What USD/CNY Through 7.00 Means For FX Markets

President Trump is accusing China of a ‘major violation’ by lowering the rate of the CNY. The Chinese deny they are using the yuan as a trade tool. Tuesday's PBOC fixing will help determine whether the People's Bank of China is letting the CNY float more freely – a move which will have broader implications for FX markets.

Leading members of the People's Bank of China, including Governor, Yi Gang (waving)

A move through 7.00 is a big deal

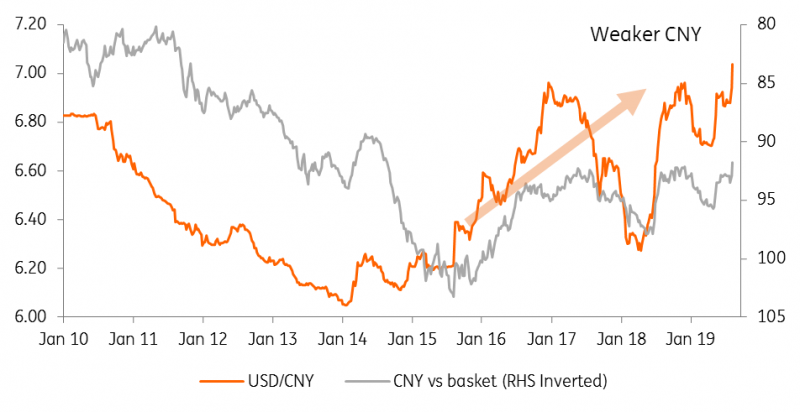

Having threatened to break it in late 2016 and again in late 2018, $/CNY has today moved cleanly through the 7.00 area. The move coincides with a significant fall in the CNY against its trading basket confirming that this is indeed a renminbi move and not just a strong dollar, weak EM story.

Rob Carnell covered this first for us today, arguing the higher $/CNY fixing looked to be a ‘deliberate decision’ from the PBOC and it begs the question whether a weaker renminbi should also be added to the list of possible retaliatory measures Iris Pang identified last week.

Over the next twenty-four hours, the focus will again be on the PBOC’s fixing. This is announced at 0315CET and the fixing will be assessed against model-based estimates and some whisper-numbers on where the fixing should come in. Unless the PBOC fixes USD/CNY below those model-based estimates, the market will again conclude that Chinese authorities have dropped their concern over a weaker Renminbi. Recall that concern prompted quite a few remedial measures from the PBOC last summer (tighter reserve requirements, fixing adjustments and closing loopholes for outflows).

Unless the PBOC tries to reverse today’s important break-out in USD/CNY, global investors will be left adding the risk of a CNY devaluation to their currently lengthening list of global concerns.

CNY weakens against both the dollar and the basket

(Click on image to enlarge)

Source: ING, Bloomberg

What are the implications for the rest of the FX market?

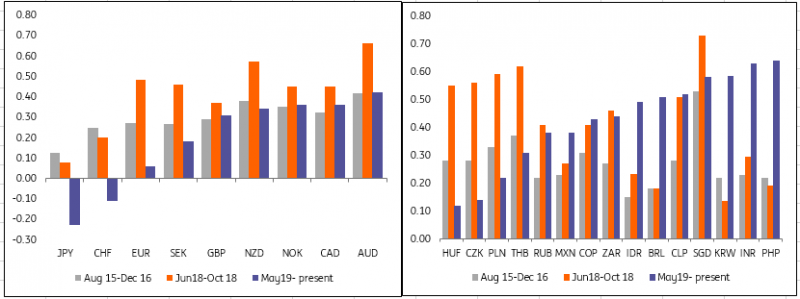

Investors have had plenty of experience with CNY weakness over the last four years – ever since the PBOC’s poorly managed fixing reform in August 2015. Below we look at FX correlations through broad periods of CNY weakness:

- August 2015 until late 2016 as CNY devaluation fears lingered,

- June-October 2018 as CNY reacted to the imposition of US tariffs and

- May 2019 until today, representing the breakdown of the trade truce.

Familiar patterns are seen across G10 and EMFX markets. The JPY is the clear out-performer, with little or inverse correlation to daily CNH moves. The commodity currencies – those currencies already under pressure on stagnation fears and flatter yield curves - are the under-performers.

In the EM space, Asian FX is showing increasing correlation to China’s FX moves – though the strong SGD link is pretty stable based on the CNY’s role in the SGD basket management. These trends should not be a surprise as Asia grapples not only with softer global trade and the China slow-down but also with the semi-conductor cycle and most recently deteriorating relations between Japan & S. Korea.

Typically CE3 is the least correlated – although they did suffer last year as CNY weakness coincided with poor growth figures out of the Eurozone. Unless EUR/USD breaks down to 1.05/1.08 – and we haven’t made that our base case yet, we think CE3 FX lags weakness in Asian FX and also the commodity centric Latin currencies.

An additional point to mention here is that President Trump’s comments about the USD/CNY move being a ‘major violation’ bring US unilateral currency intervention a little nearer. We’ve discussed the issue in detail here, but remind readers that if it did take place (probability still under 30%), it would likely see the US Treasury to instruct the Fed to buy EUR/USD and sell USD/JPY.

China dropped the price of their currency to an almost a historic low. It’s called “currency manipulation.” Are you listening Federal Reserve? This is a major violation which will greatly weaken China over time!

— Donald J. Trump (@realDonaldTrump) August 5, 2019

Correlation in daily changes between CNH and G10/EMFX currencies

(Click on image to enlarge)

Source: ING, Bloomberg

Indiscriminate deleveraging?

This extra layer of uncertainty has un-nerved global equity markets and accelerated the rotation from equity to debt markets. Were this equity correction to extend much further, even high-conviction trades in FX markets could be unwound on the back of indiscriminate deleveraging.

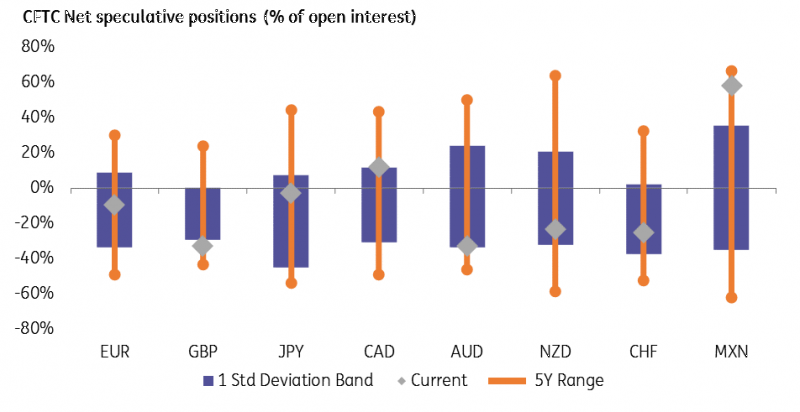

Looking at FX positioning through the lens of net speculative positions at the IMM shows the stand-out story is MXN. The 8% nominal, 4%+real rates have made the MXN a popular choice this year. We think MXN would look pretty vulnerable if equities sold off much further, with USD/MXN moving to 20.50 not out of the question.

FX net speculative positioning in Chicago futures markets

(Click on image to enlarge)

Source: ING, Bloomberg

CNY devaluation is added to the list of investor fears

The PBOC’s acceptance of USD/CNY above 7.00 has un-nerved investors further. Expect the safe-haven JPY and CHF to remain in demand and pro-cyclical currencies to stay under pressure. Only some surprise conciliatory wording on trade or the Fed surprising with more to offer in terms of easing can reverse this defensive risk environment.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more