Great Recession Causes And Case-Shiller As Explained By Marcus Nunes

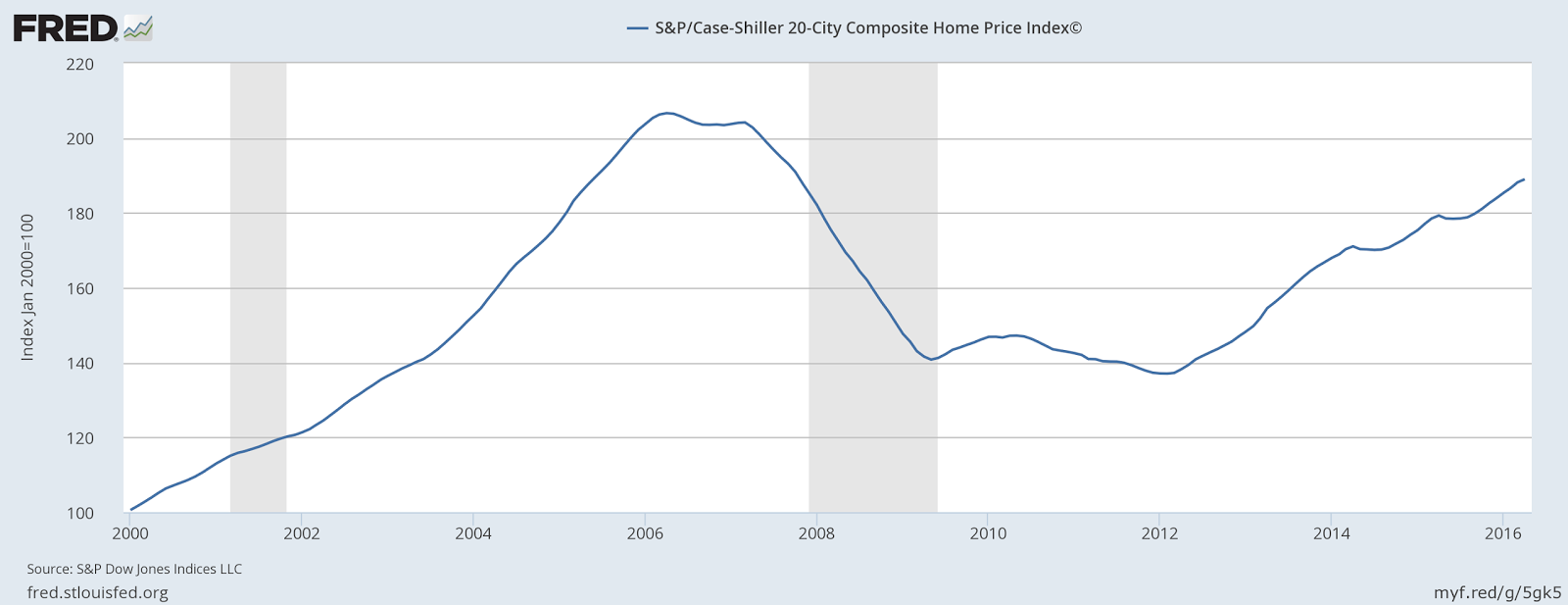

Before ending with ideas offered by market monetarist Marcus Nunes, it is helpful to explain Case-Shiller. The leading indicator of the housing crash was the Case-Shiller Home Price Index, abbreviated C-S HPI. It is a 20-city measurement of house prices. The leading indicator of the housing crash was in serious decline prior to the subprime housing crisis of August 2007. The subprime crash of August was brought into being when the commercial paper market was destroyed, commercial banks were forced to take back loans hidden in SIVs, and subprime loans went away completely.

The banks could have solved at least part of this problem prior to the August crisis, with starter loans for first time buyers, who were either priced out of the market or forced to take subprime mortgages. Starter loans for first time buyers would have been new lifeblood interjected into a housing market where subprime was dying!

