USD/JPY Rally Halted And Everything Depends On The NFP Now

This was the week: Upbeat US GDP, Asian tensions, steady Fed, and trade

After a slow start within the known ranges, US GDP sent the greenback higher. The economy grew by 2.6% annualized in Q4 2018, better than had been expected. The report served as a relief to markets which had been worried that the US consumer was not keeping up.

The market calm gave another boost to USD/JPY as demand diminished for the safe-haven yen. Earlier, the haven yen saw demand due to the rising tensions between India and Pakistan. The South Asian nuclear nations clashed on the ground in Kashmir and the air. Pakistan’s announcement of the release of the captured Indian pilot helped calm tensions.

US President Donald Trump met North Korean Leader Kim Jong-un. The encounter failed as significant gaps separated both sides. The initial concern about the abrupt end to the talks was replaced by the news of ongoing negotiations.

Negotiations between the US and China have received contradicting reports. On the one hand, US Trade Representative Robert Lighthizer said that China’s increased buying of US goods is not enough to seal a deal and that structural changes are needed. On the other hand, White House Adviser Larry Kudlow said the talks are on the cusp of a “historic agreement.”

Fed Chair Jerome Powell gave lengthy testimonies on Capitol Hill. He reiterated the pledge to remain patient on interest rates and signaled an end to the balance sheet reduction program by the end of the year. He topped it off by another speech in which he said the US economy is “in a good place“.

The mix of upbeat US data but no rush to raise rates is the perfect mix for USD/JPY but dark clouds arrived late in the week. The ISM Manufacturing PMI fell to 54.2 points indicating a slowdown and serving as an adverse hint to the upcoming NFP.

In Japan, the early reports of inflation from the Tokyo region came out slightly above expectations with the CPI ex Fresh Food figure accelerating to 1.1% YoY. This is nonetheless a meager growth rate, and the Bank of Japan remains bearish.

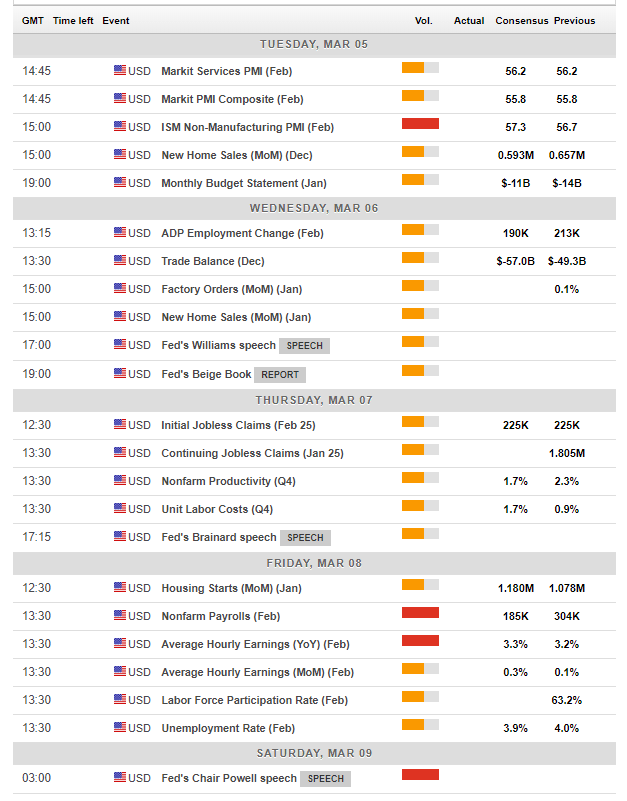

US events: NFP stands out

After the ISM Manufacturing PMI gave us the first hint towards the NFP, the complementary ISM Non-Manufacturing PMI follows with on Tuesday. The government shutdown caused a drop in January.

The belated release of New Home Sales for December will be watched. They jumped in November while other housing data have been quite weak and worrying of late.

The ADP Non-Farm Payrolls is the last hint towards Friday’s big event. The figures have been upbeat and well-correlated to the official BLS numbers of late. It is hard to see another 200K report for February, but anything is possible.

And finally, on Friday, the all-important Non-Farm Payrolls report could see some moderation after a superb increase of 304K jobs back in January. Back then, wage growth remained robust with 3.2% YoY. The Unemployment Rate will be of political interest, but markets will not worry as long as the Participation Rate increases as well. The labor market report will impact the Fed.

Apart from the data, trade talks between the US and China will be eyed. Any significant headline can move the pair. An announcement of a meeting between Trump and his Chinese counterpart Xi Jinping could boost sentiment and send USD/JPYhigher, while reports of major differences can weigh.

