Michigan Consumer Sentiment: February Final Favorable

The University of Michigan Final Consumer Sentiment for February came in at 99.7, up 4.0 from the January Final reading of 95.7. Investing.com had forecast 99.5.

Surveys of Consumers chief economist, Richard Curtin, makes the following comments:

Consumer sentiment remained quite favorable in February, at its second highest level since 2004. Consumers based their optimism on favorable assessments of jobs, wages, and higher after-tax pay. The highest proportion of households since 1998 reported that their finances had improved compared with a year ago and anticipated continued gains during the year ahead. Economic news heard by consumers continued to be dominated by the tax reform legislation and net job gains, which was untarnished by the consensus view that interest rates would increase and stock prices would remain volatile. Although rising interest rates was seen as a reason to temper their longer term outlook for the overall economy, only a modest moderation in the pace of economic growth was anticipated. Although consumers expected the unemployment rate to dip below 4% in 2018, only modest wage growth was anticipated, and inflation expectations have remained unchanged. Interest rates, even when pushed higher in the weeks and months ahead, will not cause postponement of discretionary purchases as long as income continues to rise near its present pace. Personal tax cuts are crucial to spur additional spending, but unlike prior cuts that had an immediate positive impact, this tax cut has not generated universal support across partisan lines. Overall, the data signal an expected gain of 2.9% in real personal consumption expenditures during 2018. [More...]

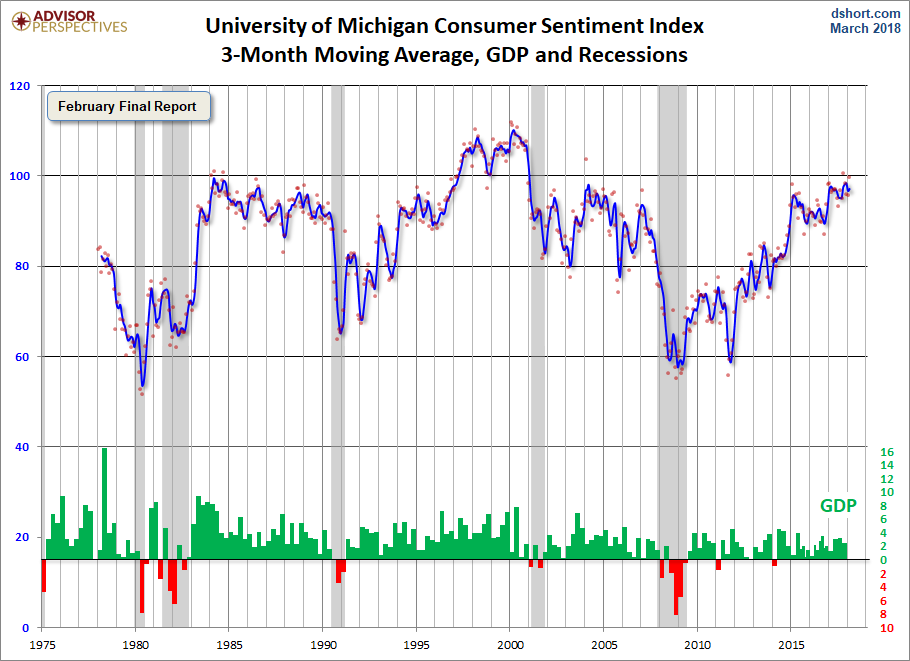

See the chart below for a long-term perspective on this widely watched indicator. Recessions and real GDP are included to help us evaluate the correlation between the Michigan Consumer Sentiment Index and the broader economy.

(Click on image to enlarge)

To put today's report into the larger historical context since its beginning in 1978, consumer sentiment is 16.2 percent above the average reading (arithmetic mean) and 17.5 percent above the geometric mean. The current index level is at the 90th percentile of the 482 monthly data points in this series.

Note that this indicator is somewhat volatile, with a 3.0 point absolute average monthly change. The latest data point saw a 4.2 percent change from the previous month. For a visual sense of the volatility, here is a chart with the monthly data and a three-month moving average.

