United Technologies Faces Reality- Will Other Companies Follow Suit Before It’s Too Late

On November 27, 2018, the CFO from United Technologies (UTX) stated that his company will focus on deleveraging and not stock buybacks. This announcement comes as General Electric (GE) is struggling mightily to retain investment grade status and its stock is nearing levels last seen during the depths of the financial crisis. While there is much to attribute to GE’s decline, massive stock buybacks in 2016 and 2017 are largely to blame.

To wit: “The root problem at GE — and why the stock is where it is — is poor capital allocation,” said RBC Capital Markets analyst Deane Dray.

Corporate debt now stands at record levels versus GDP as shown below. While the debt has been used to fund expansion and R&D it has also been used to fund record numbers of share buybacks. The pitfalls of such a strategy are now encroaching upon GE’s ability to survive. We suspect that UTX is the first of many companies to acknowledge this realization.

In February of 2016 we wrote an article on Conoco Phillips (COP). The missive, which is one of six articles we have written criticizing stock buybacks, describes how COP was forced to cut a reliable dividend and capital expenditures as they were strapped for cash. The price of oil at the time was hurting cash-flows. Unfortunately COP, like GE, had previously bought back a significant number of shares which greatly reduced their liquidity status when it was needed most.

While the article is nearly three years old we think it is every bit as important today as it was then. It exemplifies how precarious a company’s ability to survive financial weakness and/or an economic downturn is when capital is squandered in efforts to temporarily boost share prices. This story is likely to become a common theme for the next few years, especially if, as we suspect, economic growth declines and stocks prices fall.

As the Tide Goes Out, Effects of Buybacks are Exposed: The ConocoPhillips Poster Child

“The words of men may temporarily suspend but they do not alter the laws of financial dynamics. The fundamentals always take precedence eventually”- 720 Global 11/30/2015

The quote above was from an article we wrote that scrutinized stock buybacks and the unforeseen impacts they may have. In that piece as well as an earlier missive, “Corporate Buybacks; Connecting Dots to the F-word”, we rebuked the short-termism stock buyback fad. Both articles made the case that corporate executives, through buybacks, promote higher short-term stock prices that serve largely only to benefit their own compensation. The costs of these actions are felt later as the future growth for the respective companies, employees and entire economy are robbed.

This case study details how the “the laws of financial dynamics” have caught up with ConocoPhillips (COP) and demonstrates how shareholders are suffering while executives prosper.

COP

On February 4th, 2016 COP, in reaction to their fourth-quarter earnings release, slashed its quarterly dividend from $0.74 to $0.25 per share, a level not seen since March 2005. COP also lowered its current year capital expenditure (capex) budget by $1.31 billion, marking the second reduction in as many months. The actions are a direct response to the plummeting price of oil and the damage it is having on COP’s bottom line. The company’s net loss for the fourth quarter 2015 was $3.50 billion or $0.90 per share.

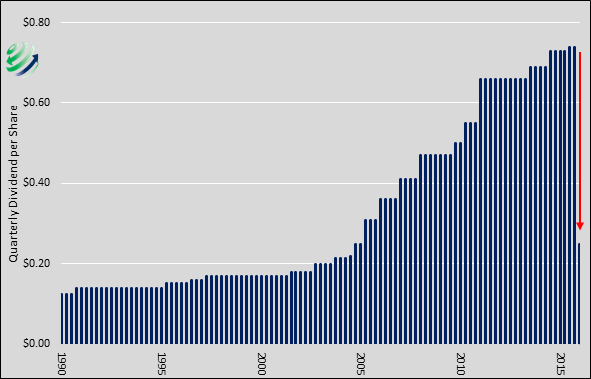

While the losses and expense cuts are not shocking given the severe decline in oil prices, the dividend cut was a jolt to many investors. COP has consistently paid a dividend, as shown below, since 1990. During that 25 year period, the dividend was increased 19 times but COP had never decreased it, until now. Even during the financial crisis of 2008/09, COP raised its dividend despite the price of crude oil dropping $100 per barrel.

Maybe the biggest cause for the shock is not the steadfastness of their prior dividend policy, but official corporate presentations. On the first page of their 2016 Operating Plan (Analyst & Investor Update – December 10, 2015) they make the following statements: “Dividend is highest priority use of cash” and “DIVIDEND Remains Top Priority”. The statements are repeated in the summary on the final page. The cover of their most recent annual report has a word cloud diagram with “dividend” shown among other key corporate values.

