The Kiwi Catapulted After Hawkish RBNZ

The value of the Kiwi was adjusted aggressively to the upside as algo activity was lighting-fast to react to a hawkish policy statement by the RBNZ. Will this represent a macro inflection point in the Kiwi, and as a consequence, the onset of a bullish trend? Read the report to find out all the details and what's the latest status in the Forex arena...

Quick Take

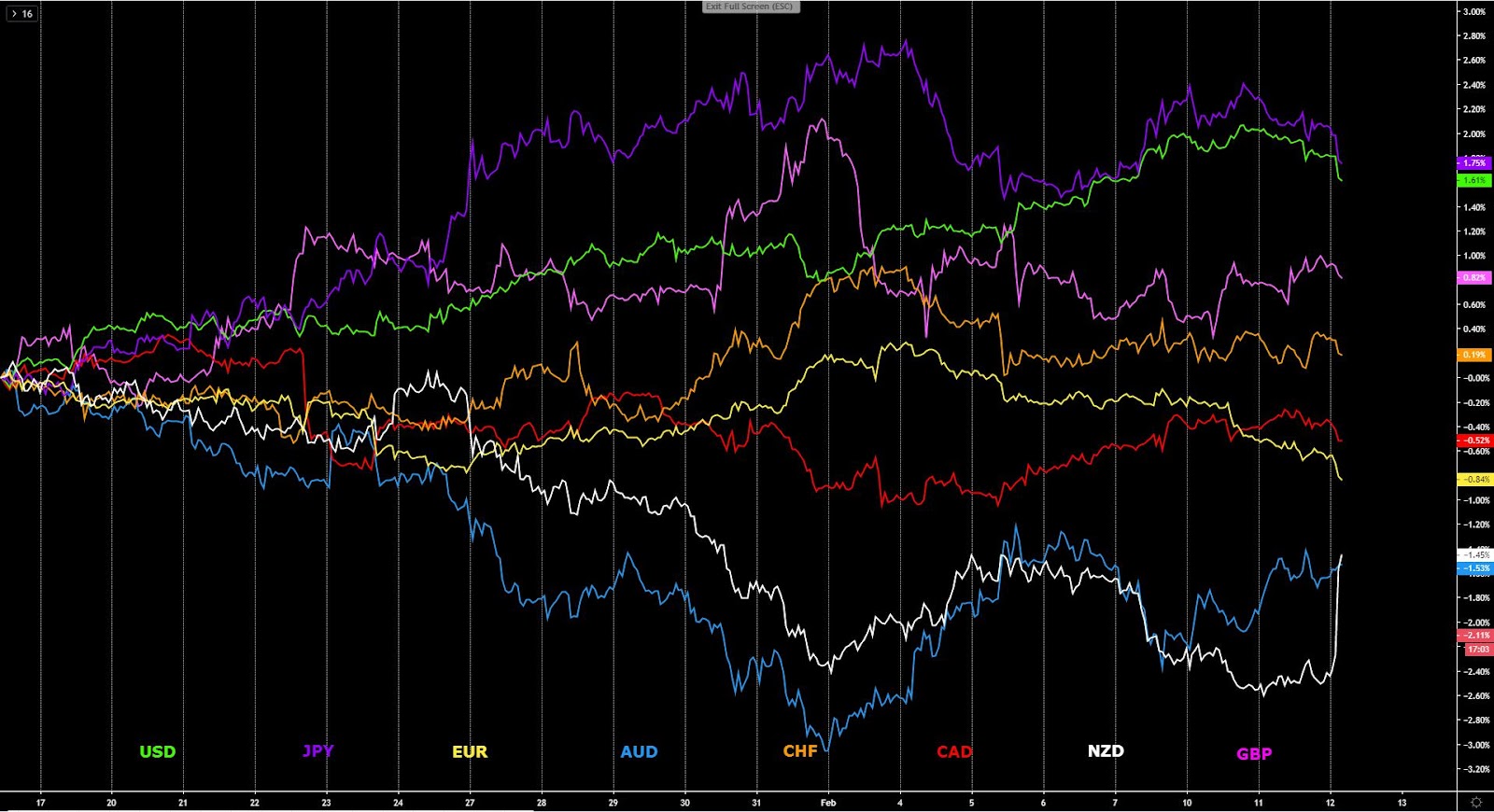

The economic calendar was packed with Central Bank events, including Fed’s Powell, ECB’s Lagarde and BOE’s Carney. The net effect, after all said and done, is a sense that these policymakers did a great job at sounding non-committal and sticking to the familiar mantra. What does this mean? It means there was little meat in the bone, a lack of substance or new surprises in the remarks they had prepared. As a consequence, the movement in currencies this week continues to be rather dull in nature, with the US Dollar a touch softer, even if that has not acted as a catalyst to see buying in the Euro, which remains in free-fall. Watch the EUR index closely as it nears a key level where long inventry building is a real possibility.

