The Buyback Blackout Period Myth. Don't Be Fooled.

Earlier this year, Deutsche bank released a chart, a proposal if you will. Why is it a proposal, I'll get to that in a moment. One of the things we aim to do at Finom Group (for who I am employed), as an exercise in rooting out facts, is to debunk myths in order to value information and data that inundates us as investors and/or traders. One such myth we were forced to debunk this year lands on the principle practice of share repurchase programs. So let's get to it!

Buybacks

The following commentary was issued in Finom Group's weekly Research Report on March 24, 2019 titled "Yield Curve Inverts, Taking Equity Markets Down: What Next?" (Subscription required). The report aimed to outline the truisms and falsehoods surrounding share repurchase programs, otherwise known as buybacks. With the political temperature running hot for the subject matter, we aimed to focus on the mechanics.

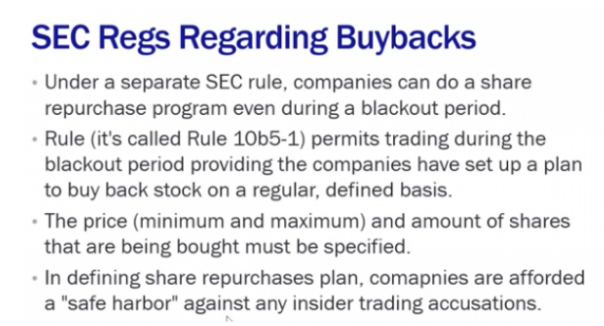

"Earnings season is fast approaching and as such, the notion of how buyback blackout periods will affect the overall market has reared its ugly head. We characterize it this way largely because of the lack of liquidity in the market place since late 2018. For an understanding of the SEC rules that govern share repurchases by corporates and executives, understand that the rules were created to remove liability from corporations while adding a layer of public disclosure for public market participants."

- Rule 10B-18 reduces liability for companies and their affiliated purchasers when the company or affiliates repurchase the company’s shares of common stock.

- In 2003, the SEC amended the rule, requiring companies to disclose more detailed information on share repurchases on forms 10-Q, 10-K and 20-F.

- Despite the safe harbor provision, the company must report repurchases in compliance with the various regulations.

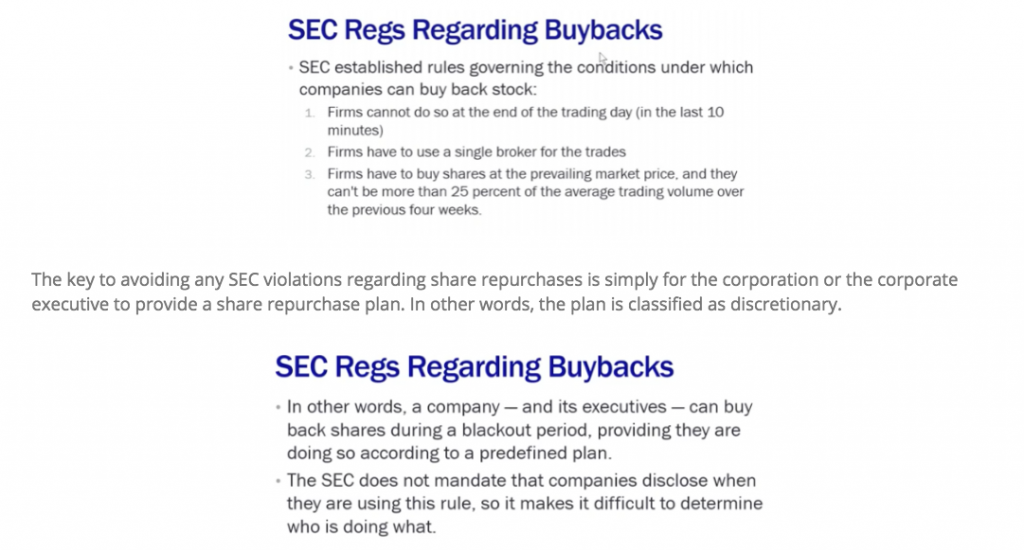

"Market participants have largely been under the impression and found with the understanding that there is an SEC regulated blackout period for corporations. The reality is that there are only 3 real rules offered by the SEC. We suggest the term “offered” because the SEC rarely has ever levied a case against any buyback program. Here are the 3 rules governing buybacks."

"So here comes the funny part or the disturbing part of the SEC rules concerning blackout periods and/or share repurchase programs. In the bullet points below, one can see that the SEC does not mandate that companies disclose when they are using rule 10b5-1. Can you believe that? It’s basically saying, “Here’s some rules we want you to follow, but because we have no real way to track, regulate and levy penalties we’re forced to institute an Honor System."

"The fact is that most people have limited to no understanding about the rules regarding buybacks. Why is this you might ask? It’s largely due to herd mentality. Nobody wants to be accused of insider trading and corporations simply move the liability of executing share buyback programs onto broker dealers. Because the SEC has only raised a couple of concerns since 1983 on the subject matter, everyone simply assumes the rules are hard and fast instead of considering there is quite literally every existing loophole in the SEC rules that basically make it possible for share buybacks to happen at any time and without the threat of penalty."