What Could Have Been

The dividend and capex reductions are prudent measures undertaken by management to help manage corporate assets and bolster their financial conditions during a historic swoon in revenue. This article does not question those actions, it instead asks if such drastic measures would be necessary had management not spent enormous sums of capital on stock buybacks in the preceding years.

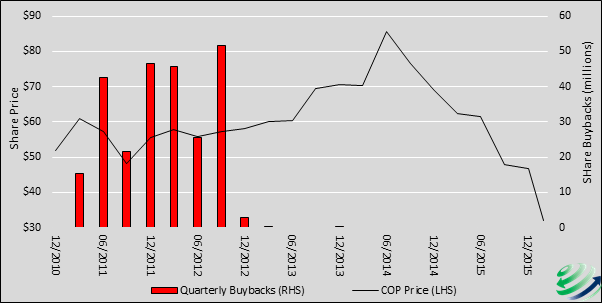

Since 2011, COP repurchased 251.316 million shares representing roughly 20% of their shares outstanding, at an approximate cost of $14.168 billion. The majority of these purchases occurred between 2011 and 2012 when the stock traded between $48 and $58 per share. Today the stock trades at $32 per share, matching prices last seen 12 years ago. The graph below charts the share price of COP with an overlay of the share repurchases by quarter.

Now let us contemplate what COP’s current financial situation might look like had management and the board of directors not engaged in repurchases. First of all, COP would still have the $14.168 billion spent on buybacks since 2011, which could be used to support the $0.74 per share dividend for almost 5 years. More importantly, the company could be in the envious position of employing the capital to buy assets that are being liquidated by other companies at cents on the dollar. Shareholders are suffering in many ways from the abuses of management in years past and will continue to do so for years to come.

The Rich Get Richer…

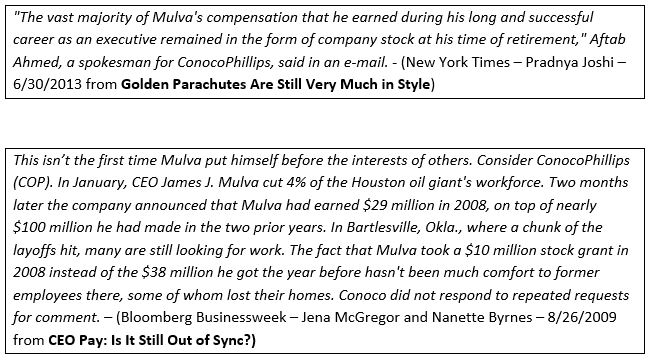

Fortunately for James Mulva, COP’s CEO during the 2011/2012 stock buyback era, his overly generous compensation is beyond COP’s ability to reclaim. Mr. Mulva retired in June of 2012 after repurchasing approximately 20% of the company’s outstanding shares. Upon retirement, he received a $260 million golden parachute from the company. That was on top of $141 million in total compensation he received in 2011.

The board of directors and shareholders must have been enamored with Mulva’s performance despite poor earnings trends in his final 2 years. From 2011 to 2012 the company earnings per share fell 25% from $8.97/share to $6.72/share. Had the board factored in the effect of buybacks on earnings per share when determining Mr. Mulva’s compensation, they would have realized that earnings per share were actually 40% lower at $5.37 per share.

We provide the following snippets on James Mulva to better gauge the potential motivations behind the tremendous buyback program.

Summary

While the financial media cheers buybacks and the SEC, the enabler of such abuse idly watches, we continue to harp on the topic. It is vital, not only for investors but the public at-large, to understand the tremendous harm already caused by buybacks and the potential for further harm down the road. Unfortunately, COP is not an isolated case. Hess Oil, for instance, just sold 25 million shares at $39 per share to improve their capital position. Sadly for Hess shareholders, many of whom likely supported buybacks, this shareholder dilution was unnecessary had Hess not bought nearly 63 million shares at a price of nearly $60 per share in the 3 years prior. Money that could have been spent spurring future growth for the benefit of investors was instead wasted only benefitting senior executives paid on the basis of fallacious earnings-per-share.

As stock prices fall, companies that performed un-economic buybacks are now finding themselves with financial losses on their hands, more debt on their balance sheets, and fewer opportunities to grow in the future. Equally disturbing, many CEO’s like James Mulva, who sanctioned buybacks, are much wealthier and unaccountable for their actions.

This article may be best summed up with the closing to our first article on buybacks.

Fraud – frôd/ noun:

wrongful or criminal deception intended to result in financial or personal gain.

Disclaimer: Click here to read the full disclaimer.