The Kiwi, however, is the exception, marked up aggressively by algo activity and the unwinding of shorts on the aftermath of a more hawkish-than-expected RBNZ. The Aussie, meanwhile, saw buy-side flows re-emerge but at a much slower pace as the positive groove in equities feeds through. The lower reported rate of new NCoV infections by China (even if numbers manipulated), or expectations of some factories in China to soon re-open are factors supporting equities. Not to forget, the Fed’s balance sheet expansion via money market operations, alongside the boost in Trump ratings to win this year’s presidential race after the Iowa caucus fiasco is also an aid.

This recovery in equities is causing the Yen and Swissy to see sell-side flows dominate this week, but the setback in the currencies is still under a bullish context when analyzing the aggregated daily flow. The Sterling is one of the clear beneficiaries from the current state of affairs, with its recovery more to do with a technically-inspired re-loading of longs at a critical liquidity area than any particular fundamental catalyst, as the EU-UK trade talks still the key driver with the outlook as tricky as it was during the aggressive sell-off in the Pound earlier this month. Lastly, the Canadian Dollar remains firmer but on the daily the currency remains structurally bearish.

(Click on image to enlarge)

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Institutional Bank Research reports.

The Kiwi flies on RBNZ hawkish surprise: The Kiwi appreciated sharply on the back of a rather hawkish RBNZ’s policy announcement. The RBNZ left the cash rate on hold as expected at 1% but once the market scanned through the details of the statement, the reasons to bid to NZD piled up. First of, he forecasts for the OCR show they do not expect to cut this year, with the next move projected a hike in mid-late 2021. The RBNZ assumes the overall impact of coronavirus will be of a short duration, expecting the economic growth to accelerate over the H2 2020. So, with the RBNZ unlikely to cut again as they appear confident to have re-calibrated the policy settings enough for the optimal conditions to see inflation pick up, there may be a significant re-adjustment in NZD short exposure. The market had expected an easing bias to be retained and certainly not the hawkish shift from the guidance. If the NCoV turns out to be near its peak, it’s safe to assume the RBNZ has signaled today the end of its easing bias.

‘Risk on’ back in vogue: Risk appetite continues charging ahead as the price behavior in the Aussie, the Yen, gold, equities or bond yields reflect. There have been a number of key factors discussed in the media to fit the current narrative in the recovery of asset valuations, from the expansion of the Fed’s balance sheet via the operations conducted to stabilize money markets, the exaggerated movements caused by the coronavirus as the rate of new infections reported by China decreases, leading some factories in China to re-open, or the greater odds of Trump claiming victory in this year’s presidential race after the Iowa caucus fiasco.

Fed’s Powell retains the old too familiar mantra: As part of the testimony by Fed Powell on the semiannual Monetary Policy Report to the Congress before the Committee on Financial Services, none of the opening prepared remarks by the policy-makers caused much movement in the market as Powell repeated the familiar lines that is going to take a considerable shock for the Fed to veer off its current neutral course. In the words of Powell, “the policy is likely appropriate barring material reassessment.

Key passage from the prepared statement by Powell: The most important passage that markets scanned as part of Powell’s current view in policy included: “The FOMC believes that the current stance of monetary policy will support continued economic growth, a strong labor market, and inflation returning to the Committee’s symmetric 2 percent objective. As long as incoming information about the economy remains broadly consistent with this outlook, the current stance of monetary policy will likely remain appropriate. Of course, policy is not on a preset course. If developments emerge that cause a material reassessment of our outlook, we would respond”.

Trump’s criticism towards Powell won't stop: The US President tweeted “when Jerome Powell started his testimony today, the Dow was up 125, & heading higher. As he spoke it drifted steadily downward, as usual, and is now at -15. Germany & other countries get paid to borrow money. We are more prime, but Fed Rate is too high, Dollar tough on exports.”