Okay so there you have the rules, the whys and hows for executing buybacks during a so-called blackout period. Naturally, based on everything offered, the term blackout period is nothing more than that, a term, a myth a colloquialism that has endured for lack of due diligence or desire to perform such exercises for efficacy of the notion. As highlighted by the SEC guidelines/rules above, the SEC basically has no recourse for share repurchases committed during these so-called blackout periods, by way of their own offered guidelines/rules/acquiescence. The SEC basically makes it improbable to violate or acquire bad behavior for the sake of share repurchase programs. And why did I decide to embark upon this exercise in March, as earnings season was unfolding?

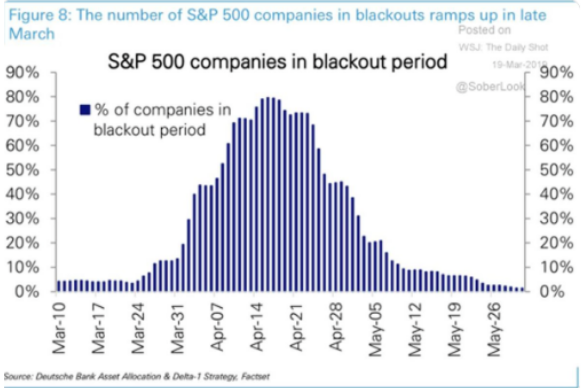

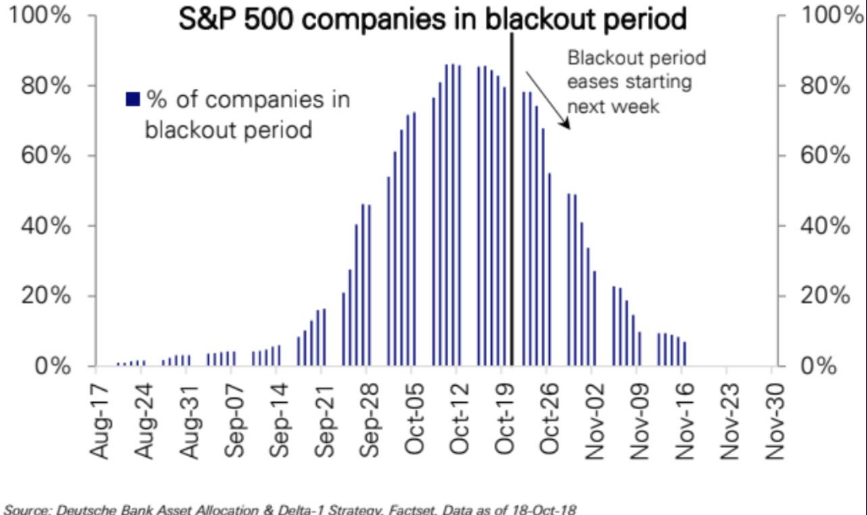

The following chart, proposal if you will, was offered during this time period. The chart proposal suggests there's a peak period for the mythological blackout period.

When I/Finom Group first saw this chart we noticed, primarily, that it's not a YoY chart, it's not even a QoQ chart that would lend to backtesting or some sort of precedence for validation purposes. Without such historic depictions, we understand this to not be a technical chart, but a proposal. Deutsche Bank is literally saying, "We believe and assert this to be the scenario, our truth!"

The chart comes from Deutsche Bank… of course it’s Deutsche bank, because they have a stellar reputation? And of course it was first published in a ZeroHedge article. Because Zerohedge's reputation for truth telling and unbiased narratives... well you get the picture!

The DB chart offered has no basis of reality on how corporate buyback plans work or the fact that the notion of a blackout period is only a notion of sentiment and has no reference to any SEC rule.

Moreover, we have seen reports that quarter-end rebalance effects will be made worse by the buyback ‘blackout’ period that starts ~1 month before earnings season, i.e., end of March. This is simply not the case either, as individual companies enter blackout periods not ahead of the beginning of the earnings season, but ahead of their own reporting date. But this is also just a myth, sentiment based and tradition. So if there even was a peak blackout period it would be in mid- to late April, rather than late March. According to J.P. Morgan Chase’s Marko Kolanovic:

“Keep in mind that blackout periods only affect discretionary buyback programs. We estimate that ~60% of buyback programs are not affected by the blackout. While a blackout period is not positive for equities, its impact should not dominate the price action of the market. Given the near-record amount of buyback activity, we estimate that blackout periods this year may result in as much activity as during peak periods of past years.”

In keeping with Kolanovic’s factual representations, we are also forced to recognize that the herd has spoken, and for years. There is a natural period of share buybacks that do ease during earnings season, but it’s not a rules based activity, just tradition and for which periodically the PBs brokerage desk data validates periods of increased buybacks during the so-called blackout period. I'll get to that in a moment.

