The 3-Big Lies About Tax Cuts & The Economic Impact

“The greatest trick the Devil ever pulled was convincing the world he didn’t exist.” – The Usual Suspects (1995)

Just recently, Politico ran a story by Brain Faler entitled: “Big Businesses Paying Even Less Than Expected Under GOP Law.” To wit:

“The U.S. Treasury saw a 31 percent drop in corporate tax revenues last year, almost twice the decline official budget forecasters had predicted. Receipts were projected to rebound sharply this year, but so far they’ve only continued to fall, down by almost 9 percent or $11 billion.

Though business profits remain healthy and the economy is strong, total corporate taxes are at the lowest levels seen in more than 50 years. Analysts agree they can’t yet explain the decline in corporate tax payments.“

Uhm, excuse me?

This is where I get to say, “I Told You So!”

The Big Lie #1

While the Devil may have convinced the world he doesn’t exist, it was that “corporate cronyism” devoured Washington politics.

“Our companies won’t be leaving our country any longer because our tax burden is so high.” – Donald Trump

That was an outright lie.

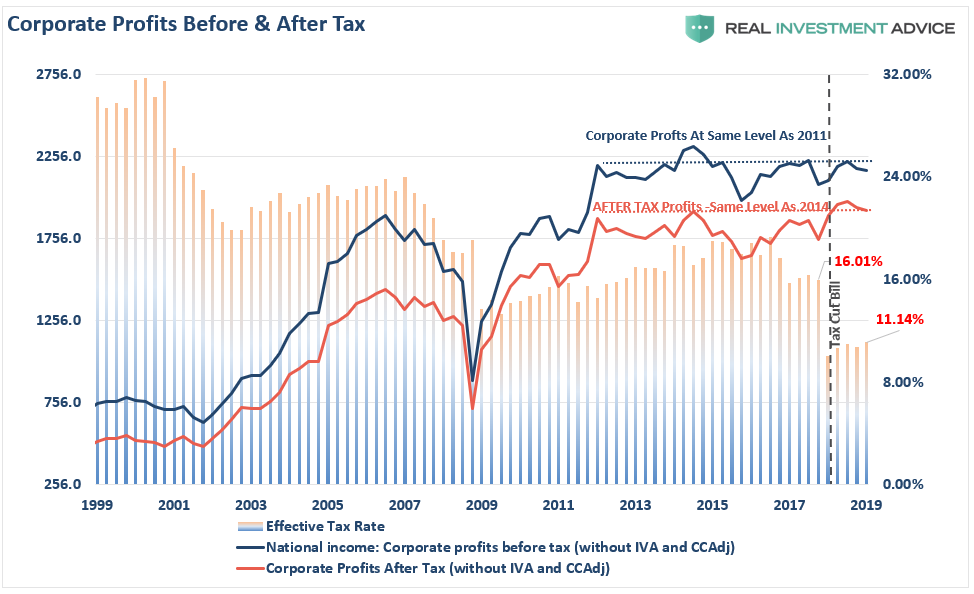

First of all, there is a massive difference between “statutory,” the stated tax rate, and the “effective” tax rate, or what companies actually pay. The chart below shows corporate profits before and after-tax with a measure of what the effective tax rate was.

Just prior to the passage of the tax cut bill, the effective tax rate for U.S. companies was about 16%, or less than half of the statutory rate of 35%. After the passage of the legislation, the effective tax rate fell to 11%, again less than half of the statutory rate of 21%.

