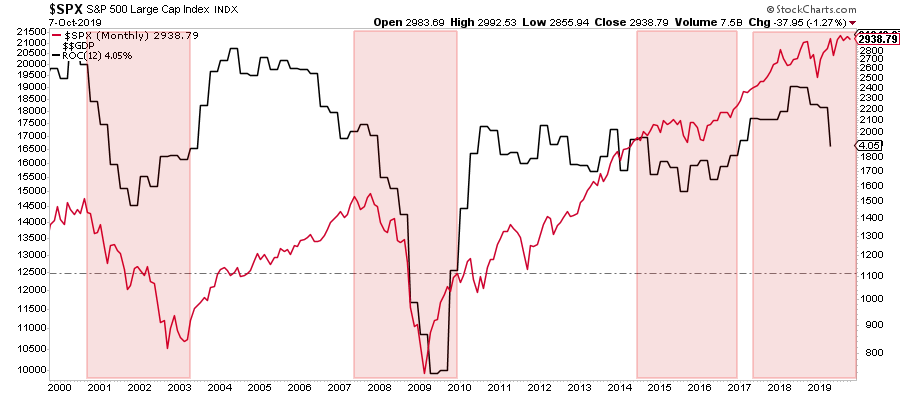

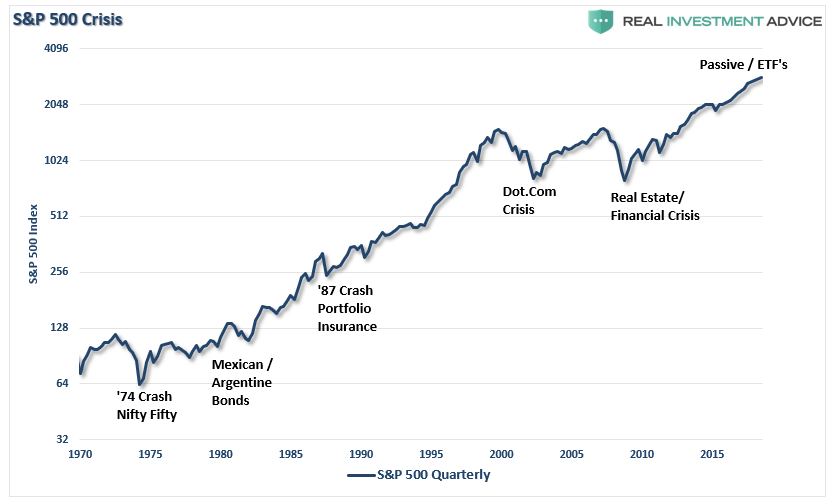

Technically Speaking: This Is Nuts & The Reason To Focus On Risk

Since the lows of last December, the markets have climbed ignoring weakening economic growth, deteriorating earnings, weak revenue growth, and historically high valuations on “hopes” that more “Fed rate cuts” and “QE” will keep this current bull market, and economy, alive…indefinitely.

This is at least what much of the media suggests as noted recently by Rex Nutting via MarketWatch:

“‘Recessions are always hard to predict,’ says Lou Crandall, chief economist for Wrightson ICAP, who’s been watching the Fed and the economy for three decades. But after looking deeply into the economic data, he concludes that ‘there’s no reason’ for the economy to topple into recession. The usual suspects are missing. For instance, there’s no inventory overhang, nor is monetary policy too tight.”

Since the financial markets tend to lead the economy, he certainly seems to be correct.

(Click on image to enlarge)

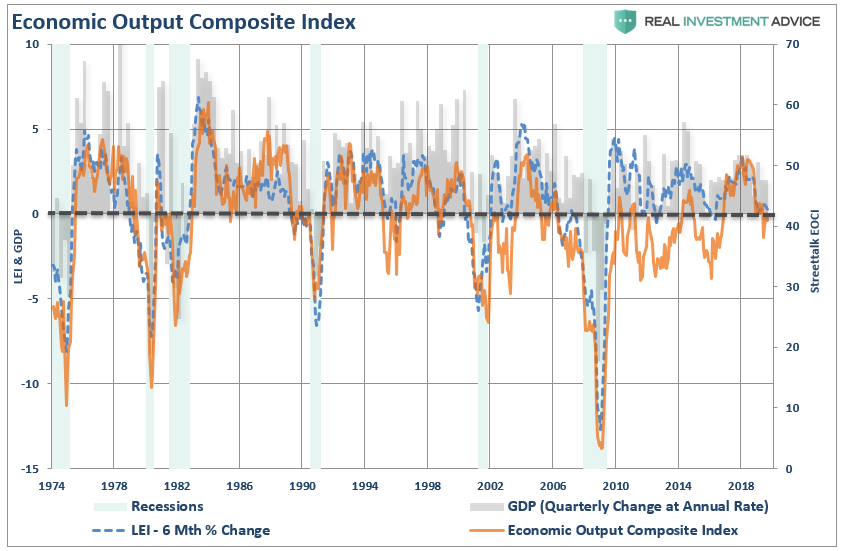

However, a look at the economic data indeed suggests that something has gone wrong in the economy in recent months. The latest Leading Economic Index (LEI) report showed continued weakness along with a myriad of economic data points. The chart below is the RIA Economic Composite Index (a comprehensive composite of service and manufacturing data) as compared to the LEI.

