Weighing The Week Ahead: Will Middle East Conflict Bring An End To The Bull Market?

The economic calendar features the employment situation report at week’s end with a preview from the ADP on Wednesday. In my early WTWA preparation I expected some reallocation action by those returning from vacation, and a focus on employment as a key economic read. I still believe that both will happen, but the U.S./Iran confrontation has taken center stage. There are so many dimensions and so much uncertainty. Financial media will pursue each of the many threads, not always sticking to market implications. The key question will be: Will Middle East conflict bring an end to the bull market?

Last Week Recap

In my last installment of WTWA, I ventured that the discussion of data would take a back seat to market forecasting. I raised the question of how best to use history in making a forecast. I was accurate in my guess about data discussion, but wrong in thinking volatility would remain low. The absence of the A-team did not seem to slow down the Thursday and Friday trading.

Eddy Elfenbein’s research on history and forecasting by Wall Street shows some interesting results. He joins the rest of us in observing that the Wall Street forecasts have little predictive value. But how are these feeble forecasts reached? He finds the following:

I dug into the numbers and found that there’s a decent correlation—a negative one—between their predictions and the year that just ended.

This means that forecasters simply take what just happened and assume the opposite will happen but to a much lesser degree. Forecasters also assume a very narrow band for the market’s performance, generally about 5% to 12% (though not always). In reality, the market is far more volatile.

If you are still interested in forecasts, the Visual Capitalist has a wider range of topics from 100 sources, presented in bingo card style.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring the futures version from Investing.com. If you check out the interactive chart, you can see the related news sources and add your own indicators.

The market lost 0.2% for the week. The trading range was 1.4%, not including the pre-opening drop in futures before the Friday opening. Much of the punditry expressed surprise that the market was so “resilient” on Friday. The overall trading range is similar to the experience before the holiday period. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

Noteworthy

The size of the Australian wildfires is difficult to grasp. Statista helps with this chart comparing noted past fires.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too.

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results remain positive in both the long- and concurrent-time frames, and the short-term forecast remains neutral. NDD continues to emphasize the split in producer and consumer indicators, something he is watching closely.

The Good

- Pending home sales for November were up 1.2%, better than expectations of 1.0% and much better than October’s (upwardly revised) decline of 1.3%.

- Construction spending for November increased 0.6% versus expectations of 0.3%. October’s decline of 0.8% was revised to a 0.1% gain. Steven Hansen (GEI) analyzes both rolling averages and inflation-adjusted data, going beyond the typical headlines.

- Serious delinquencies in mortgages declined in November. (Calculated Risk).

- Corporate sentiment is improving (Duke CFO optimism). Please note that respondents think their own company is doing fine but are less confident of others. CFO’s probably listen to and read financial media!

- Mortgage originations remain significantly ahead of each year in the last decade.

The Bad

- Consumer confidence for December registered 126.5, missing expectations of 128.0. November was revised higher, from 125.5 to 126.8. Jill Mislinski has the story – future expectations also lower—and the expected great chart.

-

ISM manufacturing for December declined to 47.2 versus expectations of 49.0 and November’s 48.1. Bespoke analyzes the various subcategories as well as comments from respondents. The thread of weaker exports is a common one, although Bespoke does not draw that conclusion. The ISM’s own release includes the following statement:

Global trade remains the most significant cross-industry issue, but there are signs that several industry sectors will improve as a result of the phase-one trade agreement between the U.S. and China. Among the six big industry sectors, Food, Beverage & Tobacco Products remains the strongest, while Transportation Equipment is the weakest. Overall, sentiment this month is marginally positive regarding near-term growth,” says Fiore.

The report, while still consistent with overall GDP growth of 1.3%, was the weakest since June 2009.

- December auto sales (still waiting for Ford) were weaker than expected. The chance of a fifth straight 17 million+ year has diminished. (Automotive News).

- Rail traffic declined 9.4% in December and was down 5% for 2019. Steven Hansen (GEI), as usual, tracks the decline not only in gross terms but also using “economically intuitive sectors.” (These remove coal, grain, and petroleum).

