Signet: (SIG)

- Investor fear has been overdone and left the shares incredibly undervalued.

- Initiatives to enhance shareholder value: large stock buyback, debt repayment, and a dividend raise.

- Overview of the current situation and the best way for investors to participate.

“I wait until there is money lying in the corner and all I have to do is go pick it up. I do nothing in the meantime.”

-Jim Rodgers - MarketWizards

My recent investment articles:

Subscribe to my free Investing Newsletter

Summary:

Shares in Signet have fallen by nearly 50% this year. The company is in the process of selling its financing portfolio and will have tremendous flexibility to retire debt and pursue significant buybacks. Strong cash flows and significant liquidity has been ignored and left the shares incredibly undervalued. Management is taking numerous moves to enhance shareholder value including debt repayment, raising the dividend, and a large stock buyback.

As such, the risk/ reward is very attractive at current levels. The best way for investors to participate in the stock and take advantage of elevated implied volatility.

About Signet: (SIG)

Signet is the largest specialty retail jeweler by sales in the US, Canada, and the U.K.

On May 29, 2014, the company acquired Zale Corporation for $1.458 billion. The company issued $1.4 billion of long-term debt to fund the purchase.

The Sterling Jewelers division: formerly the US division, operates 1,588 stores in all 50 states. Its stores operate nationally in malls and off-mall locations as Kay Jewelers, and regionally under a number of well-established mall-based brands.

- Destination superstores operate nationwide as Jared The Galleria Of Jewelry.

- The Zale division consists of two reportable segments: Zale Jewelry, which operated 970 jewelry stores at January 28, 2017, is located primarily in shopping malls throughout the U.S., Canada. and Puerto Rico.

- Zale Jewelry includes national brands Zales Jewelers, Zales Outlet and Peoples Jewellers, along with regional brands Gordon's Jewelers and Mappins Jewellers. Piercing Pagoda, which operated 616 mall-based kiosks at January 28, 2017, is located primarily in shopping malls throughout the U.S. and Puerto Rico.

- The U.K. Jewelry division, operated 508 stores at January 28, 2017. Its stores operate in major regional shopping malls and prime locations.

Relevant Articles:

45 Ways to Increase your Income

9 Best Ways to Save $7K This Year

11 Legitimate Survey Sites for 2018

Overview:

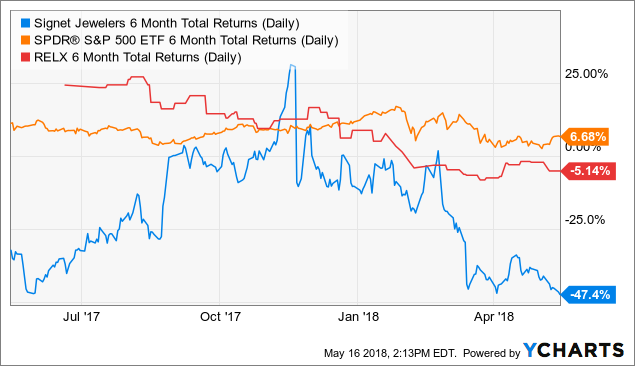

Shares of Signet have had a sizeable decline relative to the overall market and the retail index (RLX). This was due to weaker earnings, poor visibility, and a real fear among investors of mall based retailers. However, based on the cash flow and valuation of the underlying business, the fears seem overdone.

Investors have placed too much focus on the negatives and ignored excellent cash flow as well as the announcement of a plan to reduce debt and buyback around 25% of the shares outstanding.

SIG 6 Month Total Returns (Daily) data by YCharts

Companies don't become incredibly undervalued unless there is some risk involved with the business.

Risks to shareholders in Signet include a continuation of negative same store sales trends and a lack of earnings visibility. In my opinion, the shares have priced in much of the negative trend scenario.

Company initiatives include: Cost reductions, a transition to digital, and reducing underperforming stores.

Weak Earnings and visibility:

Current Fiscal 2019 guidance:

- Same store sales down low-to-mid single digits,

- Total sales of $5.9 billion -$6.1 billion,

- non-GAAP diluted EPS of $3.75 - $4.25

Earnings Estimates:

- For fiscal year 2019, analysts estimate that SIG will earn USD $3.97.

- For fiscal year 2020, analysts estimate that SIG's earnings per share will decline by 5% to USD $3.77.