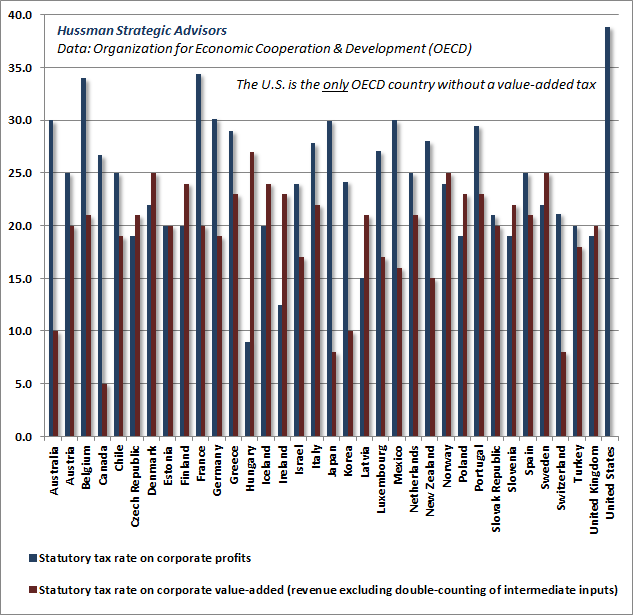

There is also the matter that every other country in the world has a “value-added tax,” or VAT, added to their corporate tax rate. Dr. John Hussman did a good piece of analysis on this.

“I’ll add that another feature of Wall Street’s blissful delusion is the notion that ‘U.S. corporate taxes are the highest in the world.’ It’s striking how disingenuous this claim is. The fact is that among all OECD countries, the U.S. is also the only country that does not levy any tax at all on corporate value-added in the production of goods and services.”

“The main point is this. The argument that U.S. taxes on corporate profits are somehow oppressive relative to other countries is an apples-to-oranges comparison. It wholly ignores that the U.S. levies no value-added tax on corporations at all, whereas the value-added tax is the principal revenue source for most other countries. The rhetoric on corporate taxes here is unfiltered effluvium.

It is a myth that the U.S. has the highest corporate tax rate in the world. We simply didn’t, and don’t.

The Big Lie #2:

The second big lie was:

““It’ll be fantastic for the middle-income people and for jobs, most of all … I think we could go to 4%, 5% or even 6% [GDP growth], ultimately. We are back. We are really going to start to rock.” – Donald Trump

So, what happened?

Nearly seven months PRIOR to the passage of the legislation, I discussed that engaging in tax cuts at the end of an economic cycle would nullify the majority of the expected effect.

“Tax rates CAN make a difference in the short run, particularly when coming out of recession as it frees up capital for productive investment at a time when recovering economic growth and pent-up demand require it.”

The reason that tax receipts have fallen since the passage of tax reform is that top-line revenue growth has slowed along with both domestic and global economies. However, we already knew this was going to be an issue as we discussed in that 2017 article noted above. To wit:

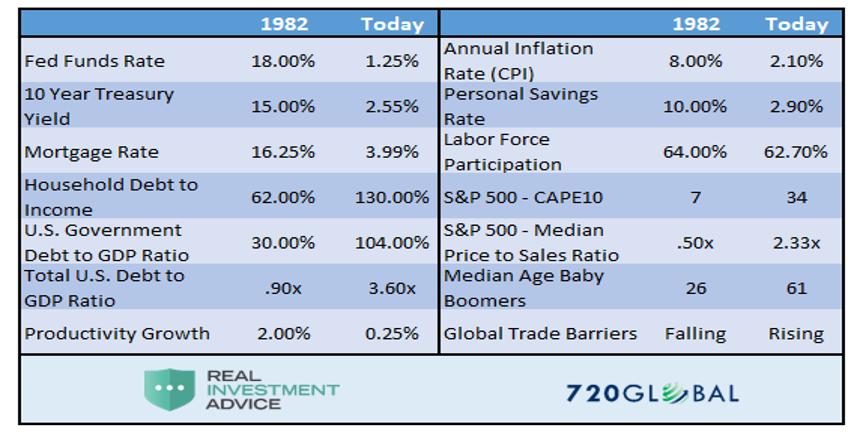

Importantly, as has been stated, the proposed tax cut by President-elect Trump will be the largest since Ronald Reagan. However, in order to make valid assumptions on the potential impact of the tax cut on the economy, earnings and the markets, we need to review the differences between the Reagan and Trump eras. My colleague, Michael Lebowitz, recently penned the following on this exact issue.

‘Many investors are suddenly comparing Trump’s economic policy proposals to those of Ronald Reagan. For those that deem that bullish, we remind you that the economic environment and potential growth of 1982 was vastly different than it is today. Consider the following table:’”

The differences between today’s economic and market environment could not be starker. The tailwinds provided by initial deregulation, consumer leveraging, declining interest rates, and inflation provided huge tailwinds for corporate profitability growth.

