We Now Have An ETA When The Biggest Bond Bubble In The World Will Burst

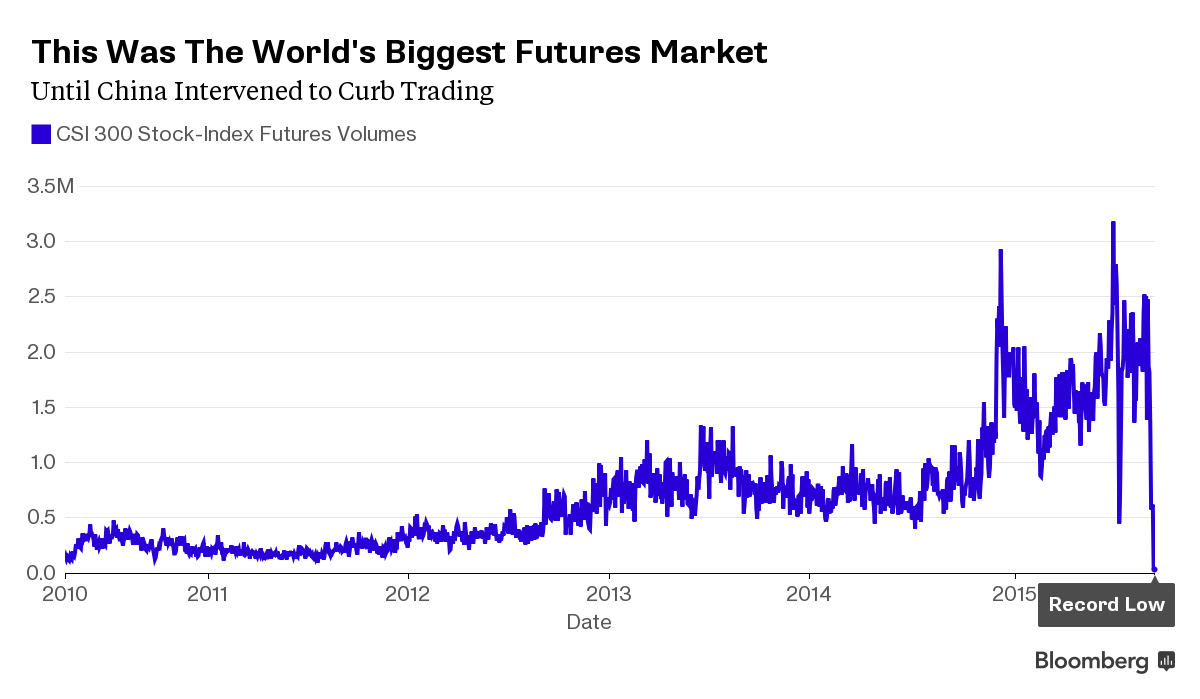

Together with Greece briefly soaring to prominence over the summer (only to fade into perpetual obscurity in its new role as Germany's certified Mediterranean colony), the biggest event of this past summer - before the EM capital flow/Fed non-rate hike fiasco - was the rapid boom and spectacular bust of China's equity market, which culminated not only in arrest of sellers, but in the hiking of futures margins so high that nobody actually trades in China any more.

However, China's equity bubble was just the beginning. As we showed in "If You Thought China's Equity Bubble Was Scary..." even after the Shanghai Composite crashed in the fall, Chinese bonds spreads continued plunging oblivious of everything that was taking place in the stock market.

This historic bond bubble is paradoxical for the simple reason that China's credit fundamentals have never been worse, and as we further showed, as a result of the ongoing collapse in commodity prices (which today's Chinese rate and RRR-cut will have absolutely no impact on), more than half of commodity companies can't generate the cash required to even pay their interest, a number which drops to "only" a quarter when expanded to all industries.

"The equity rout merely reflects worries about China’s economy, while a bond market crash would mean the worries have become a reality as corporate debts go unpaid," said Xia Le, the chief economist for Asia at Banco Bilbao. "A Chinese credit collapse would also likely spark a more significant selloff in emerging-market assets."

"Global investors are looking for signs of a collapse in China, which itself could increase the chances of a crash... This game can’t go on forever."

They will find it soon, because while China may have managed to once again kick the can on its most recent default when state-owned SinoSteelfailed to pay due principal and interest this Tuesday only to get a quasi-government bailout, every incremental bail out merely forces even more cash misallocation and even more foolish "investments" into this high risk asset class as investors ignore any concerns about fundamentals, assuming instead that the government will always bail them out.

The problem with that is that as BofA's David Cui notes today, China's bond market is the epitome of a "potential source of financial instability."

Here is Cui:

Our analysis shows that:

- the bond market is clearly not pricing default risk properly;

- the bond market has taken a few SME bond defaults in stride and seems to be counting on bail-outs of the few SOE bonds that are reportedly facing default risk; and

- leverage in the bond market is rapidly building up.

But most importantly, Bank of America has now given a time frame in which China's bond market will blow up, resulting in far more dire consequences that the equity bubble bursting this summer.

On the current trajectory, we doubt the market can stay stable beyond a few quarters, especially if some SOE and/or LGFV bonds indeed default.

Why it will be far more dire? Because as of this moment China has between $25 and $30 trillion notional in financial and non-financial corporate credit(in China, where everything is government backstopper, there isn't really much of a difference), about 5 times greater than the market cap of Chinese stocks (and orders of magnitude greater than their actual float), and 3 times greater than China's official GDP, which also makes it the biggest bond bubble in the world, even bigger than the US Treasury market.

Here is the full explanation why BofA expects some time around next summer is when the biggest bond bubble in history finally explodes:

The rumble of distant drums

When a developer can issue a 5y bond at 3bp lower than 5y quasi-sovereign CDB bond’s yield, the market appears grossly mispricing risks in our view. Credit spreads of LGFV, corp. and enterprise bonds are all at or close to five-year lows at the moment.

Investors are chasing yield, due to rapid money expansion (M2 at 13.1% in Sept vs. 6.2% nominal GDP growth in 3Q). AUM of bond and money market mutual funds expanded by Rmb1.6tr Jan-Sept and by Rmb1.3tr alone since July after the A-share correction vs. Rmb44.1tr bond outstanding as of Sept.

This is in addition to those inflows from the wealth management products and private funds.

Leverage is also rapidly escalating. Bond repo balance rose by Rmb1.9tr from Aug 12 to Oct 21 (Rmb4.4tr to Rmb6.3tr, Chart below).

Banks use repos to manage short term liquidity; investors, to subscribe to IPOs, and lately, to buy more bonds. We suspect that bond buying has been the primary driver of the growth in repos since July given rising excess reserves at the banks and the weak stock market. Structured bond funds, often providing 4-10x leverage to lower-tranche investors, is another concern. But its size appears small at this stage.

Moral hazard is playing a key role – there is no official default so far in the bond market other than some small SME bonds. Credit spreads narrowed on most occasions when major bond default threats surfaced, suggesting that most investors probably counted on bail-outs (Chart 5-7). Meanwhile, about 2/3 of repos are on less than 7-day term.

Finally, to answer the question on everyone's mind - here is the full list of most likely upcoming Chinese debt default cases. When the bubble bursts, these names will be the first to blow up.

Copyright ©2009-2015 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies every time you engage ...

more

Comments

No Thumbs up yet!

No Thumbs up yet!

{kind=link}