The Ugly

A grad student smuggling cancer lab specimens to China. (TheScientist). Prosecutors think it might be part of a larger effort. Harvard was sponsoring the student’s visa.

The Beautiful

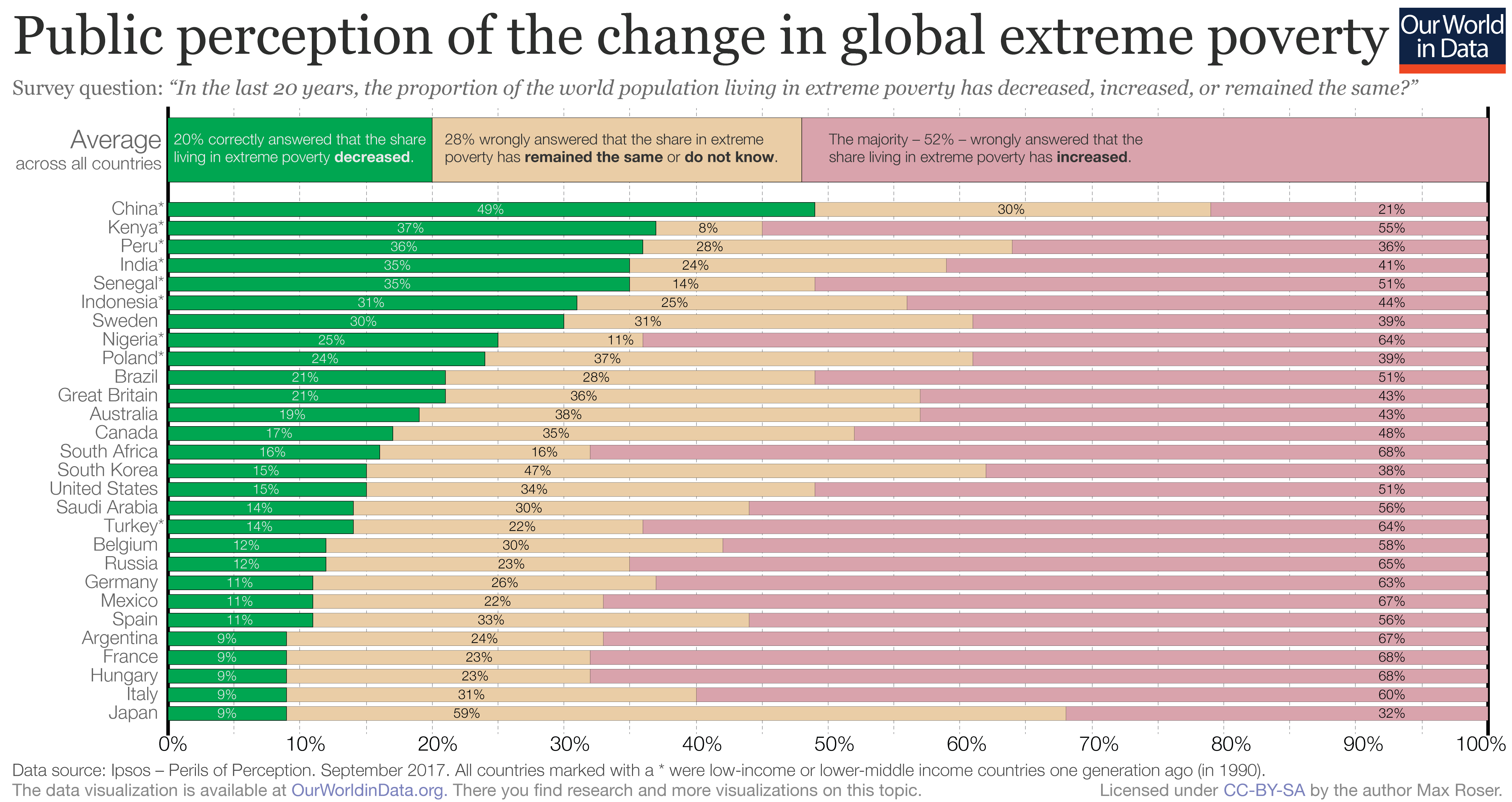

Nicholas Kristof opines that This Has Been the Best Year Ever. Looking at overall humanity he considers many metrics, all showing substantial improvement in quality of life and health. Here is a key quotation and one example.

