It can sometimes be a little confusing to the average investor when the media and financial market communities throw around the phrase “the VIX is dead”. But when we review the chart of the VIX itself, we come to acknowledge how docile the market and the VIX really are over time.

As depicted in the VIX chart, it becomes quite clear that volatility, measured by the VIX/fear index, can remain quite complacent for extended periods. In fact, volatilities very nature is to remain complacent far longer than expressing outsized volatility. Regardless of the factual representations offered in the VIX chart, which goes all the way back to 1991 and encompasses major market events, for some reason many traders and investors look to go long volatility in any of its form factors. The VIX or volatility doesn’t die nor does it have the ability to die, but rather it expresses an ability for a market or markets to mature past the point of greatest fears and from the events that cause fear to have taken place. In other words, the fearfulness surrounding the “what’s the worst case scenario” curtails as the perceived worst-case scenario actually occurs. The Savings & Loan crisis, Dot Com bubble bursting, 9-11 and the Financial Crisis have all given birth to a more resilient market and more fearless traders/investors.

It has come to be that even with markets around the globe expressing all-time highs, record sovereign debt levels, political uncertainty and currency “manipulation”, fear or volatility is near record low levels in the United States equity markets. Really short and really sweet; the VIX is not for those betting against the market, is not a viable hedge against a potential market pullback and is not an instrument for those with long, long-term intentions. Moreover, to succeed with profits by going long volatility with the VIX or any direct VIX-leveraged instrument, the timing must be impeccable and cheaply acquired, which is a rarity in and of itself. Nonetheless, even with the apparent pitfalls and a seemingly narrow path to profits from positioning long the VIX, many people do so…even those supposed professional traders and media participants on CNBC’s Fast Money.

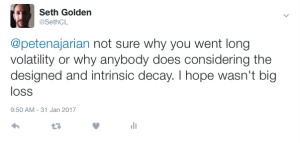

It was a little over a month ago that the markets were going up against several political and global events. These votes included an Italian Referendum vote, the eventual Inauguration of Donald Trump, U.S. equity indices hitting all-time highs and much more. It was around this time that Fast Money’s Pete Nejarian expressed on air that he had hedged against a market pullback by going long the VIX against his long positions. This wasn’t the first time Mr. Nejarian outlined the strategy and it wasn’t the first time I had followed (not positionally but in event chronology) his thought to see how the strategy would pan out. Of the many times the Fast Money contributor outlined this strategy to viewers, Mr. Nejarian lost money on this “hedge”.

The definition of a hedge is to find the hedge profitable with respect to a possible event that goes against the underlying asset being hedged, like a market pullback. So by Pete using an instrument, like volatility to theoretically move higher in case of a market pullback of sorts doesn’t make a lot of sense. Again, I refer to the VIX chart above for a brief point of evidence. If one is fortunate, going long the VIX may work out profitably, as a hedge, 10% of the time utilized as a hedge. THAT’S NOT A HEDGE! In a sense that is an expression of ignorance and willing negation of what the VIX is, does and likely will do over time. And it is for this reason of possible confusion as to why Mr. Nejarian uses the VIX as a hedge that I personally reached out to the Fast Money contributor via Twitter (TWTR ).

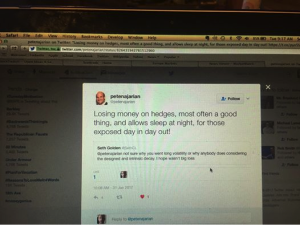

Knowing that this trade implemented by Mr. Nejarian had run its course with a loss to capital invested I offered the following to him on Twitter.

I took a screen shot of Mr. Nejarian’s reply to my direct Tweet because I often find myself in a position where others fail to legitimize an argument contrary to my position, for whatever the subject matter might be.