Negative analyst sentiment:

9 out of 10 Wall street firms have a "HOLD" rating on the stock. (vis S&P).

Analysts don't have earnings visibility due to recent disappointing comps and sales as well as concerns regarding mall based retailers in general.

Mall traffic continues to be a concern but the question for investors is, has the worst of these trends already been priced into the shares?

Positive Catalysts:

Selling credit portfolio: Sold in October for $950M. The company has stated on their earnings conference call, they plan to repurchase nearly one quarter of all shares outstanding.

At the completion of Signet’s transition to a fully outsourced credit model, we expect that the credit transactions will have generated more than $1.3 billion in proceeds, which are being used for debt repayment and significant share repurchases. - Gina Drosos, CEO

Growing E-Commerce business:

Ecommerce sales at banner websites and R2Net rose 52.8% to $253.8M in the latest quarter.

Signet aims to grow its digital sales as a percentage of total revenues to at least 15% in Fiscal Year 2021, compared to 8% in Fiscal Year 2018.

Closing underperforming stores; Signet expects to close 200 stores by the end of 2019.

Use Cost Reductions to transition to higher online sales. The Company estimates online savings will total $85M in 2019. (CC)

Financial Strength:

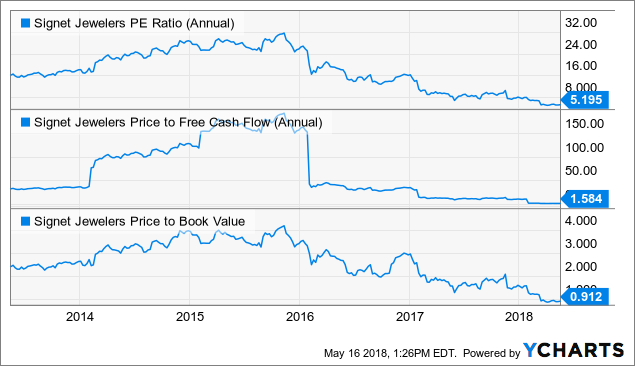

With Signet, we see all the classic signs of a value stock that is significantly undervalued:

P/E: 5 (well below historical average of ~ 15)

Price to Cash Flow: 1.56 - Incredibly attractive

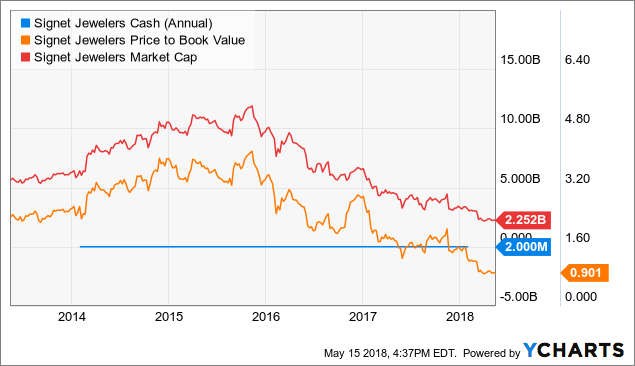

Price to Book Value: .912 -

Based simply on the valuation, Signet is clearly one of the most undervalued companies in the stock market. Since management is being pro-active, so I would not expect the shares to stay at this level.

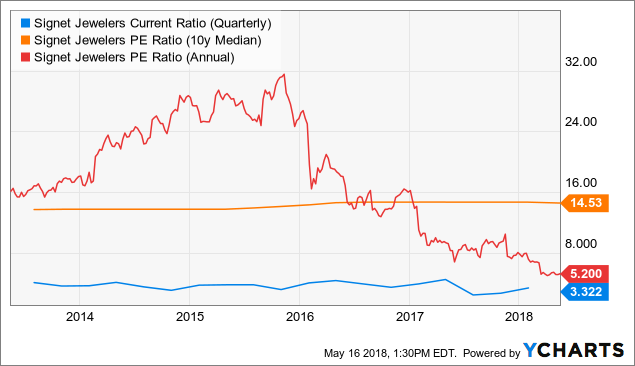

SIG PE Ratio (Annual) data by YCharts

P/E Ratio:

Price to earnings is not the most sophisticated metric to evaluate a company. However, in this instance, it provides a good representation of how undervalued the shares of signet have become. A pretty consistent 14.5 x earnings has deteriorated to a p/e of five. The shares are incredibly undervalued relative to the stock market as well as to its' historical value.

