Yen & USD Capitalize On The COVID-19 Crisis

As the Euro keeps selling off amid concerns of the spillover effects of a Chinese slowdown for the German economy, two currencies have proven to navigate these murky waters with the most resilience. I am referring to the appeal of the US Dollar and the Japanese Yen, the latter hanging in there despite all-time highs in US equities. The Pound is another currency defying the odds, even if it's being driven by ts own set of idiosyncratic matters. For a full scan of where we stand in FX, keep reading...

Quick Take

Last Friday was one of those uninspiring days with minimal flows in the G8 FX complex. Buy on dip strategies continue to thrive in the British Pound and US Dollar markets, while the Japanese Yen has firmed up its stance in recent days too, despite fresh record highs in US equities. These currencies are by a large margin the strongest since the unraveling of the coronavirus crisis in China, even if the Pound trades based on factors largely non-related to the drama China is undergoing as Brexit/politics-led stories play the bigger role. Therefore, it is safe to say that the USD and the JPY are by far the fiats drawing the most demand by such an uncertain landscape.

The coronavirus has led, on the contrary, to the Aussie and Kiwi, now joined by the outperformance of the Euro, as the other group of three currencies most punished by this new dynamics in the market. As weeks have rolled by and the market keeps working out the ramifications of the coronavirus, this fall in the Euro to multi-year lows appears to carry a clear message about the impending risks of a more dovish ECB heading into the March meeting. The story here is that when ‘China sneezes, Germany catches a cold (no pun intended)’, so the market is betting on this Chinese drama to re-instill economic sluggishness in Europe, something that the ECB may have to act upon through easier tools.

On the flip side, the Kiwi is emerging as a contender to exploit significant upside room judging by the depressed levels it trades at, even if this os based on the assumption, made by the RBNZ itself, that the virus will ‘peak’ relatively soon. The balance of risk offers an attractive long bet in the NZD if one believes that the worst of the coronavirus is behind us, which judging by the behavior in the equity market, it certainly hints as it is. However, equities have become a rather obsolete tool to act as the true barometer. As traders, you’d be better off gaining insights if the recovery also emerges through key breakouts in the Yuan or long-dated bond yields.

Another currency that keeps challenging higher ground is the Canadian Dollar, finally achieving a technically bullish breakout in the daily when analyzing the index. Lastly, in what portrays the progressive demise of the strongest trend for most of 2020, the Swissy keeps debilitating and judging by the reading of aggregated flows, it is no longer in a daily bullish cycle.

(Click on image to enlarge)

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Institutional Bank Research reports.

US retail sales fall short but consumer sentiment offsets: The US Jan advance retail sales came at +0.3% vs +0.3% expected, even if the control group came quite disappointing at 0.0% vs +0.3% expected, alongside a sizable downward revision to December. The overall flows into the USD were positive for the day nonetheless, as bullish technicals and the February prelim U Michigan consumer sentiment, at 100.9 vs 99.5 expected (highest since March 2018), partially offset the negative input via the retail sales.

Soft Germany/EU growth figures to end 2019: Germany’s Q4 preliminary GDP came soft at 0.0% vs +0.1% q/q expected, while the GDP non-seasonally adjusted stood at +0.3% vs +0.2% y/y expected. Notwithstanding the figure were poor as it shows an economy stuck in first gear, this negative input has already been priced into the low valuation of the Euro. Similarly, the Eurozone Q4 GDP second reading came unchanged at +0.1% vs +0.1% q/q preliminary.

NZ services PMI fits upbeat RBNZ storyline: New Zealand services PMI for January came at 57.1 vs 52.1 prior, the highest since January 2019. According to BNZ Senior Economist Doug Steel: January's glowing PSI report fits with the rather upbeat view of the economy expressed by the RBNZ last week. In the least, it helps offset a still soft looking PMI. Regardless, the near term outlook heavily depends on how much - and for how long - disruption occurs as a result of local weather conditions and COVID-19."

UK defying stance on tax, workers’ rights: On Brexit, the latest we’ve learnt is that the UK is set to refuse to abide by EU rules on tax and workers' rights after Brrexit, The Telegraph reports. “UK negotiators are expected to insist that the UK should be given a deal akin to the EU's agreements with countries such as Canada, Korea and Japan, which they say involve less stringent requirements than those set out in the draft mandate.” This defying tone is yet another good representation of the friction that exists and the challenges ahead for the UK to get away with the deal it wants with the EU.

