Once upon a time, central banks’ purchases of common stocks were non-existent. In recent times, however, a 2018 Reuters article observes that once stodgy central banks have moved into the fast lane of the investment world: “Lately, central banks have been doing the market equivalent of zipping around in a sporty convertible. In recent years, at least two large central banks have been snapping up large quantities of equities, typically considered a risky investment."

The two most prominent "convertibles" are the Bank of Japan and the Bank of Switzerland. The Bank of Switzerland now owns $8.8 billion in U.S. technology stocks. The Bank of Japan’s voracious appetite for Japanese exchange-traded funds also did not abate with the Dow and the Nikkei’s October highs. In fact, the bank bought a record $7.68 billion in October, “apparently aiming to support equities.” Central banks obviously feel safe employing this policy, and the public finds a reason to feel safe because of it.

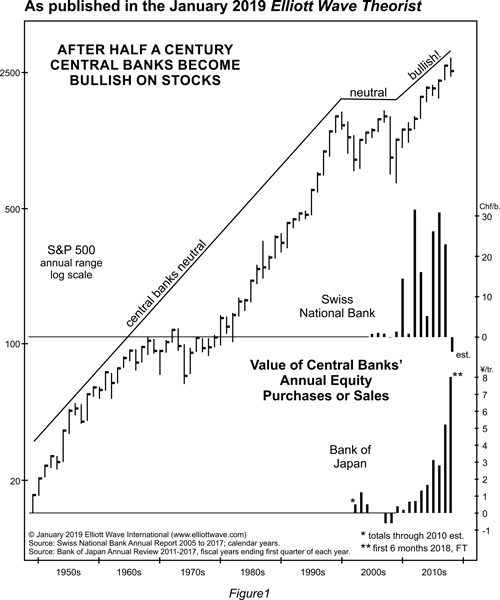

The Elliott Wave Theorist [EWT] puts the central bank equity plunge into historical perspective. Figure 1 shows stock purchases by the Bank of Japan and the Swiss National Bank back to 1949, when the Bank of Japan was restructured along current lines. Note that for half a century, central banks did not buy any stocks. Then, shortly after the peak in the S&P 500 in 2000, they revved their engines.

(Click on image to enlarge)

Wall Street on Parade estimates that more than a dozen central banks have begun buying publicly traded stocks in the last decade.

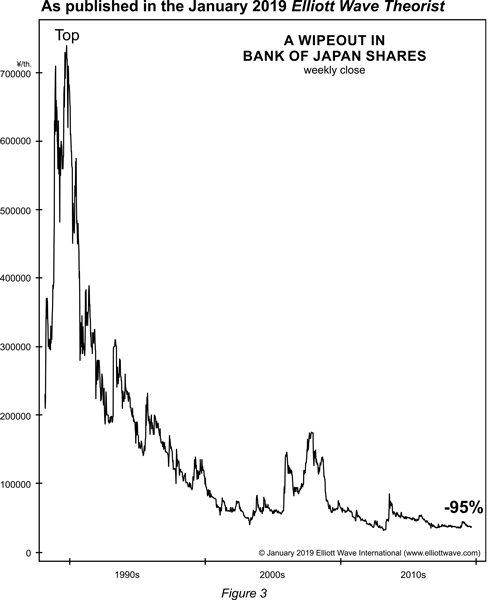

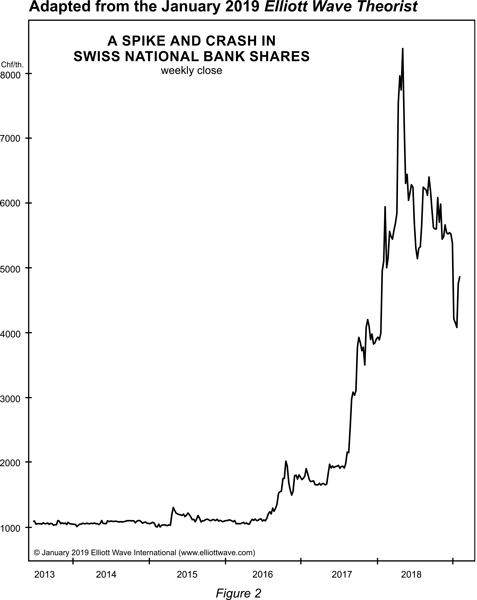

How have the banks fared so far? Not well, based on this Wall Street Journal headline from last month: "Riches to Rags: Swiss Central Bank Swings from Record Profit to Large Loss.” The Swiss National Bank itself is a publicly traded company, and the price of its stock (see Figure 2) has plummeted from just under 10,000 Swiss francs to 4000, a decline of nearly 60%. The stock of the Bank of Japan (see Figure 3) has done even worse. After peaking at ¥740,000 at the top of the Japanese bull market in late 1989, it has slumped to ¥37,000.

(Click on image to enlarge)

(Click on image to enlarge)

What happened to make these two banks take the plunge into equities? We believe the cause was the psychology driving a multi-decade bull market. EWT editor, Robert Prechter explains, “Acting just as the odd-lotters of olden days, central bankers became confident near the end of the run that owning stocks was a safe bet and a good idea.” (Note: Another group with a well-documented history of buying high and selling low is foreign purchasers of U.S. shares. See the history of foreign buying here).

Such histories have not deterred central bankers. A Forbes article on January 16 reported: "China's Central Bank Will Prop Up Country's Stock Market... China's PBoC will buy locally listed shares to prop up a stock market that's down over 25% in the last 12 months. If things get better, China can outperform with the central bank's support." As Prechter noted, “the idea that central-bank buying can force a bull market is so entrenched it’s taken for granted.” We believe that the ramped-up commitment of foreign and domestic stock purchases by central banks is not the ultimate bullish sign that investors believe, but rather one of great bearishness.

About Peter Kendall

Peter Kendall co-edits Elliott Wave International’s Elliott Wave Financial Forecast with Steven Hochberg. He also provides commentary on cultural trends, the economy and the U.S. stock market for the firm’s Global Market Perspective. Kendall began his career as a financial reporter and columnist in 1983. He wrote “On the Money,” a column for The Business Journal, from 1991 to 1997. Kendall joined Elliott Wave International as a researcher in 1992 and served as the director of EWI’s Center for Cultural Studies, where he focused on popular culture and the new science of socionomics. He has been contributing to Global Market Perspective since 1995, and he also contributes to EWI’s Short Term Update. He graduated from Miami University in Oxford, Ohio, with a degree in Business Administration.

About Steven Hochberg

Steven Hochberg co-edits Elliott Wave International's Elliott Wave Financial Forecast with Peter Kendall, writes the Short Term Update thrice weekly, and provides commentary on the U.S. stock market, interest rates and precious metals for Global Market Perspective. Over the years, Hochberg has become a sought-after lecturer and has been quoted in various media outlets, such as USA Today, The Los Angeles Times, The Washington Post, Barron’s, Reuters and Bloomberg. He has also discussed financial markets on CNBC, MSNBC and Bloomberg Television. Hochberg began his professional career with Merrill Lynch and joined Elliott Wave International in 1994.