One would expect a return to a double digit p/e once earnings normalize. In addition, the announced buyback will shrink the shares outstanding by up to 25% resulting in improved earnings as well.

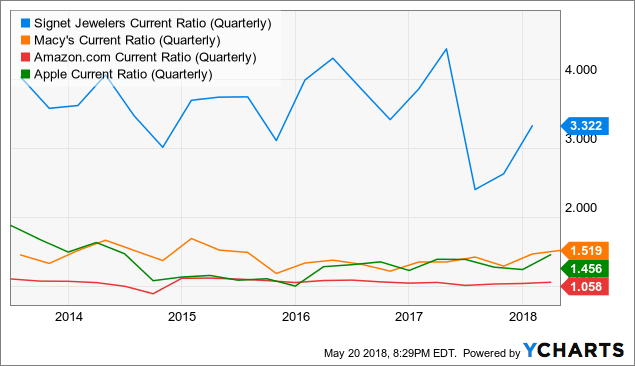

SIG Current Ratio (Quarterly) data by YCharts

Liquidity:

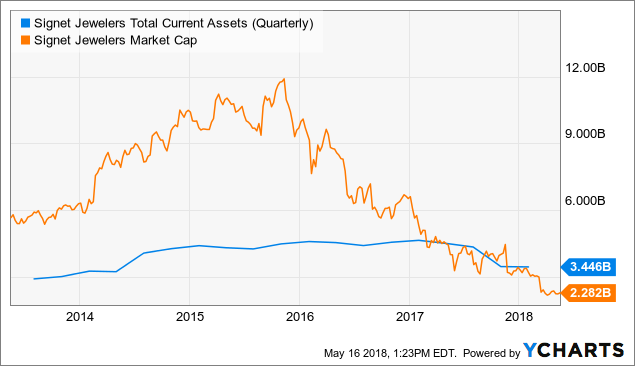

SIG Total Current Assets (Quarterly) data by YCharts

The current ratio (liquidity) above 2 demonstrates a company that has tremendous financial strength.

Deep value investors (like Ben Graham), typically look for a current ratio of 2 or higher. As we see, Signet has consistently had a current ratio over 3. This is due to the tremendous cash flow that their business generates.

The company is forecasting free cash flow of $781M for this year. (CC)

As we can see, even compared with some of the best performing companies in this market, like Apple (AAPL) and Amazon (AMZN), Signet has tremendous liquidity.

SIG Current Ratio (Quarterly) data by YCharts

Again, it's hard to find any valuation metric where Signet isn't incredibly attractive to a value investor.

SIG Cash (Annual) data by YCharts

Dividend: The company raised the dividend 19% to .37 creating a yield of ~3%. Another move to enhance shareholder value.

Technical Overview & Earnings:

Signet has a relative strength of (4), which means that 96% of the stocks in the market have outperformed it in the past year. The shares seem to have support at the $40 level and with a large buyback, would expect the shares to hold this level unless the upcoming earnings (6/6), disappoint analysts’ very low expectations.

How to participate:

The uncertainty surrounding the company has resulted in high implied volatility for the upcoming earnings (June 6th). Investors who are comfortable with options should consider using this situation to their advantage.

Regular:

For regular investors, I would advise a buy/ write strategy: buying the stock ~ $39.49 and selling a call to take in premium and take advantage of the high volatility.

Buy/ Write: Buy the stock and sell the $50 calls for $1.45 at the October 19th Expiration. If the shares are called away, the position gains ~$11.45 or ~28% for the position and ~58% annually.

Conservative:

For more conservative investors, I would advise selling a put.

Sell: The $37.50 Signet puts for 1.33 expiring on June 8th.

If the stock trades below $37.50, the cost basis would ~$36. If the stock continues to trade at or above $37.50, the investor makes about 3.5% on the position or ~42% annually.

Conclusion:

Investors have driven Signet shares down nearly 50% on fears of short-term earnings and sales trends. When we step back and look at the overall picture, Signet is incredibly undervalued based on liquidity, cash flow, p/e, and price to book. Positive catalysts for Signet include: debt repayment, a 25% stock buyback, and a dividend raise For Signet, the shares are too attractive to stay at this level too long.

For more info: The Frugal Prof