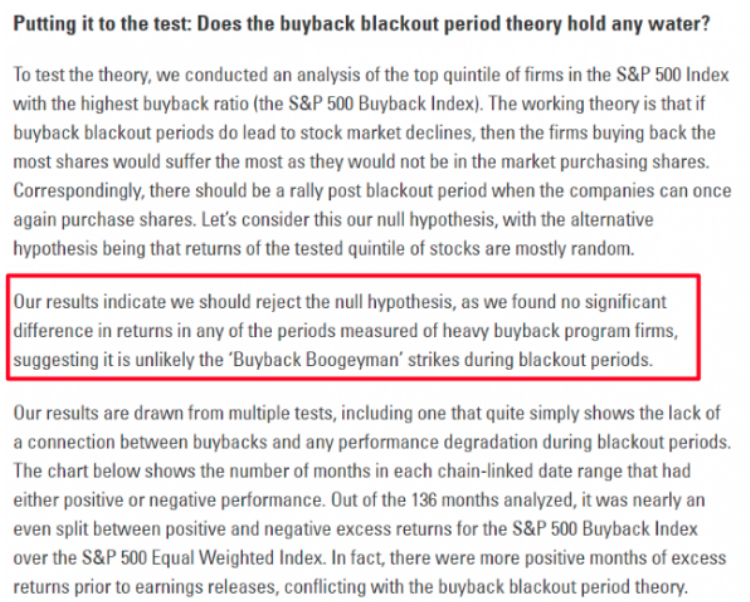

Usually, I don't have to engage a chart proposal this way, but unfortunately the DB blackout period chart became so popular that it was the top search-related item for the key words "buyback and blackout", once it was published back in March 2019. Pushing forward with this myth-busting activity, I discovered the following study on blackout periods from Wes Gray of AlphaArchitect.com. He performed a study on the effect of blackout periods on the market just last year. His findings were that they have almost no impact on the market. It's hard to impact the market with something that doesn't exist. Just logic, just logic. (See below)

With all the information already outlined above, this should be enough to understand that there really is no such thing as a blackout period other than that which is self-imposed by the corporation in question. As long as the company desires to disclose buybacks outside of the existing plan, the company can literally repurchase shares the day before it's ER release. And as noted above, the SEC doesn't even require this or have a mechanism in place for tracking outside of an Honor System.

I wouldn't even bother going beyond the already outlined due diligence exercise if it weren't for the desire to evidence the non-issue of blackout periods, but why not do so. Why not demonstrate what one of the biggest buyback Prime Brokerage (PB) desks had to offer in the way of buybacks for this period in question, the earnings season underway at that time. Keep in mind, the following insights came from my follow-up article, at the end of Q1 earnings season, from whence the peak of the blackout period was being disseminated by Bank of America Merrill Lynch's PB desk. It was offered in the article titled "A Binary Outcome From Trade Talks Looms".

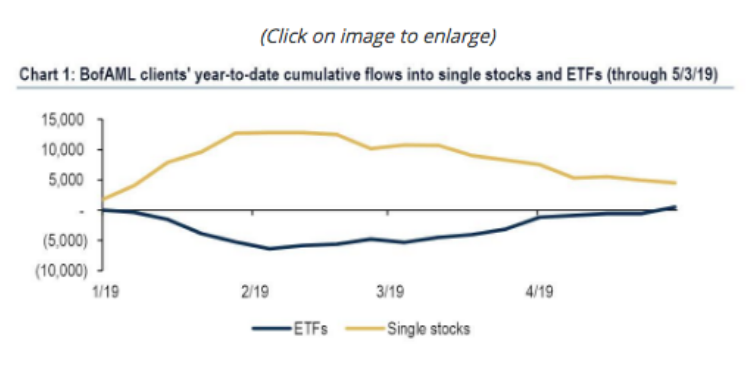

"Bank of America’s strategist Jill Carey Hall outlines that last week, during which the S&P 500 was up +0.2%, just about everyone was selling stocks, as “Institutional clients, hedge funds and private clients sold the highs in equities last week.” And yet, somehow the S&P hit a new all-time high. How? The answer: “Corporate buybacks ramped up.”

"As BofAML discusses further, “buying was led by corporate buybacks, as all other groups (hedge funds, institutional and retail clients) were net sellers of equities for the 2nd week in a row as trade skirmishes flare up."

- Clients were net sellers of single stocks (2nd straight week) but continued to buy ETFs (8th straight week). Cumulative flows into ETFs YTD turned positive, reversing outflows seen earlier this year (Chart 1).

- Buybacks last week were their highest since early Feb: they tend to be strong during earnings seasons and seasonally peak in mid/late May. Buybacks YTD are +20% YoY, though the growth rate continues to decline.

Everything offered by the BofML PB desk negates the proposed chart from Deutsche Bank, not that we needed the added information, as logic dictates. So why are we here again, talking buyback blackout periods? Well, Deutsche Bank is at it again with another one of their infamous maladies.

Their latest proposal found my attention over the weekend, as it surfaced on Twitter (TWTR). The same Twitter #fintwit participant who tweeted the former DB chart proposal on buybacks, tweeted the latter. Just saying, we don't know what we don't know and hopefully this revisited and/or updated exercise has served to add value to your knowledge base with regards to buybacks and the mechanics at play during earnings season.