Just for clarity, tax rates CAN make a difference coming out of recession. However, given the economy was already growing near maximum capacity in 2018, the boost from tax cuts was mostly mitigated.

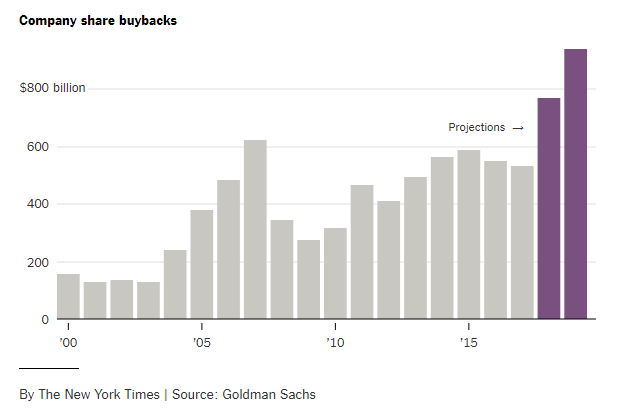

Secondly, corporations, which is where the tax cuts were primarily focused, used the tax cuts not to increase productivity, make investments, or grow revenues. Such investment most likely would have resulted in greater economic growth and higher tax revenue, however, the windfall was mainly used to manipulate stock prices through massive share buybacks.

“A recent report from Axios noted that for 2019, IT companies are again on pace to spend the most on stock buybacks this year, as the total looks set to pass 2018’s $1.085 trillion record total.”

“The reality is that stock buybacks create an illusion of profitability. Such activities do not spur economic growth or generate real wealth for shareholders, but it does provide the basis for with which to keep Wall Street satisfied and stock option compensated executives happy.”

The Big Lie #3:

The third big lie was that tax cuts would pay for themselves.

“Not only will this tax plan pay for itself, but it will pay down debt.” – Treasury Secretary Steven Mnuchin

That didn’t happen.

In fact, the debt and deficit got materially worse as I predicted they would in “3 Myths About Tax Cuts:”

“During the previous Administration, the GOP wielded ‘fiscal conservatism’ as a badge of honor. Since the election, they have completely abandoned those principals in a full-blown effort to achieve tax reform.

We are told, by these same Republican Congressman and Senators who passed a fiscally irresponsible 2018 budget of more than $4.1 trillion, that tax cuts will ‘pay for themselves’ over the next decade as higher rates of economic growth will lead to more tax collections.

