What You Need To Know About Bear Markets

The bullish pundits of the Twittersphere; the pros who never met a stock market they didn’t like, grow increasingly quiet at these times; or masterfully through the art of words, combined with short memories of investors and blatantly false narratives, still manage to maintain their personas as ‘market mavens’. As wordsmiths, they cleverly ameliorate the damage that market bears create.

It is crucial for investors to do their own homework, seek second opinions, and not allow their financial partners and the media to minimize the potential carnage bears can inflict on portfolios and financial goals.

So, what is a bear market?

A bear occurs when stock prices fall 20% from the previous high. Unfortunately, we haven’t had a bear market in years; even corrections (10% off the prior high), feel much worse. Spirit memories of the financial crisis are beginning to stir; investors I encounter have 2008 and 2009 in their thoughts and on their lips. Personally, I don’t believe this is redux of the Great Recession. However, I’m sort of relieved how investors bring it up only because the recent market routing is shaking up complacency.

A few facts as of this writing:

Small-cap indices are in an official bear market.

More than half of S&P 500 large company stocks are in bear market territory.

Energy, financials and materials sectors are in a bear markets and industrials are at the cusp.

Utilities, healthcare and consumer staples as the ‘defensive’ areas of the stock market are in correction or pullback which makes sense as money tends to flow to these sectors when the crowd belief is an economic slowdown or recession is imminent. Intuitively, it makes sense – Regardless of economic conditions, consumers are still going to eat, turn on their lights and require healthcare. Ostensibly, as market conditions deteriorate, these sectors inevitably falter.

So, what is the money truth about bear markets?

They occur more often than you think or are told by pundit guests on financial entertainment channels.

I know. Shocking.

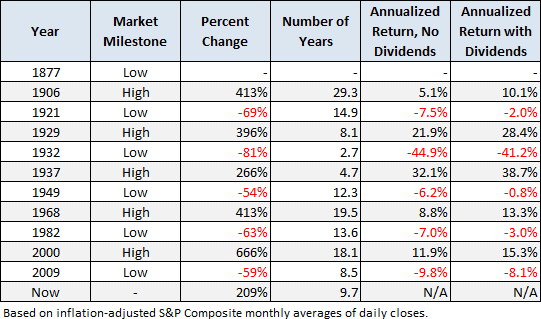

Doug Short, one of the finest and thorough economic and market analysts next to Lance Roberts, busts the myth which appears prevalent in media: Bear markets occur 20% of the time, bulls 80%. This is false and dangerous to believe.

Per Doug Short at www.dshort.com:

Since that first trough in 1877 to the March 2009 low:

- Secular bull gains totaled 2075% for an average of 415%.

- Secular bear losses totaled -329% for an average of -65%.

- Secular bull years total 80 versus 52 for the bears, a 60:40 ratio.

This last bullet probably comes as a surprise to many people. The finance industry and media have conditioned us to view every dip as a buying opportunity. If we realize that bear markets have accounted for about 40% of the highlighted time frame, we can better understand the two massive selloffs of the 21st century.

Don’t fall for dollar-cost averaging as salve for bear market agony. You’ll have a better chance to value average or lump-sum invest into stocks once markets settle down and recovery begins. Unfortunately, I have no idea when this turn will occur, so patience is required.

Let’s be clear: Dollar-cost averaging isn’t an investment strategy or a very good one, regardless of what you’ve been told. Don’t perceive it as such. It’s a method devised by Wall Street and touted by brokers to foster complacency.

Listen, a little complacency, a bit of auto-pilot can be positive to your bottom line; I agree that dollar-cost averaging is at the least a healthy financial habit.

Dollar-cost averaging is nothing special. It won’t do anything for your overall returns. If one seeks mollification to avoid regret bias or other emotional salve, then it’s fine. Continue. However, at least consider the ultimate placement of the dollars. It doesn’t necessarily need to be the stock market. DCA seems to get linked exclusively to stock investing. Go ahead and unlink your mind from the false narratives.

It would be impossible and unrealistic for the financial industry to comprehend that dollar cost averaging into the S&P 500 may be less effective than tucked underneath the Posturepedic.