The latest coronavirus numbers ‘too perfect to mean much’: The latest coronavirus official numbers show, as for Feb 15, 68,500 total cases and 1,665 dead. Hubei province (the capital city and epicentre of the outbreak) has enacted tougher vehicle movement restrictions and has instructed firms not to reopen without government approval. However, as Barron's notes, China's coronavirus numbers are "too perfect to mean much." The note from Barron’s, via ZeroHedge, reads: “A statistical analysis of China’s coronavirus casualty data shows a near-perfect prediction model that data analysts say isn’t likely to naturally occur, casting doubt over the reliability of the numbers being reported to the World Health Organization.”

Singapore tells markets brace for possible recession: Singapore reported 9 new coronavirus cases last Friday, bringing the total cases to 67. The country is currently at risk of classifying the virus as a pandemic situation. Singaporean prime minister, Lee Hsien Loong, said via the Straits Times, that a recession is possible due to the economic impact of the coronavirus, adding that the coronavirus impact on the economy already exceeds that of SARS back in 2003.

Looser fiscal policy in China, HK, Singapore eyed: Governments in the countries most affected by the coronavirus, including the US, China and HK, are being cornered to provide extra fiscal stimulus to ease the economic slowdown. As Bloomberg reports, “China said Sunday it will enact more-efficient stimulus measures despite a widening fiscal gap, including lower corporate taxes. Hong Kong’s top finance official said the city is facing “tsunami-like” shocks that may lead to a record budget deficit. Singapore is headed for its biggest budget gap in almost two decades, according to analysts.”

Talk has it OPEC+ may cancel emergency meeting: Amid the recovery in the price of Oil (first weekly gains since the first week of January), there are reports suggesting that OPEC+ is close to dropping the idea of an emergency meeting and will instead stick with March meeting dates, according to delegates cited by Bloomberg.

Market bets for a dovish Fed as the year progresses: The amount of hedges in case the virus contagion is a disaster for the global economy kept increasing last week. As Bloomberg reports, some of these bets are now clearly biased towards the Federal Reserve forced to to reduce interest rates, as the increase in eurodollar options activity reflects. In this new change of positioning observed, traders would profit “if the central bank delivers more than the one-to-two quarter-point cuts already priced in for 2020” Blomberg notes. “The impact of the virus on the global economy is going to be significantly more than what people are expecting, and when the global economy goes south, the Fed steps in,” said Tony Farren, managing director at broker-dealer Mischler Financial in Stamford, Connecticut.

U.S. raises tariffs on European aircraft: The U.S. government on Friday, via a statement released by the USTR, said it is set to increase tariffs on aircraft imported from the EU to 15% from 10%, increasing pressure on Brussels in the ongoing dispute over aircraft subsidies. The higher aircraft tariff will take effect March 18. The USTR also announced that it would make minor modifications to 25% tariffs imposed on cheese, wine and other non-aircraft products from the EU, including dropping prune juice from the list. Full details in this Reuters article.

Several rockets hit a U.S. coalition base in Baghdad: Hopefully, despite the attack, there were no casualties, Reuters reports, citing a coalition spokesman, in what constitutes a series of ongoing attacks to target U.S. facilities in Iraq. As Reuters notes, “Washington has blamed Iran-backed paramilitary groups for increasingly regular rocketing and shelling of bases hosting U.S. forces in Iraq and of the area around the U.S. Embassy in Baghdad.”

US markets closed: It’s going to be a quiet US trading session, barring any unexpected news, in observance of US Presidents Day holiday with both stock and bond markets closed.

Recent Economic Indicators & Events Ahead

(Click on image to enlarge)

Source: Forexfactory

Insights Into FX Index Charts

The EUR index continues en-route to target its next 100% measured movement after the vindication that a fresh bearish cycle is in play following the breakout of a key pivot low. With the exception of one doji candle last week, the Euro has now fallen for 9 straight days, with price action still communicating that interest to sell on strength is well and alive. There is no evidence whatsoever of a market with the slightest appetite to build EUR long inventory just yet as sellers have cemented the grip. My core view, thus remains that this is a market exploitable through sell-side action on retracements at regular intervals in line with technicals.

