Tariffs Whipsaw Markets As Retailers Are Set To Report On Q1 Results

Equities bounced back on Tuesday after a 2%+ loss on Monday, as trade talks still appear in play between the two largest economies. But the rally fizzled in the final hour of closing as the major averages lost some of their vigor. Nonetheless, Jim Cramer said Tuesday that the stock market saw a “genuine rally, and that is a bullish sign.”

“The good news ... is that typically on day three of a sell-off, you only get a smattering of brave souls coming in at the end of the session to do some buying. Today wasn’t like that,” the “Mad Money” host said. “Today was much broader than that ... Even Boeing saw its stock run, as did Caterpillar, although both were very oversold.

"Without some new trash-talking tweet from the president saying the trade talks are off, or some retaliation from China, that we haven’t thought about."

With the trade skirmish temperature now elevated investors are found hoping that the next $325bn in tariffs aren’t levied on China’s imports to the United States. This last batch of tariffs is where the greatest pain would come from and what would be found to hit the massive retail and consumer goods sectors of the U.S. economy according to most economists and analysts. As such, many market participants are moved to watch what develops by way of the late June meeting between President Trump and President Xi at the G-20 Summit.

At the previous G-20 summit in Argentina last December, the two leaders agreed on a 90-day trade ceasefire that put their tariff war on hold for months, until last week. Max Baucus said the upcoming U.S. presidential election in 2020 will also be a factor in the ongoing trade negotiations.

“I frankly wonder, it’s very possible that President Trump will strike a deal before 2020. That will especially happen if the stock market is going south because he likes a solid stock market,” said Baucus, who is also a former U.S. democratic senator from Montana.

“But Trump is caught “in a bit of a box” as “he doesn’t want to appear weak. If he appears weak, he will be criticized by the democratic presidential nominee and other democrats, so he’s in a bit of a box. In particular, the public nature of the trade dispute has made a resolution more difficult. This very public approach has put both countries in a very difficult position because it’s very hard to back down now. China wants to do business with the United States. China wants a deal, but China wants a deal that China can live with.”

The reality of the ongoing trade negotiations is that where there was once rising hope for a trade deal, this has been replaced by rising doubts for a trade deal. If there is a crowd of voters you don’t want to disappoint here in the United States, it’s investors as they vote more directly and in accordance with their perceived views of the stock market. For months, these “voters” have been told, “ A deal is close-at-hand, China wants a deal, a framework for a deal is being constructed, we see a deal by May or June”. Such rhetoric has been smashed with the recently raised tariffs, more heated tweets and retaliatory tariffs from China on U.S. imports to the region. Furthermore, Axios suggests the latest actions taken by both signs is the result of a deal not being close-at-hand whatsoever, as they’ve been told by White House officials.

Senior administration officials tell Axios that a trade deal with China isn't close and that the U.S. could be in for a long trade war. A senior administration official said the differences between the two sides are so profound that, based on his read of the situation, he can't see the fight getting resolved before the end of the year.

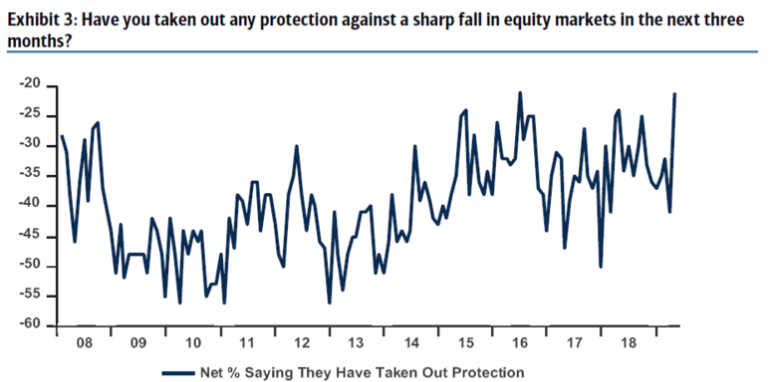

If this, in fact, the reality as described by Axios, which is increasingly likely based on recent breakdowns of the trade truce, investors are finding themselves in a dangerous position. A such, they’ve taken to protectionist measures themselves. Bank of America Merrill Lynch latest fund manager survey suggests widespread investor protection has been bought of late and under the premise that an all-out trade war could put pressure on equities near-term.

The investment bank’s latest monthly survey of global fund managers found that 34% of investors say they have secured downside protection against a big decline in the equity market over the next three months. That represents the highest level ever in the history of the survey, chief investment strategist Michael Hartnett said.

“No trade deal means post-Fund Manager Survey investor mood has soured significantly,” Hartnett said in Tuesday’s note to clients. “Longs in US stocks, EM, discretionary, tech, banks [are] all threatened if key technical levels cannot hold this week.”

