Forget "Free Trade"- It's All About Capital Flows

In a world dominated by mobile capital, mobile capital is the comparative advantage.

Defenders and critics of "free trade" and globalization tend to present the issue as either/or: it's inherently good or bad. In the real world, it's not that simple. The confusion starts with defining free trade (and by extension, globalization).

In the classical definition of free trade espoused by 18th century British economist David Ricardo, trade is generally thought of as goods being shipped from one nation to another to take advantage of what Ricardo termed comparative advantage: nations would benefit by exporting whatever they produced efficiently and importing what they did not produce efficiently. While Ricardo’s concept of free trade is intuitively appealing because it is win-win for importer and exporter, it doesn’t describe the consequences of the mobility of capital. Capital--cash, credit, tools and the intangible capital of expertise--moves freely around the globe seeking the highest possible return, pursuing the prime directive of capital: expand or die.

Capital that fails to expand will stagnate or shrink. If the contraction continues unchecked, the capital eventually vanishes.

The mobility of capital radically alters the simplistic 18th century view of free trade. In today's world, trade can not be coherently measured as goods moving between nations, because capital from the importing nation owns the productive assets in the exporting nation. If Apple owns a factory (or joint venture) in China and collects virtually all the profits from the iGadgets produced there, this reality cannot be captured by the models of simple trade described by Ricardo.

In today's globalized version of "free trade," mobile capital can arbitrage labor, currencies, interest rates, regulatory burdens and political favors by shifting between nations and assets. Trying to account for trade in the 18th century manner of goods shipped between nations is nonsensical when components come from a number of nations and profits flow not to the nation of origin but to the owners of capital.

This was recently described in a Foreign Affairs article, (Mis)leading Indicators:

If trade numbers more accurately accounted for how products are made, it is possible that the United States would not have any trade deficit at all with China.The problem, in short, is that trade figures are currently calculated based on the assumption that each product has a single country of origin and that the declared value of that product goes to that country.Thus, every time an iPhone or an iPad rolls off the factory floors of Foxconn (Apple's main contractor in China) and travels to the port of Long Beach, California, it is counted as an import from China, since that is where it undergoes its final "substantial transformation," which is the criterion the WTO uses to determine which goods to assign to which countries.

Every iPhone that Apple sells in the United States adds roughly $200 to the U.S.-Chinese trade deficit, according to the calculations of three economists who looked at the issue in 2010. That means that by 2013, Apple's U.S. iPhone sales alone were adding $6-$8 billion to the trade deficit with China every year, if not more.

A more reasonable standard, of course, would recognize that iPhones and iPads do not have a single country of origin. More than a dozen companies from at least five countries supply parts for them. Infineon Technologies, in Germany, makes the wireless chip; Toshiba, in Japan, manufactures the touchscreen; and Broadcom, in the United States, makes the Bluetooth chips that let the devices connect to wireless headsets or keyboards.

Analysts differ over how much of the final price of an iPhone or an iPad should be assigned to what country, but no one disputes that the largest slice should go not to China but to the United States. That intellectual property, along with the marketing, is the largest source of the iPhone's value.

Taking these facts into account would leave China, the supposed country of origin, with a paltry piece of the pie. Analysts estimate that as little as $10 of the value of every iPhone or iPad actually ends up in the Chinese economy, in the form of income paid directly to Foxconn or other contractors.

In a world dominated by mobile capital, mobile capital is the comparative advantage. Mobile capital can borrow billions of dollars (or equivalent) in one nation at low rates of interest and then use that money to outbid domestic capital for assets in another nation with few sources of credit.

Mobile capital can overwhelm the local political system, buying favors and cutting deals, all with cash borrowed at near-zero interest rates. Mobile capital can buy up and exploit resources and cheap labor until the resource is depleted or competition cuts profit margins. At that point, mobile capital closes the factories, fires the employees and moves on.

Where is the "free trade" in a world in which the comparative advantage is held by mobile capital? And what gives mobile capital its essentially unlimited leverage? Central banks issuing trillions of dollars in nearly-free money to banks and other financial institutions that funnel the free cash to corporations and financiers, who can then roam the world snapping up assets and arbitraging global imbalances with nearly-free money.

There's nothing remotely "free" about trade based not on Ricardo's simple concept of comparative advantage but on capital flows unleashed by central bank liquidity.

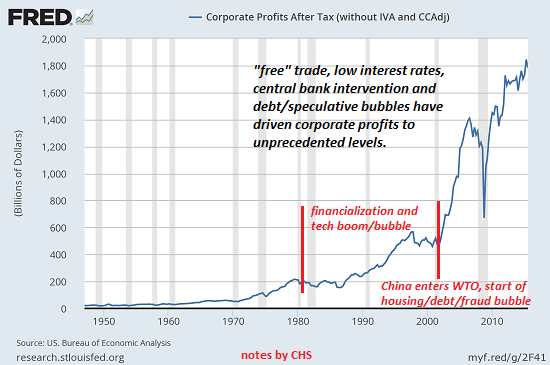

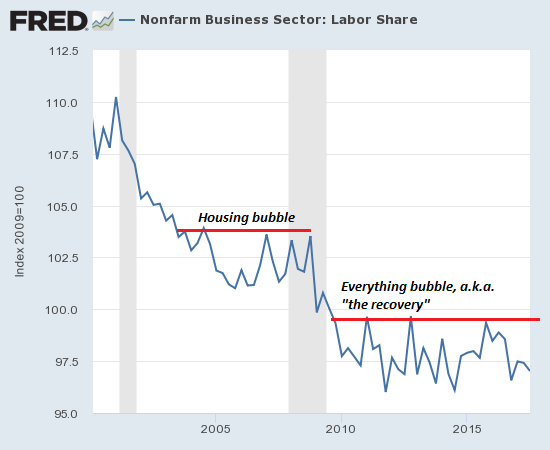

The gains reaped by mobile capital flow to those who control mobile capital: global corporations, financiers and banks. No wonder labor's share of the economy is stagnating across the globe while corporate profits reach unprecedented heights.

Disclosures: None.