“Losing money on hedges, most often a good thing, and allows sleep at night, for those exposed day in day out”. That was Mr. Nejarian’s response to my tweet displayed, but again, negates that volatility is almost always a losing hedge from the long side. Having witnessed Mr. Nejarian failing to achieve his objective with such a hedge in the past I was hoping for a better response or at least the recognition, through further dialogue, of why going long volatility is not a hedge at all. What I found though after the short response and my followed retort was that Mr. Nejarian couldn’t retort with logic as to why anybody would hedge underlying positions with the VIX/volatility. Knowing the Fast Money contributor was found wanting for logic and as he is such a public figure and proposed market trading expert I believed his tweet would be erased. As such, I took the screen shot as not just proof of the engagement, but also to show that even experts have trading and understanding errors regarding the VIX. Unfortunately, I was accurate in my assessment of the forecasted actions by Mr. Nejarian who has blocked me from viewing his Twitter feed. In no way was I attempting to pull a “ha ha ha” on Mr. Nejarian, but more so to seek out where my misunderstanding may be with regards to his VIX participation and mine to boot. Sometimes, one can validate their market participation through the participation of others.

For those readers/investors whom have read my publications over the last few years, you know by now that I don’t pull any punches and I outline things that are the way they are. It’s also no secret that I’ve been short VIX-leveraged instruments since I happened upon them in 2012. My favorite VIX-leveraged instrument is also not a well-kept secret as I maintain a core short position in ProShares Ultra VIX Short-Term Futures ETF (UVXY). I generally maintain 20% of the Golden Capital Portfolio with UVXY short shares. Only a couple of weeks ago I reduced that exposure, as I have typically done at the onset of a reverse split. The last reverse split for shares of UVXY found the share price reversing in value from $6 range to $30.60 a share. As the VIX remained complacent through and post the reverse split, shares trended lower whereby I covered a block of shares just below $27 a share. Since that time I’ve made several trades that have still allowed me to profit from shorting UVXY as the share price moved even lower. At the end of the most recent trading week, UVXY shares closed at roughly $23.50 a share, emphasizing or echoing my warnings to those holding UVXY long through a reverse split. In the article titled UVXY: Pre-Split Caution Being Raised, I expressed the greatest of warnings regarding how a long shareholder would be further impacted by a reverse split. Unfortunately, that warning or prescient analysis has come to fruition and would essentially find long UVXY participants with even greater losses since the reverse split.

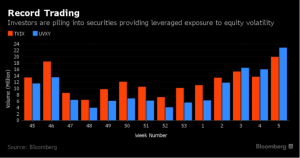

I’ve been asked, over the last two years, about my UVXY participation being as public as it has found itself to be; “Do you worry about more people using it and not being to benefit to the degree you had in the past”. It’s a great question and something I have greatly considered. Utilizing UVXY profitably and in the manner, which I do, takes a dedication to core best practices and an even greater ability to withstand the feared backwardation. Not many can withstand backwardation to the degree of 100% or greater. So even as I ascertain UVXY and like products have a degree of certain profitability from the short side and long-term, many will not participate with these instruments for fear of backwardation of 100% or greater. And I get that! But having said that, more and more people are trading these instruments day in and day out. Bloomberg recently offered a brief titled Trump Leads to Record Trading of Leveraged VIX Securities: Chart

It’s obvious that more and more people are trading these VIX-leveraged products. Hopefully, they are trading them according to their construct as opposed to how Mr. Nejarian has used them in the past. Unfortunately, publications found on Seeking Alpha show that many still don’t understand these products or use them according to their construct.

As a Seeking Alpha contributing author I’ve written around a dozen VIX-leveraged ETF articles since 2015. Additionally, I’m widely considered to be an expert of VIX-leveraged ETF “Do’s and Don’ts”. Having said that, it’s concerning when I witness other Seeking Alpha authors going long the VIX and VIX-leveraged products like VXX, UVXY and TVIX. Where other financial publishing sites will not publish such articles, for some reason Seeking Alpha has chosen to do so. Articles outlining and promoting long volatility strategies without the forbearance of risk assessment come with elevated risk, even to the degree they introduce a moral hazard for Seeking Alpha. As the publishing party, Seeking Alpha may be creating a moral hazard with these publications. To reiterate, most financial sites won’t publish long VIX-leveraged ETF articles due to the intrinsic risk for these instruments to produce outsized losses from the long side as they are constructed to decay in value over time.