(Click on image to enlarge)

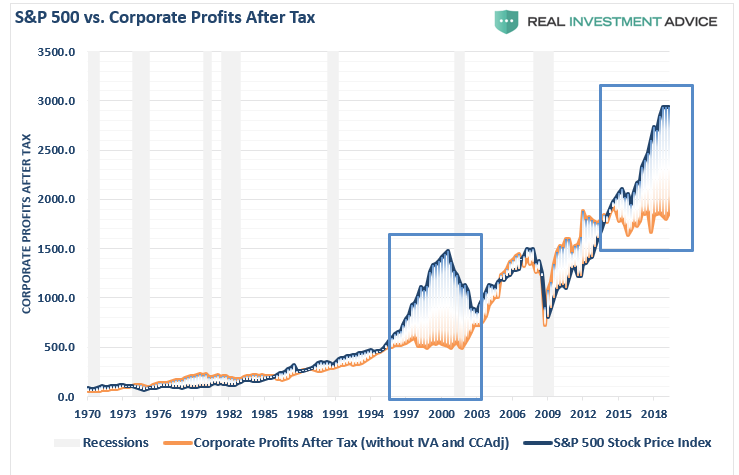

The downturn in the economy shouldn’t be surprising given the current length of the overall expansion. However, the decline in the LEI also is coincident with weaker rates of profit growth.

(Click on image to enlarge)

This also should be no surprise given the companies that make up the stock market are dependent on consumers to spend money from which they derive their revenue. If the economy is slowing down, revenue and corporate profit growth will decline also.

However, it is this point which the “bulls” should be paying attention to. Many are dismissing currently high valuations under the guise of “low interest rates,” however, the one thing you should not dismiss, and cannot make an excuse for, is the massive deviation between the markets and corporate profits after tax. The only other time in history the difference was this great was in 1999.

(Click on image to enlarge)

This is nuts!

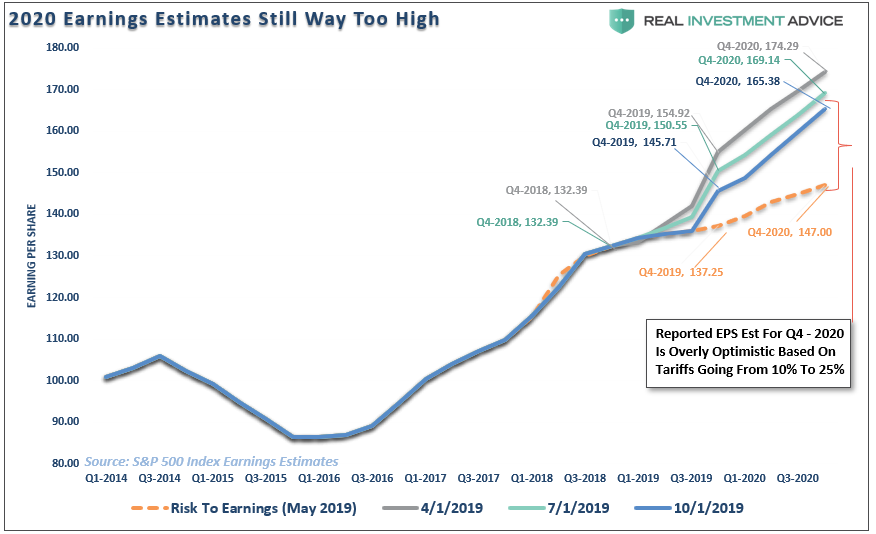

Lastly, given the economic weakness, as noted above, is going to continue to depress forward reported earnings estimates. As I noted back in May, estimates going into 2020 have already started to markedly decline (primarily so companies can play “beat the estimate game,”)

(Click on image to enlarge)

For Q4-2020, estimates have already fallen by almost $10 per share since April, yet the S&P 500 is still near record highs.

As we discussed in this past weekend’s newsletter, it all comes down to “hope.”

“Investors are hoping a string of disappointing economic data, including manufacturing woes and a slowdown in job creation in the private sector, could spur a rate cut. Federal funds futures show traders are betting on the central bank lowering its benchmark short-term interest rate two more times by year-end, according to the CME Group — a welcome antidote to broad economic uncertainty.” – WSJ

Hope for:

- A trade deal…please

- More Fed rate cuts

- More QE

The reality, of course, is that as investors chase asset prices higher, the need to “rationalize,” a byproduct of the “Fear Of Missing Out,” overtakes “logic.”

As we also discussed this past weekend, the backdrop required for the Fed to successfully deploy “Quantitative Easing” doesn’t exist currently.

“The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, and confidence is extremely negative.

In other words, there is nowhere to go but up.

Such was the case in 2009. The extremely negative environment that existed, particularly in the asset markets, provided a fertile starting point for monetary interventions. Today, the backdrop could not be more diametrically opposed.”