(Click on image to enlarge)

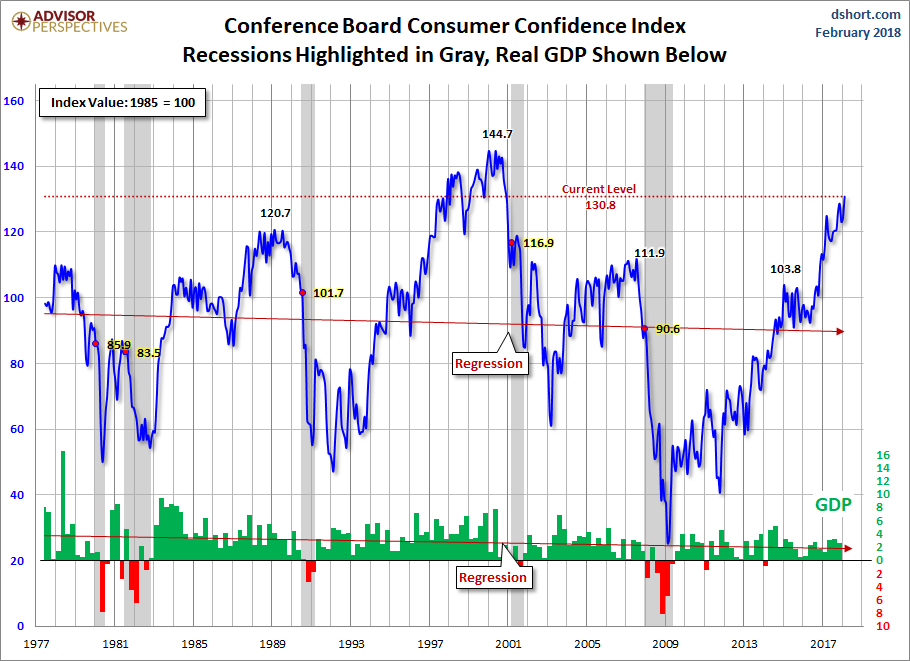

For the sake of comparison, here is a chart of the Conference Board's Consumer Confidence Index (monthly update here). The Conference Board Index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan Index.

(Click on image to enlarge)

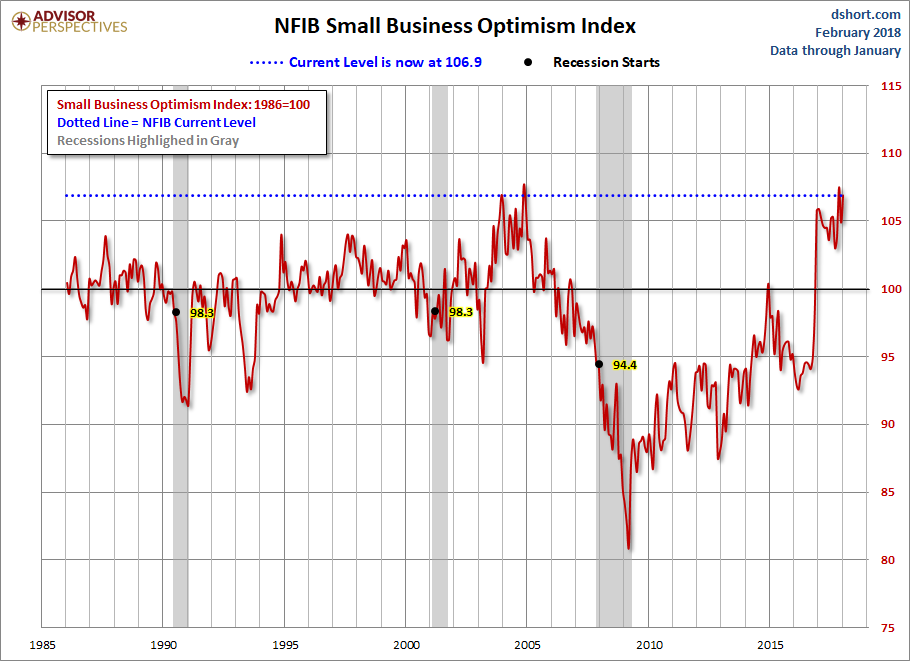

And finally, the prevailing mood of the Michigan survey is also similar to the mood of small business owners, as captured by the NFIB Business Optimism Index (monthly update here).

(Click on image to enlarge)

The general trend in the Michigan Sentiment Index since the Financial Crisis lows was one of slow improvement. The survey findings saw a jump in late 2016 with improvements that have continued through present.

Disclosure: None.