(Click on image to enlarge)

The GBP index is a whisker away from targeting its previous swing high, currently with the backing of the smart money tracker and a break of structure. Opposite to what we are seeing in the Euro, this is a market that has seen the order flow shift to support buy on dips, as depicted by the price action displayed last Friday. This market has further yet minimal upside to go before the next decision point, which may see the balance tilt towards a breakout into fresh trend highs or alternatively, carving out what would represent the making of a new broader range.

(Click on image to enlarge)

The USD index remains a solid bet to buy on dips, and based on the price action when combining the flow in the G8 FX complex seen in the last 3 days, this remains a valid prognosys to capitalize on. This view is supported by the market structure and the smart money tracker, as the USD remains the top performing currency in this new decade. Not only is the trend in favor of buying, but from an intermarket perspective, the USD has proven immune to the risk profile at play, with buying unabated regardless of risk on or risk off in the markets. There is further room to exploit to the upside until the next key level of resistance is met.

(Click on image to enlarge)

The CAD index has, at last, broken into daily bullish territory by breaching the previous swing high, even if the volume this break carries is suspiciously low. Nonetheless, for now it represents a sign of further strength when analyzing the aggregated flows into the Canadian Dollar, and I am officially no longer a bear in this market as we now have the break of structure to bullish backed up by the smart money tracker also pointing bullish. In the current phase of carry trades being promoted again as equities rise and bond yields stabilize, the CAD is one of the prefered bets to get paid relatively high yields, another positive factor to account for in favor of longs.

(Click on image to enlarge)

The JPY index has found an increase in the demand flows at a critical level of support, raising the prospects that a double bottom may be seen. Nothing has changed in the last 24h of price activity. The market profile that best defines this market for now is range-bound until there is a resolution below the equal low or above the previous swing high. Until that’s the case, the technicals are not as clear cut as they were in previous weeks, even if the overall macro bias remains rather positive as the market consolidates above the previous broken swing high with the smart money tracker still pointing mildly to the upside for now.

(Click on image to enlarge)

The AUD index remains capped by a sticky resistance line overhead, disallowing further gains for now, as the coronavirus keeps playing a critical role to determine the daily ebbs and flows. I must say that the aggregated tick volume on the second retest into this resistance has been far from compelling as the buy-side volume activity plunged, which is not a positive gauge when measuring the commitment for buyers to break this tough technical level. The price structure of lower lows and lower highs continues to be in place, so even if the slope of the smart money tracker has turned bullish, it does not yet vindicate the bullish bias until acceptance above.

(Click on image to enlarge)

The NZD index, led by the RBNZ hawkish surprise, broke its previous swing high in a show of strength that I believe has credence to find further legs up. The currency has already retraced from overbought conditions, which makes the prospects of buy on dips an attractive proposition. While the smart money tracker is yet to turn bullish, the structure of this market has been altered, and the next question that lies ahead is. Will the index evolve into an uptrend, or will the recent high prove to be the precursor to a broad range about to settle in? If we continue to see the gradual fading of the coronavirus woes, coupled with the new neutral stance by the RBNZ, this could be the recipe to one of the best trends to jump on in coming weeks/months.

(Click on image to enlarge)