Yet I fear that the news media and the humanitarian world focus so relentlessly on the bad news that we leave the public believing that every trend is going in the wrong direction. A majority of Americans say in polls that the share of the world population living in poverty is increasing — yet one of the trends of the last 50 years has been a huge reduction in global poverty.

Morgan Housel takes up a similar theme, 2020: What a Time To Be Alive. His approach is to look at progress during the last 38 years, the median age of Americans. He emphasizes that there is a lag in implementing progress, and then describes a number of key improvements.

The Week Ahead

The economic calendar is important, featuring the employment situation report and ADP’s private employment change as well as the ISM non-manufacturing index.

Congress has returned from recess. Fed officials will be in action.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The return of vacationing market participants is always an occasion for reassessment. Investment committees will meet, economic data studied, and allocations adjusted. Normally this would be a key story. It will still play out that way, but we won’t hear much about it. The employment report will still get special attention. (See today’s “worries” for my own take).

But these are all matters which have been hashed and rehashed in the financial media. The accelerating Middle East conflict offers many fresh themes, each begging for expert analysis. Expect the focus to be: Will Middle East conflict bring an end to the bull market?

Background

Readers of this column already know the basic facts, so I will keep the background section brief. As always, I’ll include sources that provide more depth for those who are interested.

The US executed a direct deadly air strike on Iran leader Qasem Soleimani. This action is various described as necessary to stop yet another threat to American lives by someone with “blood on his hands,” an assassination, and an act of war.

Whatever the justification, the action dramatically changed the military, political and economic dynamics.

Iran is promising aggressive retaliation. (Fox News). “Some 35 ‘American targets’ including ‘destroyers and warships’ are threatened.

President Trump threatens reprisals for any attack by Iran. (Washington Post).

The BBC asks, “Why kill him now and what happens next?”

As for the rocket attacks against the US bases in Iraq, the Pentagon has already hit back against the pro-Iranian militia believed to be behind them. That prompted a potential assault on the US embassy compound in Baghdad.

In explaining the decision to kill Soleimani, the Pentagon focused not just on his past actions, but also insisted that the strike was meant as a deterrent. The general, the Pentagon statement reads, was “actively developing plans to attack US diplomats and service members in Iraq and throughout the region”.

With the background in mind, I will take a deeper look at three themes and the possible market effects: military, political, and economic. Once again, I will use the recent format that readers seem to like. The column on the right is my evaluation of the evidence – at least what we have so far.

|

Military |

Jeff Comments |

|

Direct escalation against US personnel in the Middle East |

This is so widely threatened that it must be expected. |

|

Escalation on US soil. |

No one really knows. Presumably terrorism attacks were already at a high level. |

|

Escalation involving other countries. |

If prior actions are a guide, most other countries will steer clear. Again, it is all guesswork at this point. |

|

Politics Reports |

Jeff Comments |

|

The political divide has growth even wider. Speaker Pelosi complains that she and other Congressional leaders were left out of the loop before the surprise attack. The President and his allies do not seem to mind the act first, provide a briefing later approach. (The Hill). |

This does little to change the current political dynamic. With the impeachment process underway, how could the divisions get meaningfully worse? Key legislation has already been passed (avoiding a government shutdown, North American trade) and that is all we can expect for now. |

|

National security has become the big issue in the 2020 election race. The Democratic candidates generally opposed war and complained about the lack of consultation. Mayor Pete contrasted the action with decisions by Presidents Obama and Bush. The issue will also now be significant in the general election. (NY Times) |

The Democratic candidates were caught flat-footed on this issue. They had to respond to questions, but their positions need (a lot) more thought. For the market impact we first must figure out if it helps any particular candidate. Right or wrong, the immediate market reaction will be negative to Warren or Sanders ascendancy and more moderate on Biden. |

|

Economy |

Jeff Comments |

|

The immediate effects were clear: higher oil prices, a spike in gold (and Bitcoin!), a flight to safety in bonds and “safe” currencies, and lower stock prices. (Barron’s) |