If we are correct, investors who are dependent on QE and rate cuts to continue to support markets could be at risk of a sudden downturn. This is because the entire premise is based on the assumption that everyone continues to act in the same manner.This was a point we discussed in the Stability/Instability Paradox:

“With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the ‘instability of stability’ is now the most significant risk.

The ‘stability/instability paradox’ assumes that all players are rational and such rationality implies an avoidance of complete destruction. In other words, all players will act rationally, and no one will push ‘the big red button.’”

Simply, the Fed is dependent on “everyone acting rationally.”

Unfortunately, that has never been the case.

The behavioral biases of individuals is one of the most serious risks facing the Fed. Throughout history, the Fed’s actions have repeatedly led to negative outcomes despite the best of intentions.

(Click on image to enlarge)

This time is unlikely to be different.

Over the next several weeks, or even months, the markets can certainly extend the current deviations from long-term means even further. Such is the nature of every bull market peak, and bubble, throughout history as the seeming impervious advance lures the last of the stock market “holdouts” back into the markets.

The correction over the last couple of months has done little to correct these extensions, and valuations have become more expensive as earnings have declined.

Yes,. the bullish trend remains clearly intact for now, but all “bull markets” end….always.

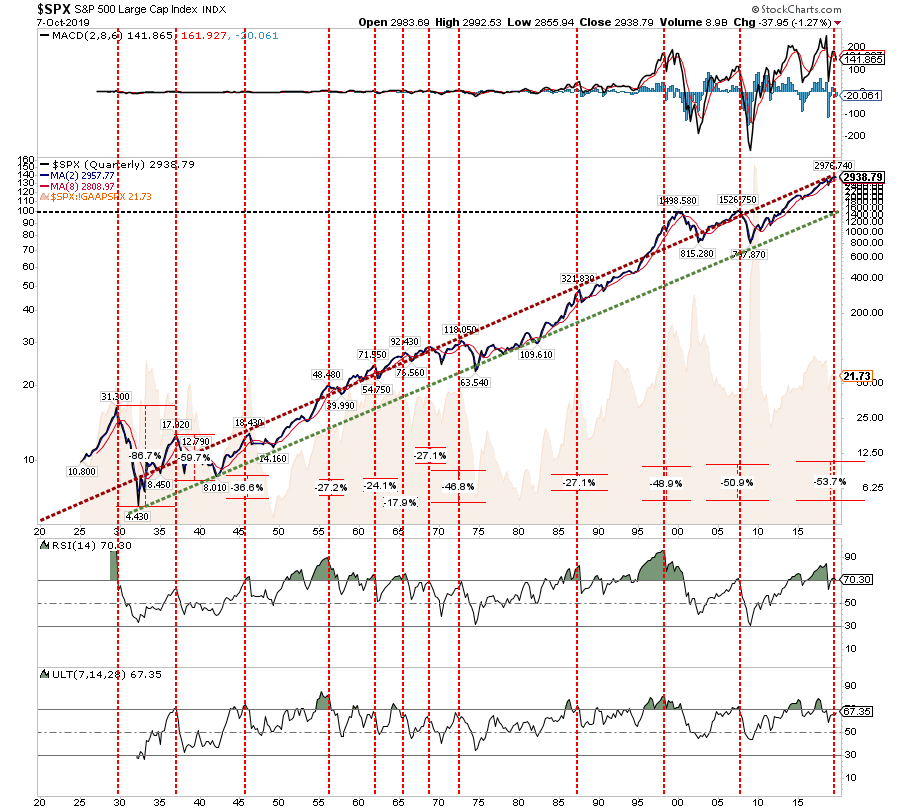

Given that “prices are bound by the laws of physics,” the chart below lays out the potential of the next reversion.

(Click on image to enlarge)

This chart is NOT meant to “scare you.”

It is meant to make you think.

While prices can certainly seem to defy the law of gravity in the short-term, the subsequent reversion from extremes has repeatedly led to catastrophic losses for investors who disregard the risk.

There are substantial reasons to be pessimistic about the markets longer-term. Economic growth, excessive monetary interventions, earnings, valuations, etc. all suggest that future returns will be substantially lower than those seen over the last eight years. Bullish exuberance has erased the memories of the last two major bear markets and replaced it with “hope” that somehow, “this time will be different.”

Maybe it will be.

Probably, it won’t be.

The Reason To Focus On Risk

Our job as investors is to navigate the waters within which we currently sail, not the waters we think we will sail in later. Higherer returns are generated from the management of “risks” rather than the attempt to create returns by chasing markets. That philosophy was well defined by Robert Rubin, former Secretary of the Treasury, when he said;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty.Second, every decision, as a consequence, is a matter of weighing probabilities.Third, despite uncertainty, we must decide and we must act.And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecast. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

“A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions.It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.”

We must be able to recognize, and be responsive to, changes in underlying market dynamics if they change for the worse and be aware of the risks that are inherent in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes which is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

Just something to consider.

Disclaimer: Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with more than $800 million under management. As a team of certified and ...

more