Here are the top US events as they appear on the forex calendar:

(Click on image to enlarge)

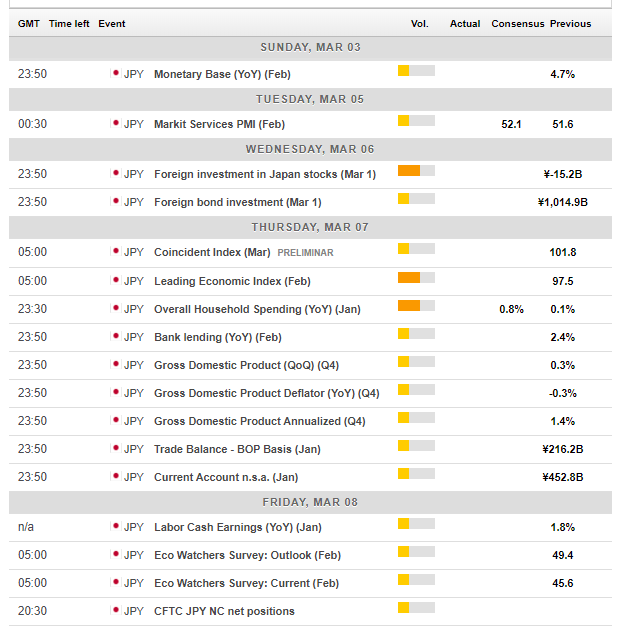

Japan: Keeping an eye open Asian tensions

Traders of the safe-haven yen will keep an open eye on developments in tensions between India and Pakistan. Things seemed to have calmed down at the time of writing but fresh flare-ups cannot be ruled out.

In addition, we may hear more from the US and North Korea on the failed summit. The versions differ and reports about ongoing low-level talks are needed to alleviate tensions. Trump insists he has a good relationship with Kim.

In Japan, the final GDP report and spending data are of interest in an otherwise not-too-busy calendar. The Japanese currency will move more with stocks than with data from the Land of the Rising Sun.

Here are the events lined up in Japan:

(Click on image to enlarge)

USD/JPY Technical Analysis

Dollar/yen trades in an uptrend channel which is better defined in its upper part. Uptrend resistance caps the pair since the early days of 2019 and has touched the price four times, making it quite significant.

Another bullish sign is rising Momentum and the ultimate signal is the fact that the pair crossed above the 200-day Simple Moving Average. At the time of writing, the Relative Strength Index (RSI) is still below 70, thus not pointing to overbought conditions.

The round number of 112 is an initial line of resistance. 112.25 was a double bottom in late 2018 and maybe a harder hurdle to cross. 112.55 worked as support in the autumn and 113.10 provided support to the pair on several occasions when it enjoyed higher ground late in 2018. 113.77 was a peak in December and 114 held USD/JPY down in November.

Support awaits at 111.30 which was an initial peak in February and it also coincides with the 200-day SMA .110.95 was a resistance line in mid-February and 110.25 provided support around the same time. 109.50 supported dollar/yen in early February and 108.50 was a low point in January.

(Click on image to enlarge)

-636870417978954011.png)

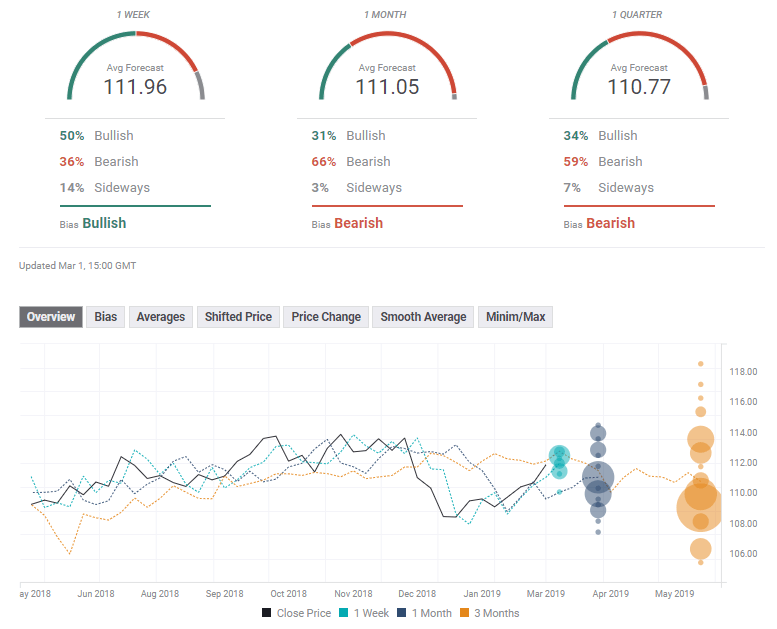

USD/JPY Sentiment

The pair finally broke out of range but have done so too far, too fast. We may see a correction now, especially as worries about global growth resurface. The NFP could also fall short of expectations.

The FXStreet forex poll of experts shows a bullish bias in the short term but a bearish one afterward, with lower targets as time progresses. The average forecasts have been upgraded for the short and medium terms but downgraded in the longer term.

(Click on image to enlarge)

Disclaimer: Foreign exchange (Forex) trading carries a high level of risk and may not be suitable for all investors. The risk grows as the leverage is higher. Investment objectives, risk appetite and ...

more