Lagarde says monetary tools not the only game in town: In the introductory statement by Christine Lagarde, President of the ECB, on the presentation of the ECB Annual Report at the European Parliament, she said that monetary policy can't be only game in town, warning that the side effects of policy become greater with time. In terms of euro area growth, Lagarde noted that “momentum has been slowing since the start of 2018, largely on account of global uncertainties in weaker international trade.” As per inflation, Lagarde finds that the sluggish growth has led to “weaken the pressure on prices and inflation remains some distance below the medium-term aim.”

ECB set to rush review of inflation goal: According to an article by Bloomberg, the currently underway ECB comprehensive strategic review could be rushed to set an inflation goal by July. As part of the review, there are eight areas of focus to potentially revise, including inflation goal, measures of inflation, policy instruments, macro modeling, (de)globalization, digitalization, communication, climate change. An unnamed source noted that the governing council members will start addressing the specific issues immediately before the policy meetings in March and April. The strategic review represents a chance to heal the fragmented views by policymakers that built up under Draghi.

BOE Carney reassures stance on rates to remain low: As part of a testimony in front of the Economics Affair Committee in the UK, BOE Governor Carney said that “some stimulus may be required to get back to trend growth.” He also added that “interest is set to remain relatively low for the foreseeable future, with any upward adjustments expected to be modest.” Carney went on saying that “low interest rate environment adds to govt fiscal capacity.” Also, akin to the ECB, Carney said that “the BOE in the process of reviewing its monetary policy framework: It is possible, not saying there will, that there will be structural changes to how inflation targets are set, the bar being quite high.”

NCoV still at a critical phase: China Global Times quoted a Chinese senior medical advisor Zhong Nanshan as saying that the Coronavirus outbreak is still at very difficult moment. It read: “Wuhan epicenter of coronavirus outbreak is still at a very difficult moment, although a lower death rate compared to SARS and MERs, the city has not completely solve the problem with people to people transmission.”

UK growth in Q4 null, will it pick up in Q1 2020? The UK Q4 preliminary QoQ GDP came unchanged at 0.0% vs 0.0% expected, confirming that the UK economy got stuck in a phase of no growth during Q4 last year. Services and construction contributed positively to growth in the output approach to GDP in Quarter 4 2019, while production output contributed negatively to growth. What the market cares about though, is whether or not the economy can sustain to breathe a breeze of fresher air via a prolonged positive post-election sentiment. Such prospect must be reconciled with a very challenging road ahead to negotiate trade conditions between the UK and Europe.

Mixed-bag US data, Jolts a red flag: In terms of US data, we saw a solid NFIB small Business Optimism Survey, which came at 104.3 from 102.7, with strong market gains the main contributor. On the flip side, a major slump was seen in job-openings (JOLTS 6,423k in December from a downward revised 6,787 in November). It’s worth noting that based on Fed chair Janet Yellen’s favorite measure of labour market condition, this was her favourite data to monitor. What this suggests, according to the Research team at NAB, “is significantly slower monthly payroll gains down the not too distant track.”

Recent Economic Indicators & Events Ahead

(Click on image to enlarge)

(Click on image to enlarge)

Source: Forexfactory

Insights Into FX Index Charts

The risk dynamics keep re-anchoring to a more benign stance, led by the new highs printed in US equities, while the US 30-year bond yields also sees a mild tick up. This price action in the two ultimate instruments to understand the risk mood has resulted in a better tone in the likes of the Aussie, while the Yen gets sold. When looking at the USD/CNH, the fall in the pair (strength in the Yuan) for a second straight day can be interpreted as another positive sign. While the market structure of the risk-weighted index is not yet bullish off the daily, we are nearing a potential breakout through the previous high, in which case, it will further solidify the sense that risk appetite may see a more prolonged recovery in weeks ahead.

(Click on image to enlarge)

The EUR index keeps selling off and is fast approaching a key level of support. The question now is, will the index validate a fresh bearish cycle or could we see a rebound off the lows? If the latter ends up playing out, the currency is nearing some very attractive levels to play longs, even if one must be aware that it would be against the dominant bearish tide, hence some type of intraday confirmation on one’s entry will be a must-needed approach. If the index evolves into a new bearish cycle by finding acceptance below the previous low, sell on rallies is the way to go. For now, based on the lack of aggregated tick volume activity on the way down, I have serious reservations that we are headed into a new bearish cycle on the daily, which means a potential bottom may be looming near, even if as I said, you can’t just buy blindly.

(Click on image to enlarge)

The GBP index keeps finding support at a critical line of support that has so far disallowed a bearish breakout which would have damaged the outlook considerably. Instead, the index keeps recovering and is keeping the prospects of higher levels alive with dip buyers emerging. Technically, there is still value to buy the GBP under the context of a market that does not look overly pricey and has the structure not negating further upside. The smart money tracker has also turned back to bullish. I remain cautiously optimistic on the GBP outlook.

