US Consumer Slowdown Fears Spread

Softer-than-expected US retail sales will reinforce the case for further stimulus. Coupled with weak inflation expectations and a deteriorating business backdrop we expect October, December and January rate cuts.

Evidence of the spreading US slowdown

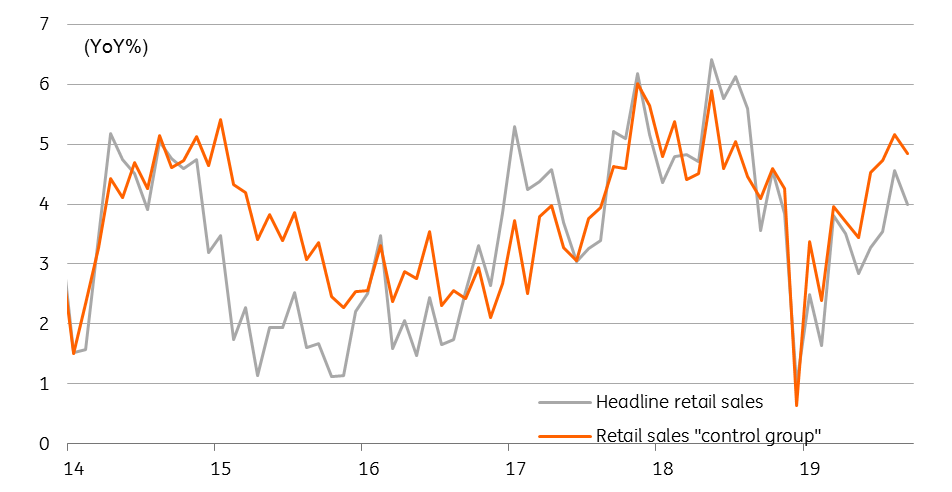

The disappointing run of US data has continued with today’s retail sales numbers for September, which posted the first decline for seven months. Rather than rise 0.3% month-on-month as expected, they actually contracted 0.3% with the report showing broad-based weakness. Just five of the 13 major categories within the report experienced an increase, namely furniture, health, clothing, miscellaneous and eating/drinking. Motor vehicles/parts fell 0.9%, gasoline stations sales fell 0.7%, building materials fell 1% and department store sales fell 1.4% (-7.3% year-on-year).

Stripping out the volatile components we find that the “control” group, which better reflects movements in the broader consumer spending component of GDP, was flat on the month versus expectations of a 0.3% MoM gain. With the rate of employment growth clearly slowing and the latest wage growth coming in much softer than expected, there are have been valid questions regarding how long consumer spending can continue to prop up the economy. Today’s report is not encouraging.

Retail sales growth has peaked

Source: Macrobond, ING

The case for further Fed rate cuts grows

With the major business surveys such as the ISM and National Federation of Independent Business reports seemingly in freefall and investment lead indicators pointing to contraction, we expect to see the economy to experience sub 2% growth in 4Q19. Add in weaker global growth, the strong dollar and a nagging doubt about the imminent prospects of a meaningful de-escalation of trade tensions and we see the economy expanding just 1.3% in 2020.

Given this growth backdrop and the fact recent inflation indicators show signs of softening and the University of Michigan consumer inflation expectations series hit an all-time low, the Federal Reserve will be increasingly nervous about hitting its inflation target. We expect the Federal Reserve to follow up the July and September rate cuts with a further 25bp move in October and another in December.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more