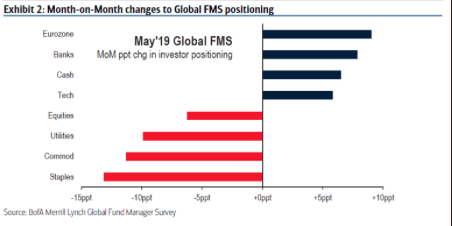

Moreover, traders reduced their exposure to equities compared to the April survey and removed their underweight position in eurozone and banking stocks and added to tech shares by reducing exposure to bond proxies and commodities.

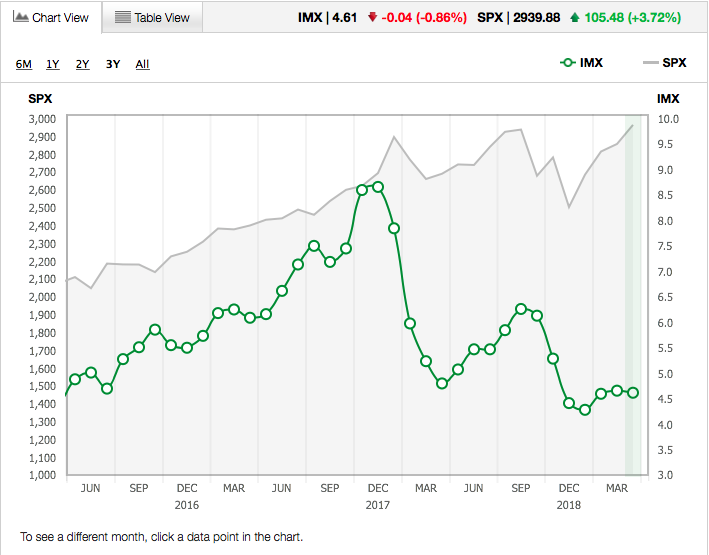

And if you think retail investors are left holding the proverbial bag of equities, think again. According to the TD-Ameritrade Investor Movement Index, exposure to equity markets decreased among TD-Ameritrade clients during the April IMX period. The IMX decreased by 0.86%, down 0.04 from the previous period, to 4.61.

TD Ameritrade clients were net buyers overall during the period but favored less risky assets. Clients were net sellers of equities and favored buying of products with reduced risk, including fixed income. This rotation out of equities and into fixed income pushed the IMX to a score of 4.61.

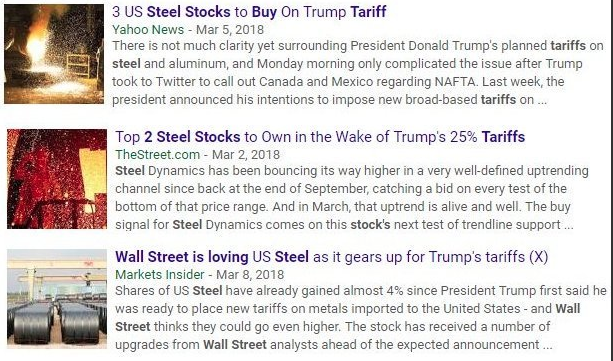

Nobody wins in a trade war and everyone loses as tariffs have little more effect than exacting a tax on corporations and consumers. Recall when the steel and aluminum taxes went into place in 2018? Something tells me U.S. Steel (X) can’t forget the first mention of the tariffs, which were eventually levied.

And the analysts and media suggested buying steel and aluminum companies of course! So much for that.

So what’s on deck, EU auto tariffs! That’s been the threat or warning in place for nearly a year, as put forth by the White House Administration. The president had threatened that he would slap a 25% tariff on car imports from the European Union. So far, however, the tariffs have not been imposed, but Trump is due to make a decision on European auto imports by May 18, this Saturday.

David Hauner, head of cross-asset strategy and economics for Europe, the Middle East, and Africa at Bank of America Merrill Lynch, believes the dispute is a strategy by the U.S. to increase its share of agricultural goods imported by the EU, from the United States.

“We think there will at least be an attempt by the U.S. to push for some sort of concessions from Europe. It’s gonna be very difficult particularly if Trump actually starts a discussion about agriculture.

Some say that car tariffs might ... be a Trojan horse to actually start discussions about agriculture, because that’s where really the big business for the U.S. and Europe would be. Agriculture and Europe is politically very very sensitive when it comes to allowing American imports.”

Farmers have seen their fortunes suffering from the trade war with China, and that’s potentially a concern for the president ahead of his 2020 re-election bid.

According to the Office of the United States Trade Representative, U.S. imports for consumed agricultural products from EU countries totaled $23.9 billion in 2018, while U.S. agricultural goods exports to the EU was $13.5 billion.