(Click on image to enlarge)

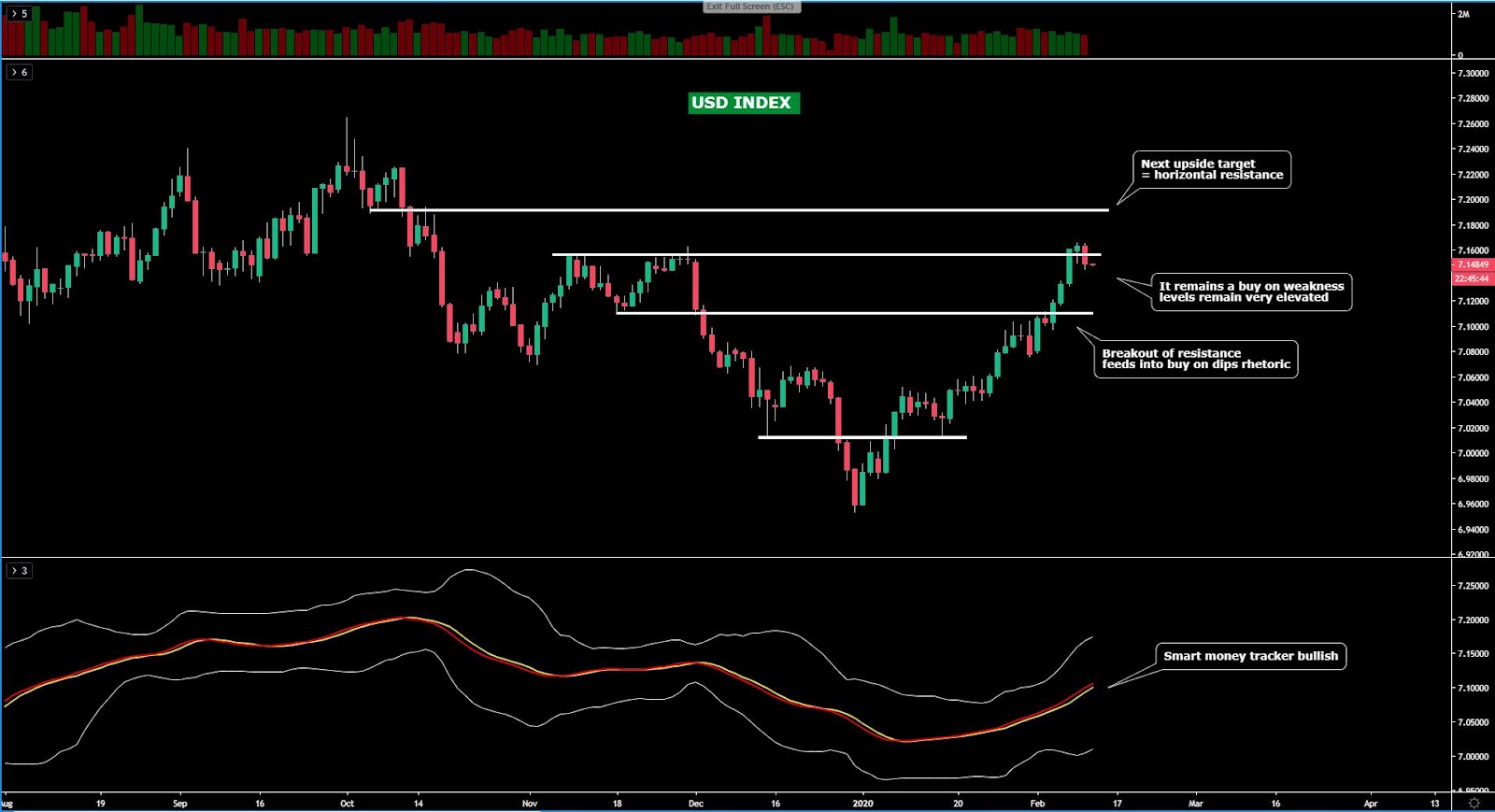

The USD index trades at rather lofty levels to perceive much value in being a buyer unless engaging in intraday scalping opportunities aimed at quick profits. I’d be very wary of entering longs as this is not a location where big institutions are looking to get the best pricing. In fact, we are at an area, judging by the aggregated flows, that the risk of profit taking at these liquidity area(double top from Nov breached) increases significantly, leading to pullbacks. The tapering of aggregated tick volume on the way up also suggests that this last part of the rally does not carry the substance necessary (for now) to make its prospects be long-lasting. This early warning does not negate the fact that the bullish trend is very well established, therefore I wouldn’t be surprised in the slightest if the USD keeps seeing buying pressure on shallow dips.