These are all typical knee-jerk reactions to crisis news. Human or robot traders react according to the playbook. Barron’s did a good job of rounding up some comments on short notice. Next week will provide a better read on the reaction of investors and managers with a longer time frame. |

|

Overall impact of a collapse in Iran’s economy (still from Barron’s) is estimated as a reduction of 0.3% in global GDP. Prices on Brent Crude could reach $150 per barrel creating a boost to inflation if Iran closed the Strait of Hormuz. |

I doubt that Iran can close the Strait of Hormuz. Any spike in oil prices will be short-lived, since there is idle capacity. This is the most important direct impact with potential for a longer term effect. That said, there is certainly some pressure on the global economy. |

|

The market was “priced for perfection” with a lack of global conflict assumed by all. |

This is a typical comment from people on my Twitter list of “reliably bearish commenters.” No one really knows what has been priced in, but their position suggests that no is reading what they have contended for years. |

|

This is the “black swan” event we have all feared. |

The chances for a cascading effect are low because dealers are “long gamma.” This means that they benefit from big moves and buy into them. There are good reasons to expect a tempered short-term effect and time to evaluate in the intermediate term. (The Heisenberg). The long gamma explanation helps to explain why the Friday reaction was “muted” in the eyes of many and included a rebound. This is exactly what you would expect of the “B-Team” was trading around a position with a lot of “curvature.” |

I’ll have some additional observations in today’s Final Thought.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both long-term and short-term technical indicators remain neutral, but continue to show improvement.

The C-score has moved lower implying greater odds of a recession within the next nine months. Since May we have been watching for confirming data. Like others, we don’t see much of that. Most sources have lowered recession odds, so why has the C-Score fallen? The potential for inflation. So far, so good on that front, but it is important to keep the Fed out of play while we start to enjoy reduced trade war effects.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian updates the regular quarterly and annual cycles in earnings forecasts. His important conclusion?

This is what most retail investors miss about SP 500 earnings as a forward quarter is added and the back quarter falls off, the trend is inexorably higher.

Brian also updates the 2020 growth rates by sector.

Guest Sources

David Templeton analyzes a popular strategy in Dow Dogs 2019 Return Unable To Keep Pace With Broader Market. He discusses the component sectors as well as holdings removed and new holdings for 2020.

The Daily Shot reports on inflation expectations in the University of Michigan survey. This will become important someday.

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone. My colleague Todd Hurlbut, Chief Investment Officer at Incline Investment Advisors, LLC has been collaborating on this series. The most recent post was Time to Batten Down the Hedges? We take up the question of risk control and whether to prefer stop loss orders or hedging. As always, the trading models share some recent action which Todd analyzes.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Tim Duy’s analysis, Are Stocks Overvalued? The leading Fed expert was dragged into this topic via the back door. He became frustrated with the many short-sighted analysts attributing the rally in stocks to the changes in the Fed’s balance sheet.

My own frustration began years ago. The misconceptions around valuation are responsible for trillions of dollars in losses or missed opportunities. The media consensus on a handful of lame valuation methods legitimizes the descriptions of “frothy” or “elevated” and makes any dissenter seem foolish. Despite the ongoing failure of these methods, the proponents keep reaching for explanations for the “temporary” deviation from true value. My post on this topic, The Fed as a Fig Leaf, was published nearly seven years ago. It has survived the test of time.

Prof. Duy’s plain, careful, and authoritative explanation should set things right for any open-minded reader. He has several key conclusions which investors should consider carefully:

- The path of equities is pretty normal for an economic expansion.

- The current market does not look like that of the late 90’s.

- The Fed has neither created a bubble or set the stage for another bubble.

- A less optimistic view of the world has already been priced into equities.

And importantly, he responds to those reaching for a “QE” explanation – another that I have often mentioned myself. (No wonder I think this is the best story of the week!)

How does QE or, more generally, monetary policy fit into this story? To the extent that the Fed sets policy in a way designed to kill your recession call, it will support a general uptrend in equity prices over time because the economy remains in expansion. If the Fed commits a policy error or is unable to respond to a negative shock with sufficient speed and the economy tumbles into recession, I would expect equities to follow the economy down. With regards to the most recent months, I think the equity moves have more to do with a reduced risk of recession than repo-related balance sheet changes.

