Quantitative tightening has been humming broadly unnoticed in the background through 2023, but it will have an accelerated impact next year. While the level of rates will fall, the perception of liquidity will tighten. Bank reserves will fall in the second half of 2024, and QT will have wound down to prevent liquidity stress by year-end.

Image Source: Pixabay

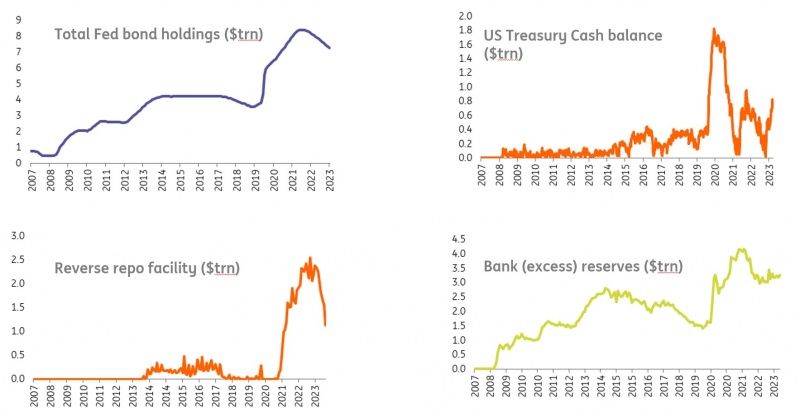

Reverse repo balances will hit zero in 2024, and then bank reserves meaningfully fall

There's no shortage of challenges on the horizon for the US rates market in 2024. Already the Treasury market has been struggling with liquidity, mostly with getting size done. This is typical when there's been an injection of impactful one-way direction. A gear switch from rate hiking to cutting typically generates jumpy price action, and this is set to be a source of volatility – which is exacerbated by a repo market that has seen better days in terms of size and liquidity. In bonds, tailed auctions, and especially in longer tenors, are another 2023 feature that could persist into 2024. Fiscal deficit-originated supply pressure is also impactful here, making the market a tad skittish, even as the pendulum switches to a rate-cutting bias next year.

The ongoing withdrawal of excess liquidity from the money market is also important to note. The genesis of this is ongoing quantitative tightening (QT) as the Federal Reserve continues to allow US$95bn per month to roll off the curve (and off their balance sheet). The most significant manifestation is to be seen in the fall in idle market cash going back to the Fed on the reverse repo facility. That peaked at around US$2.5tr and is now just below US$1tr, helped recently by a rebuild in Treasury cash balances.

The bottom line here is that these reverse repo balances will head to zero, signalling a virtual end to excess liquidity. As the US Treasury does not need to build additional cash buffers, the pace of fall in reverse repo balances should slow to something akin to the size of monthly quantitative easing – but even at that pace, it would mean the reverse repo balance hitting zero by the third quarter of 2024.

Bank reserves holding up as reverse repo balances take most of the QT pressure

(Click on image to enlarge)

Macrobond, Federal Reserve, US Treasury, ING estimates

By that time, the Fed is already set to be cutting rates. So, we envisage a period during which the central bank is easing policy through rate cuts and at the same time continuing to engage in QT. While the latter could be construed as being a contrary tightening in policy, the Fed will view it more as a return to more normal conditions in terms of the balance of liquidity in the system. Once the reverse repo balance hits zero, bank (excess) reserves will come under downward pressure. The big question, though, is how far the Fed will push this. Bank reserves are currently flatlining at around US$3.3tr, but have edged higher as of late.

Quantitative tightening likely ends around the end of 2024, long after the Fed has started to cut

The last time the Fed engaged in quantitative tightening, bank reserves bottomed at a little under US$1.5tr and there was a material effect felt on the money markets. It’s unlikely that we'll get anywhere near that this time around. Bank reserves will certainly get below US$3tr and likely down to US$2.5tr – but it’s unlikely that we'll get much lower, especially as the bias of policy is towards easing. The Fed will want to get liquidity into better balance as a first port of call, but beyond that, it won’t want to over-tighten liquidity conditions. Taking this into account, QT likely ends around the end of 2024.

The Fed could be a supplier of liquidity through the permanent repo facility by year-end

Consequently, one of the key features through 2024 will be a gradual and persistent tightening in liquidity conditions. This will become more apparent as bank reserves eventually start to ease lower. Less supply of liquidity typically goes hand in hand with a rise in the price of it, which is counterintuitive to the notion that market rates are falling. It acts to mute the extent of rate-cut euphoria which is likely to envelop markets through much of 2024.

This does not prevent market rates from falling, but it does make for more expensive funded longs at the margin. And it also reins in excessiveness that might come from a falling rates environment. It should result in higher market repo rates, well clear of the reverse repo rate offered by the Fed.

If pushed too far, it will require drawdowns from the Fed's permanent repo facility that supplies liquidity to the market. We think it'd be best for the Federal Reserve not to push on this.

More By This Author:

Hungary’s Labor Market Cools Slightly

The lure of rate cuts in 2024

FX Daily: Is Less Growth Pessimism Enough?

Comments

Log in or sign up to join the conversation.