Treasury Market Flashing A Warning For US Economy

Recession risk remains low for US, based on the latest economic data overall, but the Treasury market is pricing in a higher probability that growth will slow and perhaps lead to a downturn at some point in 2019. It’s still unlikely that output will contract in the near term, although a combination of political and economic risk factors has unleashed a repricing of the macro outlook for the year ahead.

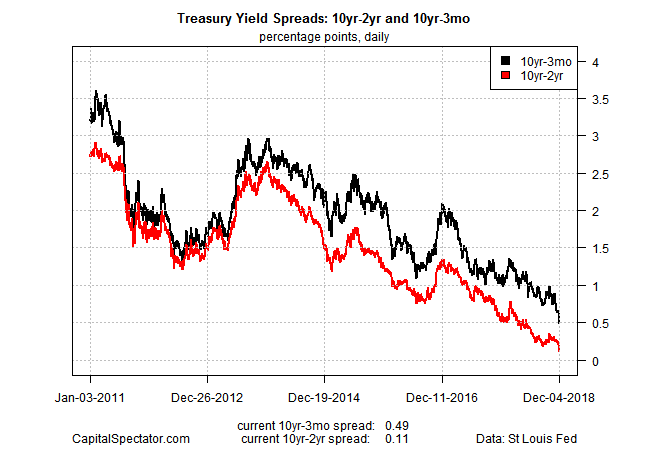

The widely followed 10-year less 2-year Treasury yield spread has fallen sharply in recent days, tumbling to 11 basis points on Tuesday (Dec. 4). Economists warn that a dip below zero for the spread – an inverted curve – would signal a high probability of a US recession within 12 months.

No one should dismiss this risk, yet some analysts point out that the spread for the 10-year and 3-month T-bill remains moderately higher at around 50 basis points. By some accounts, this spread is a more reliable measure of recession risk compared with the difference on the 10- and 2-year rates.

In any case, both spreads are still positive and so it’s premature to assume that a new recession is fate. Even if one or both of these spreads goes negative there’s still room for debate about the implications for the business cycle. Although inverted yield curves have been reliable predictors of recessions in decades past, there’s a school of thought that argues that it may be different this time. The reasoning is that the Federal Reserve’s extraordinary monetary policy over the past decade have distorted interest rates and so the historical record for this indicator may be less reliable these days.

Perhaps, but no one really knows the degree of relevancy (or irrelevancy) for the yield curve as a recession predictor. Surely it deserves a spot on the short list of business-cycle indicators, but relying on it in isolation could be problematic in the pursuit of a dependable and timely evaluation of recession risk.

A more reliable assessment of recession risk in real time requires looking at a broad set of metrics and monitoring a varied set of business-cycle indicators. By that standard, it’s highly unlikely that an NBER-defined recession has started, based on data published to date.

To be sure, it’s becoming increasingly clear that US growth peaked earlier this year and the economy remains on track to slow in the foreseeable future, as discussed in this week’s edition of The US Business Cycle Risk Report. But at this stage it’s not obvious that softer growth will soon deteriorate to the point that a new recession is fate.

Indeed, history reminds that the US economy’s speed can vary significantly in an expansionary period without slipping into contraction. Recall that many analysts were fooled in 2011 and 2012 (and again in late-2015 and early 2016) into believing that a new recession was destiny – forecasts that turned out to be wrong, largely due to flawed models and a misguided focus on a handful of indicators.

The solution is focusing on a diversified set of metrics for modeling recession risk. But that requires a fair amount of work, which inspires the search for shortcuts. At the top of the list is the Treasury yield curve, which holds out the promise of a quick and easy estimate of the state of the business cycle.

In reality, developing a robust profile of recession risk requires a deeper read. Whatever the merits of the yield curve as a recession indicator, one metric alone doesn’t rise to the level of a silver bullet for business-cycle analysis. In fact, no one data set passes that test.

A better approach is to monitor a wide set of numbers and on that basis recession risk remains low. The macro trend looks set to decelerate in the near term, but it’s not yet obvious that the downshift will deteriorate to the point that a new NBER-defined recession is near.

Sure, that analysis could change, depending on the incoming economic reports. But assuming the worst at this point is less about making informed decisions vs. assuming that a single data point will tell you everything you need to know about a $20 trillion economy.

Disclosure: None.