Naturally, nobody is suggesting to literally use your mattress as a deposit box. However, the point is that dollar-cost averaging was designed to be a sales tool to sucker you into investing and forgetting.

Not cool.

“The truth is that many advisers are smart, and they are aware that dollar cost averaging is not a good idea. But rather than trusting people to learn, they are happy to get a second-best solution. After all, dollar cost averaging has such a good image, why not capitalize on it?” – Presh Talwalker, Author of The Joy of Game Theory – An Introduction to Strategic Thinking.

A disciplined investor’s approach would be to adhere to the process (because it is a good one), and establish a periodic investment plan where a specific amount of money is auto-deposited into a portfolio mix allocated based not on the time frame required to reach a financial benchmark, but on the current risk exposure required to achieve return at this stage of the current market cycle.

Plainly speaking, fund a conservative allocation temporarily – then initiate larger, lump sum investments into riskier asset classes as valuations improve. How do you know when valuations improve? Well, that’s what a financial adviser is there for, isn’t it?

An individual I counsel who has been out of the market for five years decided on dollar-cost averaging 20 percent into stocks (split between U.S. and international), 30% in short-duration bonds, 20% in intermediate-term fixed income and the rest in cash.

She’s willing to give up some possible continued short-term upside and consider risk first, based on the valuation risk in stocks. Smart move. It’s a cake and eat it type of decision. If markets go higher, she participates. If they falter, her portfolio downside is muted.

Stock diversification is a big fail during bear markets.

Through this cycle you’ll be hearing the D word often. It’s supposed to make you feel better, but it won’t. And it shouldn’t.

Remember this: Diversification is not risk management, it’s risk reduction.

- When your broker preaches diversification as a risk management technique, what does he or she mean?

- It’s not risk management the pros believe in, but risk dilution.

- There’s a difference. The misunderstanding can be painful.

To you, as an investor, diversification is believed to be risk management where portfolio losses are controlled or minimized. Think of risk management as a technique to reduce portfolio losses through down or bear cycles and the establishment of price-sell or rebalancing targets to maintain portfolio allocations. Consider risk dilution as method to spread or combine different investments of various risk to minimize volatility.

Even the best financial professionals only consider half the equation.

Beware the lamb (risk management) in wolf’s clothing (risk dilution).

The goal of risk dilution is to “cover all bases.” It employs vehicles, usually mutual funds, to cover every asset class so business risk can be managed. The root of the process is to spread your dollars and risk widely across and within asset classes like stocks and bonds to reduce company-specific risk.

There’s a false sense of comfort in covering your bases. Diversification in its present form is not effective reduce the risk you care about as an individual investor – risk of loss.

Today, risk dilution has become a substitute for risk management, but it should be a compliment to it.

Risk dilution is a reduction of volatility or how a portfolio moves up or down in relation to the overall market.

Risk dilution works best during rising, or up markets as since most investments move together, especially stocks. Think about betting on every horse in a race.

- In other words, a rising tide, raises all boats.

Diversification can be stronger than it is right now. Unfortunately, the financial industry as a whole, has watered it down and widened it so much, it’s become absolutely ineffective as a safeguard against losses. One reason is the sales targets that forces financial representatives to spend less time with client portfolios.

Also, a financial big-box compliance department which is designed to protect the firm, not you as a client, will not allow anything but the washed-down outdated definition of diversification.

Think about it: A targeted diversification strategy places accountability on the advisor and poses risk to the firm. A wider approach makes it easier to vector responsibility to broad market ‘random walks’ so if a global crisis or bear market occurs and most assets move down together, an advisor and the compliance department, can “blame” everything outside their control.

- “Hey, it’s not our fault, it’s the market!”

Convenient excuse, isn’t it? After hearing this mantra repeatedly you’re going to get tired of it.

If positioned properly, bear markets should be perceived as future opportunity; a cycle that takes stocks from expensive to value. Currently, I have a long list of potential purchases. Overall, as a firm we maintain an overweight to cash and short-term bonds that will allow us to purchase equities at better prices.