When Defensive Assets Stop Working

What if I told you there was a bubble but it wasn't in risk assets? What if I told you that the assets most investors look to for safety and capital preservation could actually be the biggest source of risk in portfolios right now?

OK, if I haven't lost you already, yes that does sound a bit cheesy and smacks of the scaremongering that a lot of pundits use to sell their subscriptions (and why yes, I do have a subscription to sell you, but that's a matter for a different time!). So I apologize for upfront for the douchey intro.

But then again, once you check out some of the charts I'm about to show you, it might actually begin to make a little bit of sense...

On my metrics, the traditionally defensive assets are looking very richly priced, and I guess you can't blame investors for crowding in. You've got NIRP/ZIRP all over the world, QE/"not QE", trade wars, political BS 24/7 (to put it euphemistically), scary headlines, crappy data, and late-cycle lamentations. Simply put, it's easy to explain why you're overweight bonds, REITs, and gold when the global PMI is below 50 and the next selloff is only a tweet away.

But what if things change?

What if the global economy experiences a rebound instead of a recession? What if all that other crap starts to fade (or heaven forbid, political risk surprises to the upside)? What happens to defensive assets if we get a full blown late-cycle-extension?

1. Valuations: defensive assets are extremely expensive

As I alluded to, based on my proprietary mix of valuation indicators the average valuations across the defensive assets (treasuries, REITs, gold) is at the most expensive level on record. Meanwhile, the average across US equities, international equities, and commodities (growth assets) is still around quite reasonable levels. Simply put: defensive assets are very expensive, and growth assets are cheap. This is basically a market-based measure of a profound level of fear, uncertainty, and pessimism on the economic outlook.

What to watch for: valuations often have little influence on short-term timing decisions except for where extremes are reached, but over the medium-longer term valuations are virtually all that matter (other things are important too, but valuation is a biggie). So the big open question here is can defensive assets still "work" or reduce risk when they are this overvalued?

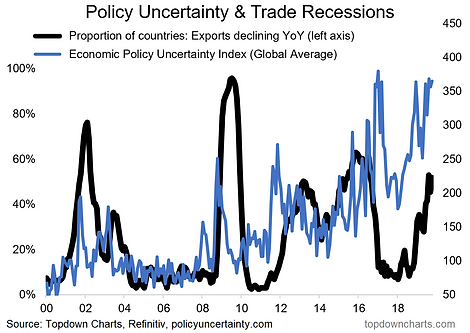

2. Mass Distraction: policy uncertainty and deflation waves

This chart requires a little bit of explanation. The blue line is the global average economic policy uncertainty index (index which is based on algorithms that read news articles and track the mentions of words/phrases associated with greater levels of economic policy uncertainty). The black line is the proportion of countries that have recorded declining exports on a year-over-year basis (i.e. an export 'recession'). What it's telling us is that policy uncertainty is near record highs, and roughly half of the world is experiencing an export recession. In other words, it's a graphical representation of crappy hard data (which by the way is backward-looking), and heightened bad news/noise flow (again, at best a coincident indicator - and often a contrarian indicator from a risk-taking standpoint). Hence my quip on mass distraction.

What to watch for: bad historical data and heavy bad news flow as mentioned tend to be actually good times for risk-taking. To be fair, defensive assets rally into an environment like this (hence why we have seen valuations run up so intensely). But from a contrarian perspective, this is a great chart. The phrase "so bad it's good" comes to mind.

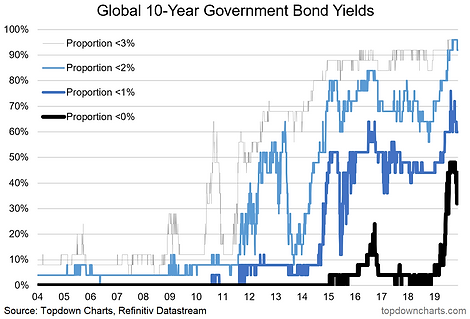

3. Mass Distortion: the surge of negative yields and experimental policy

This chart looks across the global sovereign 10-year bond universe and checks what proportion of 10-year government bond yields are trading below the respective brackets in the legend. There's a few things to cover on this, firstly the proportion of 10-year government bond yields with negative yields peaked at 48% in September (96% below 2% and 76% below 1%). Second, there are clear successive waves/spikes in the proportion of bond yields plunging through the successive lower limits. Thirdly, while government bond yields are clearly influenced by the softer growth/inflation pulse and risk aversion/hedging demand, central bank policy also obviously is a substantial influence given the bond buying programs. Given how bond yields (real and nominal) play a critical role in pricing many other assets, you can understand why I tagged this one 'Mass Distortion'.

What to watch for: aside from the distortive impact on other asset classes from negative yields and just plain lower bond yields, this chart has a hidden utility. Adroit observers will note that each successive wave and spike in breadth basically coincided with a cyclical peak in bonds (trough in yields), and it's no different this time - I actually used this chart back in Aug/Sep to make that point. So again, it's more of a sign of a turning point than a new normal or doomsday as such.

Final Thoughts and Bottom Line

Bottom line: the combination of a softer growth/inflation pulse, elevated uncertainty/fear, and (experimental) central bank policies, has seen investor herding drive defensive assets to trade at extreme expensive valuations.

The trouble with this herding into defensive assets is that those who've gone all-in on defensive assets (or those that are locked into such a strategy by investing in/being placed in "conservative" portfolios) could be at risk of a rapid 'repricing' (another euphemism) of defensive assets. In other words, defensive assets could become a source of risk rather than a hedge against risk. To be fair, if the world does tip over into a deep/prolonged recession or if disaster does strike then defensive assets will likely serve their diversifying purpose. But to me, it's another sign (along with lower expected returns) that active asset allocation is a worthwhile function, even if just for risk management purposes. It also means we ought to challenge traditional wisdom and apply some thoughtfulness rather than deferring to rules of thumb or correlations of bygone eras.

For more and deeper insights on the global markets, good charts, and actionable investment ideas you may want to more