Auto imports from EU countries were worth $56.4 billion. Overall, the U.S. goods trade deficit with EU countries was $169.3 billion in 2018, an 11.8% increase over 2017, according to the USTR.

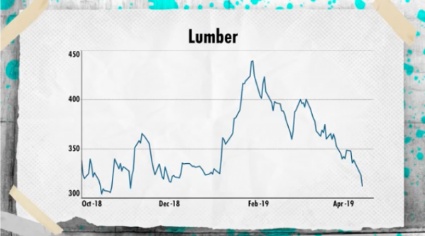

As it proved to be with the implementation of steel and aluminum tariffs if auto tariffs are implemented, why would investors anticipate any positive effects for the likes of Ford (F) or General Motors (GM)? Hence all the protection being purchased of late by investors. Nobody wins in a trade war; tariffs are taxes. Still, don’t believe us? How about those lumber tariffs implemented in 2018?

Finom Group (for whom I am employed) highlighted this issue recently, given the rise of Michael Gayed’s recent call for a decline of 40% for the S&P 500. Gayed points to the 45% collapse in lumber prices over the last several months as a sign the economy is slipping into a recession and the market will follow.

Gayed attempts to avoid the understanding that tariffs created the artificial rise in lumber prices in his Real Vision YouTube video. Finom Group debunks his irrational thought process in its State of the Markets video, which analyzed the Pension Partner’s thesis for a 40% collapse in the S&P 500.

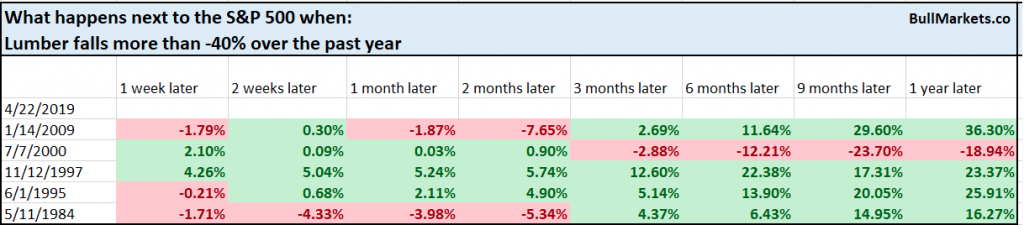

Troy Bombardia of Bullmarkets.co also aimed to look into the Michael Gayed thesis surrounding lumber price declines with new studies.

“Lumber prices soared after the tariffs were placed on lumber imports. Like the bump right now in imports (companies front-running tariffs), such a spike is unsustainable and is bound to fall.

Using a low sample size and recency bias, bears can point out “over the past 30 years, the only other time lumber was down more than -45% was January 2001!”

If we relax the parameters even a little bit (from -45% to -40%), we can see that a lumber crash isn’t consistently bearish for stocks.

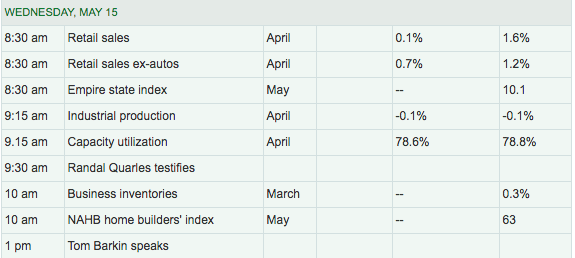

Always do your research folks, don’t take what the pundits say at face value, expand those charts and dig into the fundamentals that are producing those charts. There is always a reason why a chart appears and depicts what it depicts. With that being said, there’s a slew of data to discover today and as we pivot away from the geopolitical risks.

Retail sales are expected to be the highlight of the economic data released today. After a strong retail sales release for the month of March, investors are hoping to see the momentum carried forward through the month of April. Unfortunately, the YoY results may not prove as easy a comparison although the expectations for MoM are seemingly subdued. Economists polled by MarketWatch expect a modest .1% rise in monthly retail sales when reported ahead of the opening bell.

Among 18 services industries surveyed, retail is the only one projecting sales will fall this year, an Institute for Supply Management report shows. The U.S. Department of Commerce releases its April retail sales figures on Wednesday, and they’re expected to show a slower gain than March. The National Retail Federation already forecast in February that sales growth will slow in 2019, especially as the benefits of tax cuts fade and the trade war with China threatens to erode Americans’ appetite for shopping.

