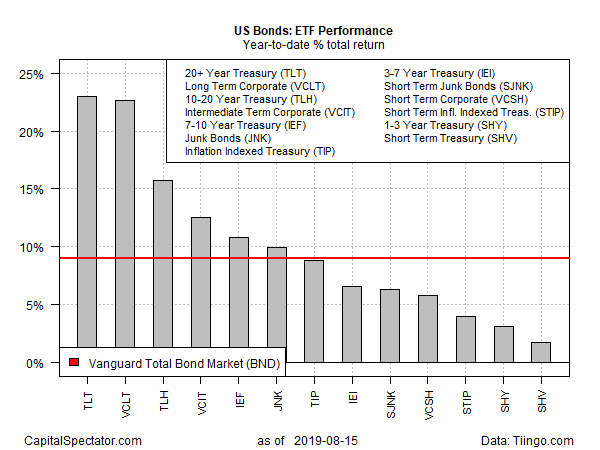

Mounting recession worries of late have taken a bite out of stocks, but heightened fears that an economic contraction may be near has lit a fire of buying for US bonds. Long bonds, in particular, have soared recently, delivering stellar results, as shown by a set of exchange-traded funds representing the major slices of the US fixed income market.

Two funds on our list stand out for year to performance: iShares 20+ Year Treasury Bond (TLT) and Vanguard Long-Term Corporate Bond (VCLT). These pairs are neck and neck in 2019 through yesterday’s close (Aug. 15). TLT is up a sizzling 23.0%, trailed ever so slightly by VCLT’s 22.6% rally.

The rest of the field is doing quite well also, although the results look tame these days compared with going long. The third-best year-to-date return is found in iShares 10-20 Year Treasury Bond (TLH), which is up 15.7% this year. That’s a solid return by historical standards, but it’s no match for the longer maturities.

The source of the bond market’s striking gains: elevated recession fears. Right or wrong, the crowd has piled into Treasuries and investment-grade credits on the assumption that the US economy is caught in downward spiral. Although the economic data have yet to issue a clear warning, investors are betting that the numbers will soon align with the bond market’s implied forecast.

“The bond market is screaming recession,” says Andrew Brenner, head of international fixed income National Alliance. “Just take a look at what the US market is doing.”

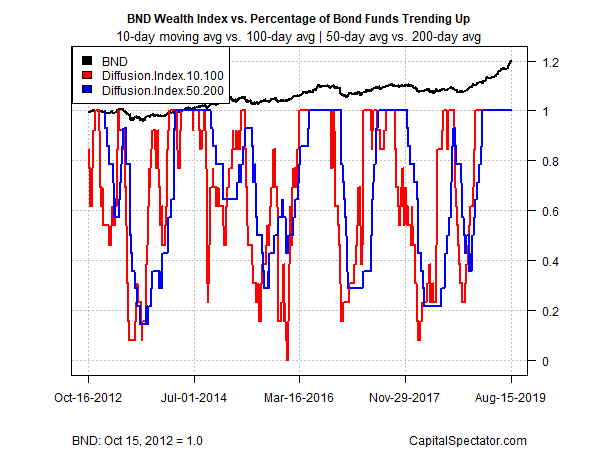

A picture’s worth a thousand words, as they say, and on that point a chart of TLT’s rally of late speaks volumes.

Suffice to say, the fixed-income crew is all-in on expecting that the US economy will begin contracting soon, courtesy of the implied forecast via inverted yield curves.

Reasons for adopting a modicum of caution, however, include yesterday’s retail sales report, which revealed that consumers ramped up spending by 0.7%, a four-month high. Retail numbers are just one slice of the economic profile, of course, and hard data tends to lag the forward-looking estimates of the markets. But for Bernard Baumohl, chief global economist at The Economic Outlook Group, the latest sign of strength on Main Street is telling.

“The key determinant that will shape the path of the economy this time won’t be the yield curve or the direction of the fed-funds rate,” he wrote in a note to clients.“It’s the extent to which American consumers will offset the damage done by policies that impede world trade and reverse globalization. All eyes should therefore be laser focused on what households are thinking and doing in the coming months— and not on some tampered yield curve.”

The crowd begs to differ. After all, yield curves have an impressive history of anticipating recession through the decades. But skeptics are quick to point out that this time could be different, in part because US yields are (still) high relative to what’s available elsewhere. The German 10-year yield is roughly -0.70%, for example, vs. 1.52% for a 10-year Treasury at the moment. The gap in favor of US bonds is compelling for foreign investors, even after factoring in forex risk. As a result, rising offshore demand to grab a higher yield is a factor in driving up bond prices and pushing long yields below short rates. In other words, inverted yield curves in the US may be less about the outlook for the US economy vs. a reflection of the desperate search for positive yield in Europe and elsewhere.

Keep in mind, too, that quite a lot of the pessimism these days is bound up with the US-China trade war. The question is whether President Trump senses that his battle is hurting the US economy, which in turn threatens his re-election prospects? Will that convince Trump to wind down the conflict, declare victory, and move on? If so, a sentiment boost would surely arrive, perhaps triggering a sell-off in bonds.

In any case, if the US economy continues to plod along, which suggests that there may be a reckoning for certain corners of the bond market that appear to be betting the farm on macro calamity.

“Bond yields signal recession risk, we say not so fast,” advises Mark Haefele, chief investment officer at UBS Wealth Management. “If Fed rate cuts successfully steepen the curve comfortably into positive territory, this brief curve inversion may be a premature recession signal.”

For now, though, Haefele and others in his camp are in the minority. Judging by pricing in the bond market, the future has miraculously become clear. Indeed, profiling momentum in the fixed-income market continues to reflect confidence in the extreme on what’s coming. The profile is based on two measures of the price trend for the funds listed above. The first metric compares each ETF’s 10-day moving average with the 100-day average — short-term trending behavior (red line in chart below). A second set of moving averages (50 and 200 days) offers an intermediate measure of the trend (blue line). The indexes range from 0 (all funds trending down) to 1.0 (all funds trending up). Based on prices through yesterday’s close shows that all the bond ETFs cited are in a strong bullish posture. As such, the only thing that bond investors fear: upbeat economic reports in the days and weeks ahead.

Comments

Log in or sign up to join the conversation.