And finally:

Bottom Line: I don’t think you need to fall back on “it’s all QE” to explain the behavior of equities this past year or this cycle. It appears to me that the general path of equities is what should have been anticipated given continued expansion. To the extent the Fed is involved, it is because policy moves have sustained the economic expansion. It seems best to view the Fed as endogenous to the system not some conspiratorial exogenous factor.

This is as close as investors will get to commentary from an expert with no dog in the hunt. Take it seriously!

Stock Ideas

Dividend Sensei identifies 5 Stocks I’m Buying For My Retirement Portfolio In 2020. The long article includes a lot of macro speculation, and my main interest is in the five stocks. Each gets a “Chuck Carnevale style” analysis of valuation and trends along with some background. I own one of the five and have two others on my watch list. As always in this section I am providing ideas for your own research.

Biotech In 2020: M&A And Gene Therapy In Focus is an interesting roundtable including expert opinion and some ideas for further research.

Ben Levisohn (Barron’s) writes Lennar Stock Looks Like a Bargain. Here’s Why. While upcoming earnings may reflect a soft quarter, the stock is cheap and prospects are “lining up.” I agree. And I like the company’s new emphasis on starter homes.

Beth Kindig explains the reasoning behind her accurate call on Microsoft’s successful bid for the Defense Department’s cloud business. While that decision has been made, the description of the technology differences and the importance of hybrid cloud computing are important information for anyone investing in the cloud computing space.

Want Yield?

Blue Harbinger observes: Exxon Mobil: 5% Dividend Yield Is Near A 25-Year High. He also likes the upside potential and strong balance sheet.

Barron’s published it’s eighth annual review of income-producing parts of financial markets. They discuss and rank 12 sectors and mention quite a few specific names. They warn, however, that:

After a broad global rally in stocks and bonds, income-oriented investments offer fewer opportunities than they did a year ago.

So investors will need to lower their expectations. But there are still places to look for yield on a range of stocks and bonds. And income will be welcome if markets turn more volatile.

The Great Rotation

There is a tall order for the next phase of the trade agreement.

Watch out for

Aurora Cannabis (ACB) has a “problematic profit picture” opines Stone Fox Capital. Loss of key people and insider selling are warnings.

Micron Technology (MU) is fairly valued despite the low P/E. Valuentum’s concern is the overall DRAM market and geopolitical risk.

Boeing (BA). The culture behind the 737 Max crisis is deep-seated. Natasha Frost (Quartz) traces it back to a 1997 merger.

Final Thought

I don’t know whether the strike against Soleimani will mark the beginning of the end of the bull market and neither does anyone else. I included most of my thoughts in the discussion section. I see a typical knee-jerk reaction – a rush to the obvious. What should investors do?

Barron’s has suggestions with the evergreen “how to position your portfolio” angle. You can hedge, buy dips, or trade the volatility in oil prices. Of the three, the only one I like is the airline angle. Fuel is a declining portion of airline costs and the oil price spike might not stick.

It is tough for journalists to crank out articles on a topic like this on short notice. I sympathize. Investors need not rush into these ideas. We do not know how this story will play out, and we are not required to guess. In general, news of attacks, conflicts, and even limited warfare has been more of a headline story than an economic story.

Traders might feel the need to rush, but investors should not. It is a critical time. Get it right.

Great Rotation Hint of the Week

Look for stocks that are value-priced, represent emerging markets, and will benefit from improvement on the trade front. Michael A. Gayed’s analysis of Tata Motors (TTM) provides information on all of these points. It is a stock I have been watching for more than a year. It is a good candidate for the Great Rotation theme.

Some other items on my radar

- I am concerned about an over-reaction to the employment report. Wide deviations from sampling error are completely normal. In the moment, most people forget this. The bearish community has teed up this report as an indicator of the spread of manufacturing weakness to consumers.

- I am concerned about inflation! Will tight labor markets start to create cost pressures on companies?

Disclosure: Has your portfolio kept up with the changing times over the last year? If you look at it, is your reaction, “Oh, this is so 2009?” If you are unsure, write for my brief ...

more

{kind=link}