If the central bank had 1. encouraged this starter loan program, and 2. had not permitted mark to market, 3. banks would have honored promises to refi toxic loans, and 4. had embarked upon an effort to buy commercial paper in early 2007, the banks would not have stopped lending in the real estate market in general (though the bubble states may have suffered), and the following chart would not have looked the way it now looks.

There may have been a decline in prices, but surely not the decline that took place. After all, the real subprime (including Alt A) debacle came from four states: California, Florida, Nevada and Arizona.

We can see that the crash started before the subprime financial crisis took place. The question is why? The C-S HPI clearly was the leading indicator of crash. The chart is shown below:

The decline in prices began in April, 2007. Again, this was way before the subprime crisis of August, 2007. But the decline was as intense in April as it was after August. The question remains, why?

Clearly, the bankruptcy of New Century Finance must have had a major effect on kick-starting the real estate decline. The trouble started in January of 2007, increased in March, 2007, and culminated in the April 2, 2007 bankruptcy of the firm.

This should not have affected the entire housing market. However, the MBSs that were pledged as collateral were undermined by the bankruptcy. The mortgages were simply not worth what people thought they were worth. The collateral derived from the MBSs was not worth what was claimed.

The derivatives catastrophe that resulted from the mispricing of MBSs by the Fed made the New Century Finance demise that much more significant than it ever should have been. Banks had bet on the stability of these MBSs, making things even worse, undermining the these bonds.

This derivatives catastrophe was all made possible by the creation of securitization of mortgages. Getting rid of the paper brought profits based on the volume, not the soundness, of the loans. The bonds, mispriced by the Fed itself, were then used as collateral in other deals until shown to be faulty.

New Century was ruined when it was forced to repurchase failed mortgages which were no longer being securitized, and it ran out of money. According to Investopedia New Century was over-leveraged, controlling $25 billion of assets with $2 billion of equity. Leverage played a key role in the destruction of subprime lending. Yet it was all sanctioned by commercial banks until the CP market went under. Once New Century and more subprime lenders went under, the commercial banks had to bring the bad loans back onto their balance sheets. Lending to the subprime market effectively ended.

I take issue with the conclusion of the Investopedia article. The article author blames New Century, but really the fault was with those responsible for allowing deregulated entities like New Century to exist in the first place. That would seem to fall at the feet of Congress and central banks.

As Marcus Nunes has pointed out, once the subprime crisis had stalled, the next shoe to drop was the ability to borrow on your own wealth. That HELOC source of credit was destroyed in mid 2008, and with the demise of HELOCs, housing wealth as shown by the CS20 chart above was cratering too. That probably was the back-breaking development. Once nominal income and spending declined, and people had no access to credit from their own vanishing equity wealth, the economy collapsed.

Nominal spending is still below trend, as Nunes goes on to say. Therefore, recovery just isn't progressing as it should. Of course, that article was written in 2013, and it appears that the economy is a little stronger now, but not strong like past recoveries.

But, as Prof. Nunes points out, forcefully, the destruction of housing wealth, and the ability to borrow on that wealth, was a key driver of financial decay in the entire system, leading to the Great Recession. Not only did the banks experience a financial crisis, but so did many homeowners, the backbone of the middle class. Banks would not lend, and borrowers could not borrow.

If you want to keep an economy going, you have to give the people access to credit. Cut off credit in a widespread manner and you risk upending the financial system's solvency. Heloc destruction and the inability to refinance easy loans caused a mark decline of wealth, and were key to the takedown of the real estate market.

Yet the wealthy were able to blow the bubble back up in the last few years without the help of the middle class. Therefore, keeping credit going for the middle class during the financial crisis would not necessarily have been an exercise doomed to failure in most states. I just think it was failure that was wanted by those who would profit.

Disclosure: I am not an investment counselor nor am I an attorney so my views are not to be considered investment advice.