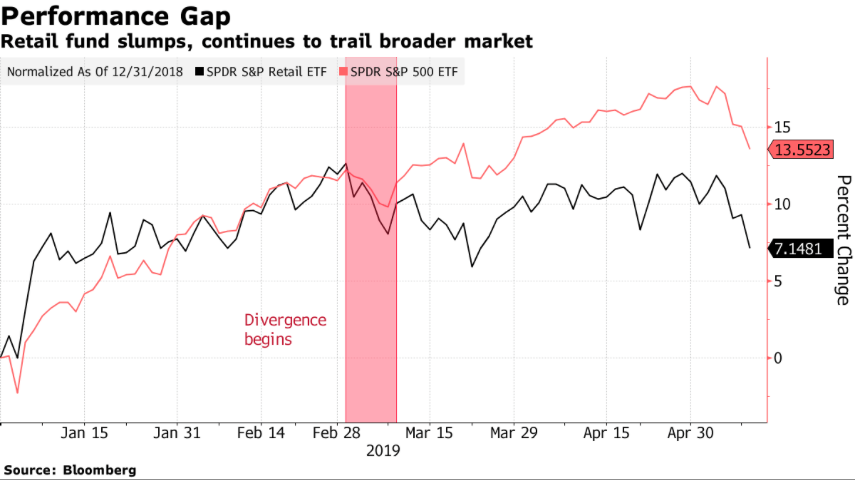

“Major retailers account for close to 20% of U.S. imports from China, and with President Trump’s administration raising tariffs on some $200 billion in Chinese goods to 25% on Friday, it could completely wipe out earnings growth across the sector, according to Evercore ISI.”

The retailers most exposed to higher Chinese tariffs include Best Buy (BBY), since many electronics are sourced in China with long lead times and few other options; Target, due to the increasing number of private-brand goods made abroad; and Bed Bath & Beyond Inc. (BBBY) and other sellers of home goods with minimal ability to boost prices. Generally speaking, the more food a retailer sells, the more insulated it is, but that doesn’t mean big grocers like Wal-Mart (WMT) and Kroger Co. (KR) are totally immune.

And then there’s the weather. While investors hate hearing about the weather-related impact on quarterly results, as it pertains to retailers it does play a significant role in their quarterly performance. This past February in the U.S. was the coldest in 9 years and the second wettest in 125 years, according to Telsey Advisory Group. Things improved by April, but analysts say it might not be enough to offset the unpleasant earlier weeks in the quarter. Also, look for retailers to say that the second quarter is also off to a bad start weather-wise, as this month is trending colder so far and companies are lapping the warmest May on record in 2018. A later Easter may have also pushed some sales out of the first quarter and into the second, depending on when retailers set their calendars.

As we can’t steer clear of the tariff discussion given the possibility of another $325bn in tariffs to be levied near-term, analysts will notably seek out retailers’ take on the subject. We would expect for every retailer to answer this question from the analysts’ participating on individual quarterly conference calls. Macy’s (M) is the first major national chain set to report results.

According to Benzinga, Macy's earnings will be near 33 cents per share on sales of $5.52 billion, according to analysts. Macy's EPS in the same period a year ago totaled 48 cents. Sales were $5.54 billion. If the company were to match the consensus estimate, earnings would be down 31.25 percent. Sales would be down 0.38% from the same quarter last year.

Macy’s sales are right where they were in 2009, proving the business model is in dire straights despite all the implemented initiatives over the last decade. Department stores have all seen a mass move from consumers into the online retail-shopping arena. Try as they may to offset such shifts in consumer behaviors, the scalable solutions for department stores are lacking. And Macy’s stock price has suffered greatly, even as they have developed a formidable omni-channel presence with online sales growing double-digits for many years now.

As shown in the chart above, Macy's has been below a "death cross" since Dec. 3, when the 50-day simple moving average fell below the 200-day simple moving average, indicating that lower prices would follow. On Dec. 4, investors could have reduced holdings at the 200-day simple moving average at $34.10, which was a perfect setup before the mall anchor issued a warning on Jan. 10, which is shown on the chart as a huge price gap lower.

Yours truly warned investors about shares of M after the retailer posted results last quarter. In the following TD Network Live interview, I discussed the headwinds the retailer has faced and will continue to face in the years to come.

I was short shares of M through the latest quarter and has since covered its short position after achieving its desired downside price target objective. It remains to be seen just how Macy’s answers the questions surrounding tariffs and future growth prospects, as investors cling to the high dividend with hopes of a turnaround. The retailer continues its “shrink to grow” strategy that may bear fruit in the interim but has never in the history of big-box retailing proven to resurrect a retailer’s fortune. Just ask Sears Holdings (SHLD) CEO, Eddie Lampert.

As the retail reporting season is set to take place over the next couple of weeks, investors will remain on high-alert for trade headlines. In the meantime, I will be trading what the market delivers in the way of opportunistic trade alerts. Yesterday’s trade found my UVXY short trade covered for a quick profit as depicted below. (Finom Group trade alert via private Twitter feed)

We’ll see what’s in store for the market’s today as investors continue to seek out the safety of bonds!