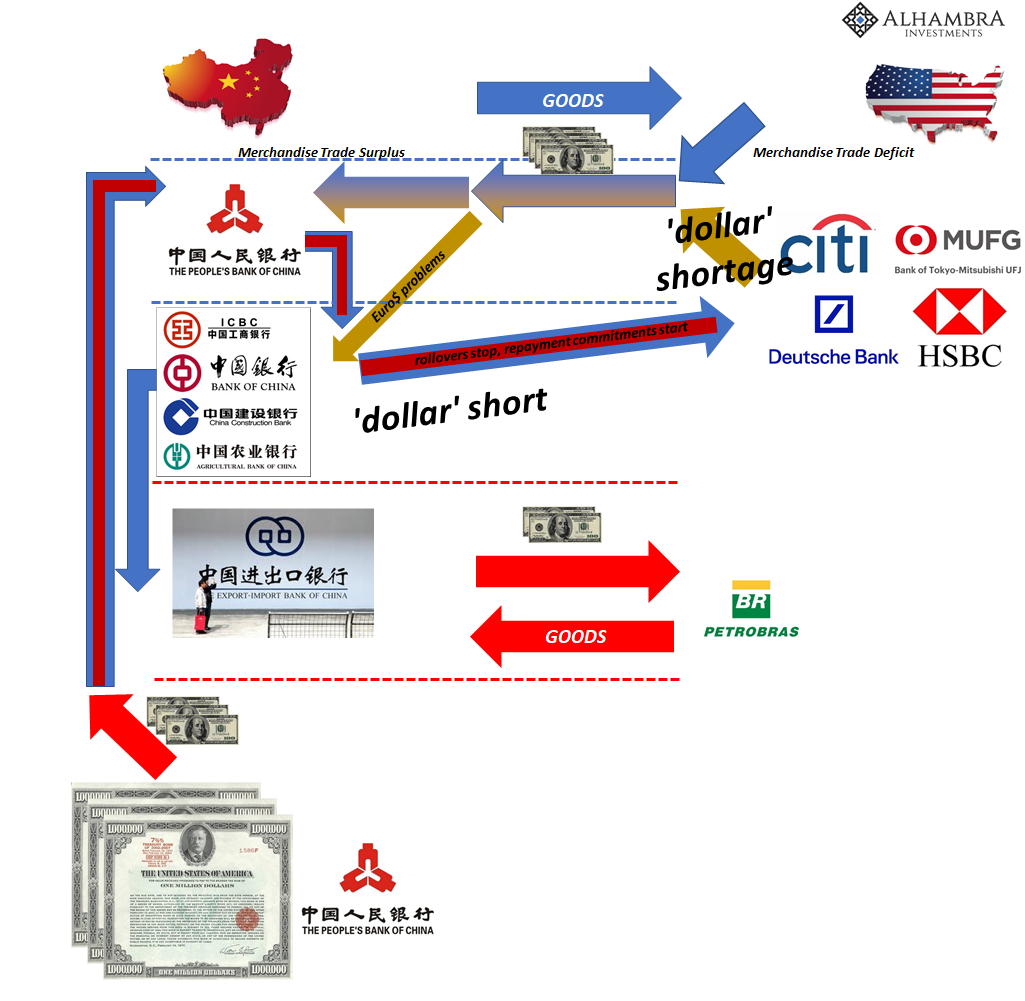

It is here when Argentina was the world’s unanticipated darling. In early 2016, they went to the Eurobond market to fill up on dollar reserves. Borrowed “dollars” from bonds isn’t a perfect substitute for prior “dollars” obtained via banks. In some ways, it can be worse (inflexible).

Giving up on reflation is almost unnatural. It requires substantial evidence whereas reflation requires almost none. The very idea of symmetry is reflexive; asymmetry is repellent and abhorrent. That’s why these upturn narratives can last on only mainstream rhetoric. It’s like an inferential statistics test where symmetry is the null hypothesis which requires a high standard of data and confidence in order to reject it.

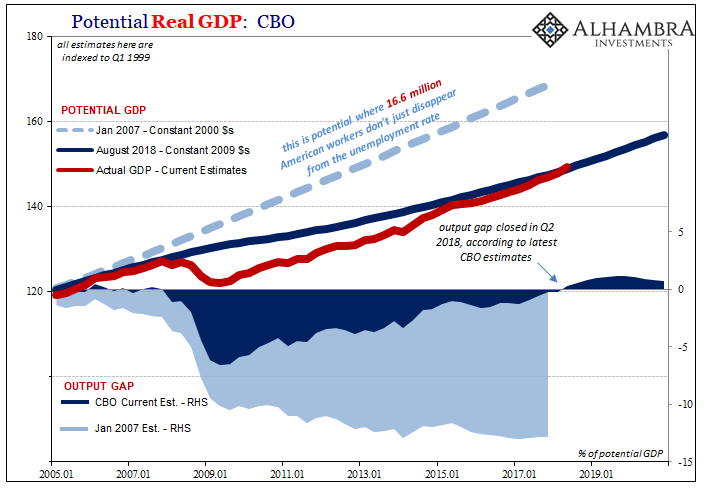

Time and again we see that symmetry no longer holds, not since August 9, 2007. Even the current so-called boom in the US is asymmetric, as the CBO quietly confirmed what Jay Powell is really talking about. Powell sees an end to the output gap, but which one? Not the one everyone thinks, at least outside the long ends of the UST or eurodollar curves.

It wasn’t the Great “Recession”, it was the Great L. And the “L” is greatest where the eurodollar infiltrated the most. This is still the nightmare, the one I wrote about to begin that crucial month of September 2015:

There is another way to look at it, and this is really the nightmare scenario and not just for China but everywhere. By requiring private firms to deposit forex (mostly dollars) in October the PBOC might be planning for the worst case. It has, by now, appreciated just how limited actual mobilization of all those “reserves” actually can be, as even doing heavy intervention so far was largely ineffective despite all the convention about having all those protective reserves in the first place – the yuan still broke and China fell into the crosshairs of open disorder. And that is the larger point and confluence, where the PBOC “reserves” may contain further disruption if they aren’t properly calibrated (and they never are; again Brazil, Indonesia and the rest) just as the rest of the world wakes up to the fact that all those reserve piles were instead of being insurance against the worst case are the very problem itself – wholesale exposure as the decay in wholesale eurodollar reaches almost predetermined amplification.

It’s like Hollywood quicksand. The more you struggle, the worse it gets. Argentina received the largest IMF bailout in its history, achieving nothing of substance for the nation – except to have painted a target on it.

Quite simply, if you built up a lot of “reserves” however they may have been obtained, you actually built up your “dollar short.” That’s fine when “dollars” are plentiful or at least minimally sufficient as they might be when the rhetoric of reflation is sweetest. When it gets back to the “dollar shortage”, on the contrary, there aren’t any good options.

This is the bottom of the “L.” Argentina is just one of many examples. A final thought from FT:

Yet the recent turmoil in emerging markets has since muddied the outlook and called into question how Argentina will meet its $82bn financing needs for this year and next, while navigating a looming recession and rising consumer prices ahead of a presidential election in 2019.

It’s not really what people were imagining in 2017 for globally synchronized growth in 2018. Looming recession? Not possible, even in Argentina.

Then again, imagination is the one thing really lacking as conventions fall apart under the weight of one lost decade turning toward a second. Good thing this all nothing more than T-bills.

Disclosure: None.