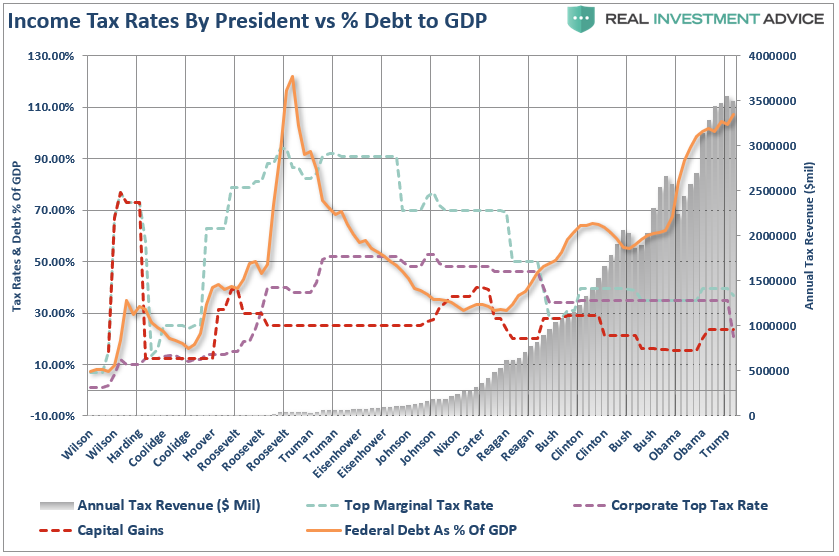

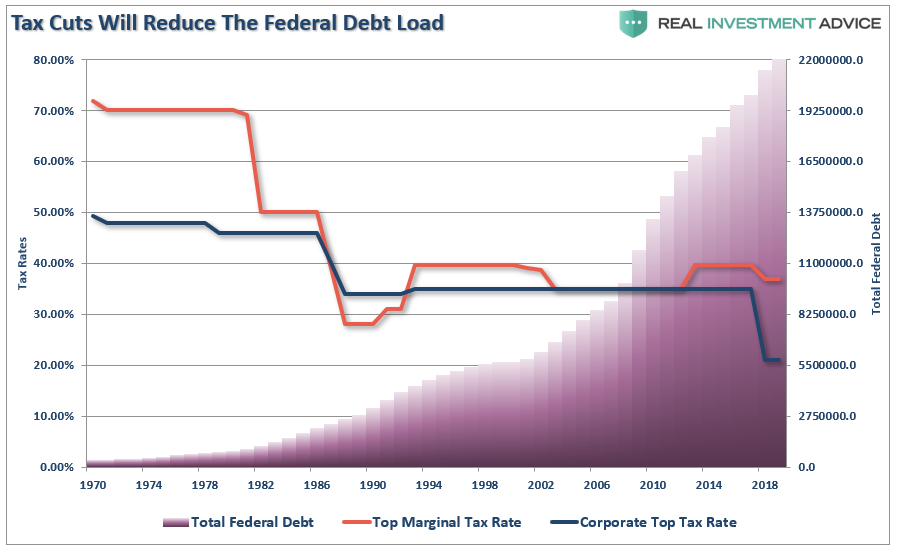

Again, we see that over the “long-term” this is simply not the case. The deficit has continued to grow during every administration since Ronald Reagan. Furthermore, the widening deficit has led to a massive surge in Federal debt which is currently in excess of $22 trillion, and growing much faster than economic activity, or the nations ability to pay it off.

This was the exact point made in “Tax Cuts & The Failure To Change The Economic Balance:”

“As noted in a 2014 study by William Gale and Andrew Samwick:

The argument that income tax cuts raise growth is repeated so often that it is sometimes taken as gospel. However, theory, evidence, and simulation studies tell a different and more complicated story. Tax cuts offer the potential to raise economic growth by improving incentives to work, save, and invest. But they also create income effects that reduce the need to engage in productive economic activity, and they may subsidize old capital, which provides windfall gains to asset holders that undermine incentives for new activity.

In addition, tax cuts as a stand-alone policy (that is, not accompanied by spending cuts) will typically raise the federal budget deficit. The increase in the deficit will reduce national saving — and with it, the capital stock owned by Americans and future national income — and raise interest rates, which will negatively affect investment. The net effect of the tax cuts on growth is thus theoretically uncertain and depends on both the structure of the tax cut itself and the timing and structure of its financing.”

Since the tax cut plan was poorly designed, to begin with, it did not flow into productive investments to boost economic growth. As we now know, it flowed almost entirely into share buybacks to boost executive compensation. This has had very little impact on domestic growth. The ‘sugar high’ of economic growth seen in the first two quarters of 2018 has been from a massive surge in deficit spending and the rush by companies to stockpile goods ahead of tariffs. These activities simply pull forward “future”consumption and have a very limited impact but leaves a void which must be filled in the future.

Nearly a full year after the passage of tax cuts, we face a nearly $1 Trillion deficit, a near-record trade deficit, and empty promises of surging economic activity.

It is all just as we predicted.“

Recessionary Warning

While well-designed tax reforms can certainly provide for better economic growth, those tax cuts must also be combined with responsible spending in Washington. That has yet to be the case as policy-makers continue to opt for “continuing resolutions” that grow expenditures by 8% per year rather than doing the hard work of passing a budget.