(Click on image to enlarge)

The CAD index faces the risk of selling off from these pristine levels in line with the daily bearish structure and this is a view so far backed up by the tick volume taper seen. On the flip side, the prolonged retracement has led to a softening of the bearish momentum as indicated by the smart money tracker turning bullish now, which debilitates the case for the selling to be in congruence with my favorite measure of momentum in a market, which is when the slope still points lower. Nonetheless, my main case of risks skewed towards the downside is still valid as the smart money tracker may still re-anchor bearish if selling ensues from these levels. The case to be a CAD seller, from a fundamental standpoint, has debilitated a tad following the positive surprise in the Canadian jobs, which reduced the odds of a BOC rate cut.

(Click on image to enlarge)

The JPY index, on the back of closing the up-gap from two weeks ago, continues to suggests that further bullish price action in line with the underlying price structure is a real possibility. The upward slope in the money tracker is also endorsing longs at this stage, hence why I wouldn’t be surprised in the slightest if buy-side pressure increases for an eventual retest of the previous highs, even if the risk conditions at this stage are not supportive with US equity indexes at all time highs. I remain firm in my core case that adding Yen short exposure at these levels is frankly quite risky as the daily pattern at play remains a powerful one for at least the recent trend high. The readership can find out more about this pattern in this video I created.

(Click on image to enlarge)

The AUD index is putting up a fight to challenge the sell-side pressure off a key resistance. However, based on the aggregated tick volume, the retest into this resistance for a second time is far from compelling as the buy-side volume activity is reducing. The price action from Tuesday still changes nothing the outlook as all the prerequisites to be a seller on weakness are still in place, that is, a price structure of lower lows and lower highs, a resistance tested and rejected, alongside the smart money tracker heading lower. Longs the AUD remains a risky bet, a view that would be negated on a break and hold above the mentioned resistance.

(Click on image to enlarge)

The NZD index is breaking to the upside at the time of writing as the RBNZ surprised the market with a hawkish policy statement, essentially preparing the market for an end of its easing bias, barring a major deterioration in the NCoV situation. This markup has the momentum behind to see further gains short-term, but be aware that is always much safer, in order not to be caught at suboptimal price entries, to wait for a retracement before engaging in longs. This is a move, stimulated by a Central Bank decision, that sets the stage for an inflection point that may see the onset of a long-lasting trend in the Kiwi even if it’s still early days.

(Click on image to enlarge)

The CHF index, the more candle that get printed this week, the more that it reaffirms my bullish stance that an eventual retest of the previous high is within reach. The build up of buy-side pressure from the current levels is predicated on the bullsh market structure, the price action formations, with back to back long long shadows in this week’s candles, alongside a bullish smart money tracker. Therefore, dip buying is still the main case.

(Click on image to enlarge)

Important Footnotes

Market structure: Markets evolve in cycles followed by a period of distribution and/or accumulation. To understand the principles applied in the assessment of cycles, refer to the tutorial How To Read Market Structures In Forex

Horizontal Support/Resistance: Unlike levels of dynamic support or resistance or more subjective measurements such as Fibonacci retracements, pivot points, trendlines, or other forms of reactive areas, the horizontal lines of support and resistance are universal concepts used by the majority of market participants. It, therefore, makes the areas the most widely followed and relevant to monitor. The Ultimate Guide To Identify Areas Of High Interest In Any Market

Fundamentals: It’s important to highlight that the daily market outlook provided in this report is subject to the impact of the fundamental news. Any unexpected news may cause the price to behave erratically in the short term.

Projection Targets: The usefulness of the 100% projection resides in the symmetry and harmonic relationships of market cycles. By drawing a 100% projection, you can anticipate the area in the chart where some type of pause and potential reversals in price is likely to occur, due to 1. The side in control of the cycle takes profits 2. Counter-trend positions are added by contrarian players 3. These are price points where limit orders are set by market-makers. You can find out more by reading the tutorial on The Magical 100% Fibonacci Projection

The Daily Edge is authored by Ivan Delgado, Head of Market Research at Global Prime. The purpose of this content is to provide an assessment of the market conditions. The report takes an in-depth ...

more