Why Staples Is A Strong Buy In 2015

A) Introduction

On Tuesday, a FT report came out saying that Staples (NASDAQ:SPLS) was likely to reject calls from activist Starboard Value to merge with competitor Office Depot (NASDAQ:ODP), sending the stock down nearly 6%. Whether you believe Staples will give into the activists or not, we believe that Staples offers an attractive valuation and price momentum. We will begin by taking a quantitative look at how Staples stacks up in a variety of different valuation and growth metrics, before providing qualitative analysis on the activist situation.

We should note that we take a quantitative approach to investing, preferring to focus our analysis on a certain set of metrics that have a strong predictive ability. Thus, we tend to analyze academic papers and perform historical back tests on different metrics before including them in our analysis. We will provide links to the academic papers we draw inspiration from as we progress through our breakdown of the stock so investors can see for themselves what we base our conclusions on. Investors looking to learn more about our analytical style can do so here.

B) Valuation Breakdown

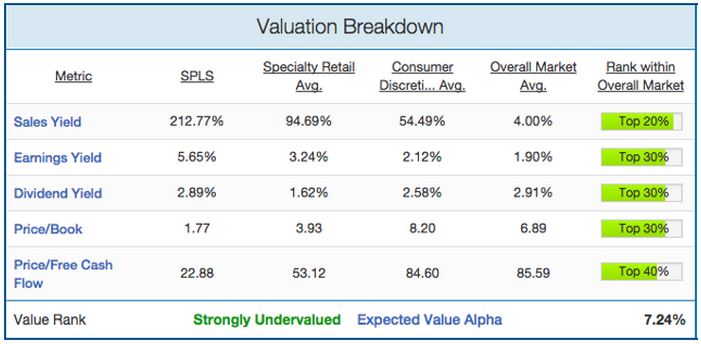

We'll start by analyzing Staples value profile. This is important to look at as "Value stocks (with low ratios of price to book value) have higher average returns than growth stocks (high price-to-book ratios)". Staples valuation profile is shown below:

There are a few important things to note from this table. First off, Staples finishes in the top 40% of the entire market in every valuation metric shown above. Of these, Staples is most undervalued on a revenue basis with its sales yield of 213% being way below the Specialty retail (95%) and consumer discretionary sector average (55%). The company looks fairly attractive on a earnings and dividend basis, with its earnings yield of 5.65% and dividend yield of 2.89% both much higher than the specialty retail averages (3.24% & 1.62%). Staples also looks attractive on a book value (P/B ratio of 1.77 vs. group average of 3.93) and free cash flow basis (price/FCF of 23 vs. group average of 53). As shown in the link above, value stocks tend to produce significant excess returns, which bodes well for Staples in 2015. Overall, the stock is strongly undervalued relative to its group peers and we expect the stock to generate 7.24% of outperformance due to this undervaluation.

C) Growth Breakdown

There are a variety of different growth metrics that have been shown to predict stock returns. Most important among them is price momentum. Winning stocks keep winning, and losing stocks tend to keep losing. Staples growth profile is shown below:

Rumors of a potential merger with Office Depot have sent Staples up 51% in the last six months, after it had started the year off weakly. This six-month price performance puts it into the top 10% of the overall market over the last six months, reflecting its new-found status as a market leader. As we detailed in reports on Best Buy (BBY) and Kroger (KR), retail stocks have been leading the market recently as investors capitalize on the expected increase in consumer spending due to cheaper gas. While Staples big run has been mostly due to rumors of activism, they should benefit from the retail sector comeback as well. Overall, we feel that Staples is a "Strong Growth" company and will outperform the market averages by 6.11% over the next twelve months due to its growth.

D) Qualitative Analysis & Conclusions

We'll now supplement our quantitative analysis with a qualitative discussion of some of the major growth catalysts and risk factors that could impact the stock price in the near future. As we mentioned at the start of the article, Staples shot down the proposed merger between Staples and Office Depot on Tuesday, citing concerns over FTC approval. While this news sent the stock down 6% on Tuesday, Staples recovered half this fall over the next three days, showing that the market was still optimistic on a potential deal. Staples fears of FTC resistance stem from the previously failed merger with Office Depot in 1997, in which the FTC cited antitrust concerns regarding "office supply superstores". The FTC has relaxed this narrow definition now that Internet retailers like Amazon (AMZN) and Ebay (EBAY) have taken significant market share. This is shown by their recent acceptance of the Office Depot/Office Max merger in 2013. The FTC knows that office supply stores cannot impose monopoly-like pricing in the internet age, and thus is likely to approve the merger.

Considering this recent historical precedent, the fact that Starboard (the activist behind the Office Depot/Max merger) is the driving force, and that the steady loss of market share to internet retailers is forcing industry consolidation, there seems to be a very good chance that the proposed merger will eventually go through. With that being said, even if the proposed merger between Staples and Office Depot does not go through, we believe Staples combines an attractive valuation with strong profit growth, and price momentum. Thus, we recommend Staples as a "Strong Buy" and expect the stock to continue its outperformance in 2015.

Disclosure: The author has no positions in any stocks mentioned, but may initiate a long position in SPLS over the next 72 hours. The author wrote this article themselves, and it expresses their ...

more