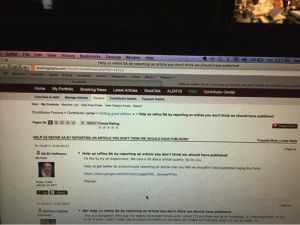

So when the CEO of Seeking Alpha (Eli Hoffman) posted a forum topic (only open to Seeking Alpha contributing authors) titled Help US Refine SA By Reporting Articles You Don’t Think We Should Have Published, I took the opportunity to comment on the thread. I believe Seeking Alpha publishing long thesis on VIX-leveraged instruments creates a moral hazard in the Seeking Alpha community as well as outsized losses for the readers and investors who otherwise are not well informed regarding the constructed decay that resides within these instruments. I commented within the forum along these lines, evidencing the constructed decay for these ETFs and why using them from the long side is with great error. Unfortunately, as is the case many a time and exampled in many Seeking Alpha volatility publications, even those contributing authors in the forum didn’t understand the inherent risk of these articles and the thesis put forth. Now, because there could not be any logical argument to the contrary of what I offered as an opinion, but supported with great factual representations and logic, the CEO of Seeking Alpha locked the forum and would not comment on my offering directly. I don’t believe Eli Hoffman realized that someone would question the moral standing of Seeking Alpha through these publications that go back several years.

Even more relevant, I don’t believe Mr. Hoffman understands the concern raised or expected it to be inflamatory. At best I would suppose or hope that the Seeking Alpha team has researched my comments and course corrected for the future publications of long VIX-leveraged ETF thesis article submissions. Seeking Alpha is one of the most widely visited, free financial blog sites on the Internet and comes with a great, longstanding reputation for op-ed and investment thesis articles. But I have had my “run ins” with the editorial staff in the past for failure to conceptually understand my article submissions and to the point where e-mails had gone back and forth with me having to educate the staff as to the facts of the subject matter. To that point, I’ve even facilitated appropriate content on Seeking Alpha by reporting grossly false positioned information within many articles. Those articles had been removed or the author of the article was forced to revise for “reason of content fact”. So it was quite disappointing that for a forum topic dedicated to the betterment of publications that Mr. Hoffman fell short of not only logically refuting my assertions regarding VIX-leveraged ETF long thesis articles, but he locked the topic thread from further commentary by stating the following:

“RE: Help us refine SA by reporting an article you don't think we should have published

I'm going to close this thread so it doesn't inadvertently become a place to report articles we shouldn't have published (IYHO).

Not going to respond to any specifics discussed here.

Here's the thing: SA is not about editorial expertise. As this thread demonstrates, experienced investors can disagree about some fairly fundamental issues - which is why I believe the optimal path to (relative) truth is to discuss things in the open. Point counterpoint. That is one of the raisons-d'etre of SA. And why burying these kinds of disagreements - polite but vigorously argued - on a contributor forum deprives SA readers of the discussion.”

Maybe it was my fault for introducing my comments and aligning them in the interest of recognizing the moral hazard created. Nonetheless, Mr. Hoffman contradicts the purpose of the topic thread that he created in the opening response to my well-intended comments aimed at offering what should not have been published by Seeking Alpha. Secondly, as Mr. Hoffman further offers, I’m well aware of the editorial lack of expertise and the overall shortcomings of the platform. Thirdly, I guess the optimal path to truth can be discussed in the open, unless there is no way to argue against the apparent moral hazard introduced by the Seeking Alpha platform through certain publications. In offering that disagreements are being buried away from the readers’ ability to review them openly, it also seems contradictory that Mr. Hoffman locked the thread from even his contributing authors to discuss, openly. As is often the case regarding VIX-leveraged instruments, there is a great deal of misinformation and erroneous thesis published, but “what are ya gonna do”. Let’s move on!

The increasingly, present consideration as it pertains to the media and financial market pundits is whether or not the VIX will trade into the single-digits level. This would express an amazing feat of strength for the fear index and befitting the overall market that has expressed record levels for many market metrics. Having said that, with the Golden Capital Portfolio holding only 17.2% of its assets in UVXY now, I’d also equally welcome a return of volatility for which to recapture short shares of UVXY from higher prices. So bring on the fear and higher levels of volatility oh mighty markets, I’ll be awaiting it with a cash-heavy portfolio! And for the increasing number of volatility traders and investors out there, be sure to surround yourself with good resources and sound information on the subject matter.