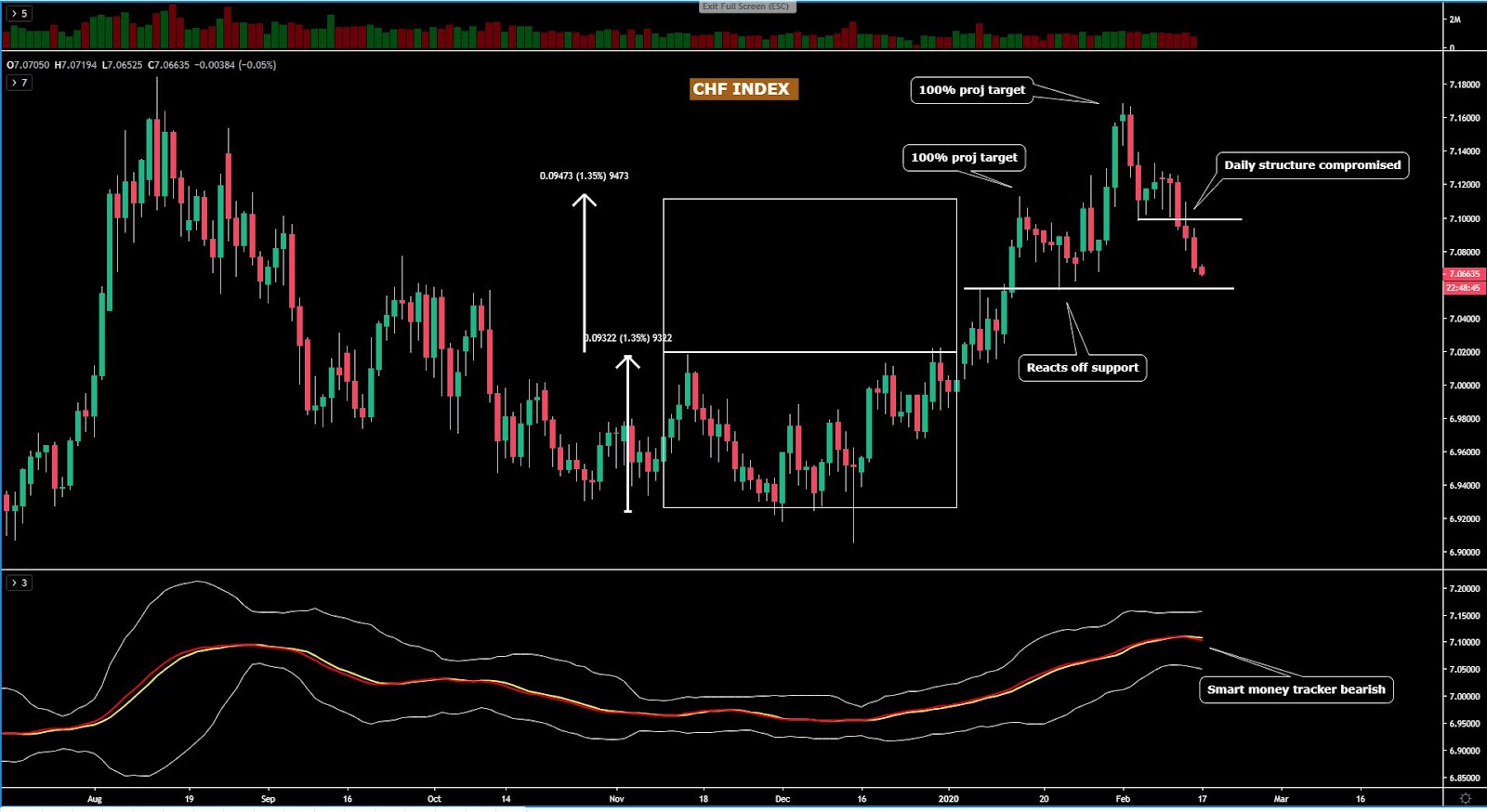

The CHF index, technically speaking, had its first breakout of structure at a time when the smart money tracker had already re-aligned to the downside. The CHF is now headed towards a key level of support near-by, hence the downside is quite limited before we encounter potential buy-side pressure. But the reality is that buyers no longer have the upper-hand to remain the dominant force in this market as technical readings no longer back them up. The Swissy could go either way short-term, but the market is giving us indications that the tide has turned.

(Click on image to enlarge)

Important Footnotes

Market structure: Markets evolve in cycles followed by a period of distribution and/or accumulation. To understand the principles applied in the assessment of cycles, refer to the tutorial How To Read Market Structures In Forex

Horizontal Support/Resistance: Unlike levels of dynamic support or resistance or more subjective measurements such as Fibonacci retracements, pivot points, trendlines, or other forms of reactive areas, the horizontal lines of support and resistance are universal concepts used by the majority of market participants. It, therefore, makes the areas the most widely followed and relevant to monitor. The Ultimate Guide To Identify Areas Of High Interest In Any Market

Fundamentals: It’s important to highlight that the daily market outlook provided in this report is subject to the impact of the fundamental news. Any unexpected news may cause the price to behave erratically in the short term.

Projection Targets: The usefulness of the 100% projection resides in the symmetry and harmonic relationships of market cycles. By drawing a 100% projection, you can anticipate the area in the chart where some type of pause and potential reversals in price is likely to occur, due to 1. The side in control of the cycle takes profits 2. Counter-trend positions are added by contrarian players 3. These are price points where limit orders are set by market-makers. You can find out more by reading the tutorial on The Magical 100% Fibonacci Projection

The Daily Edge is authored by Ivan Delgado, Head of Market Research at Global Prime. The purpose of this content is to provide an assessment of the market conditions. The report takes an in-depth ...

more