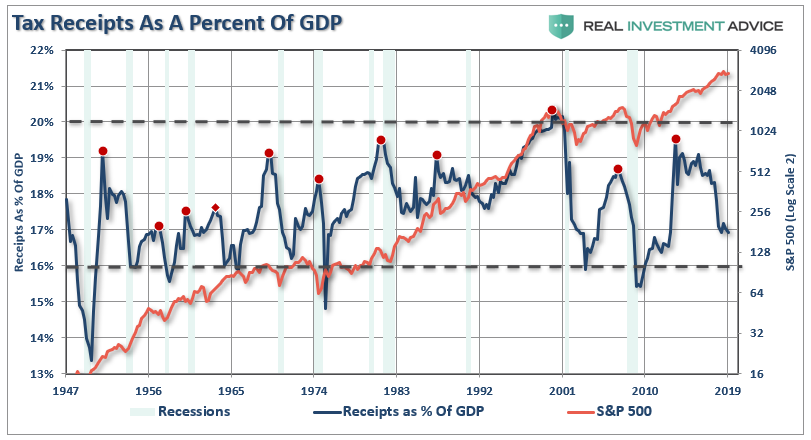

Given that tax receipts fall as the economy slows, tax receipts as a percentage of GDP is a pretty good indicator of recessionary onset.

The true burden on taxpayers is government spending because the debt requires future interest payments out of future taxes. As debt levels, and subsequently, deficits, increase, economic growth is burdened by the diversion of revenue from productive investments into debt service.

As expected, lowering corporate tax rates certainly helped businesses increase their bottom line earnings, however, it did not “trickle down” to middle-class America. As noted by Jesse Colombo:

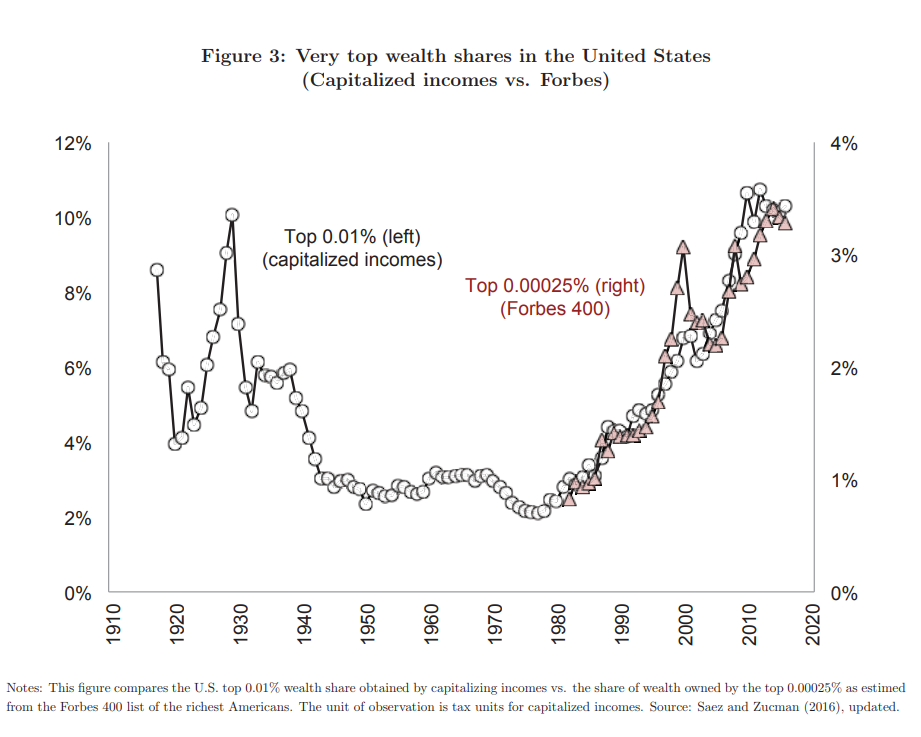

“‘In 1929 — before Wall Street’s crash unleashed the Great Depression — the top 0.1% richest adults’ share of total household wealth was close to 25%, today, the that same group controls more wealth than the bottom 50% of the economy combined.”

Not surprisingly, focusing tax cuts on corporations, rather than individuals, only exacerbated the divide between the top 1% and the rest of the country as the reforms did not focus on the economic challenges facing us.

- Demographics

- Structural employment shifts

- Technological innovations

- Globalization

- Financialization

- Global debt

These challenges will continue to weigh on economic growth, wages and standards of living into the foreseeable future. As a result, incremental tax and policy changes will have a more muted effect on the economy as well.

As investors, we must understand the difference between a “narrative-driven” advance and one driven by strengthening fundamentals.

The first is short-term and leads to bad outcomes. The other isn’t, and doesn’t.