Tariffs, Inversions, Debt, Brexit... Oh My!

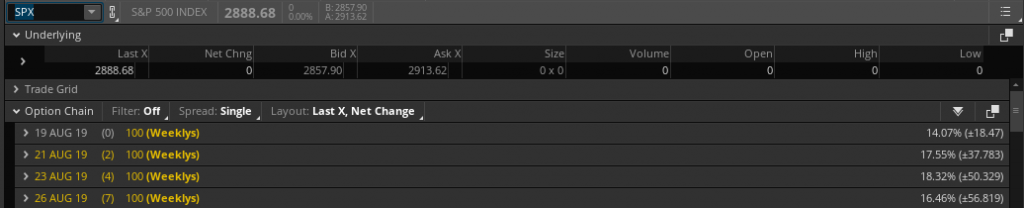

Ya'll ready for another rip roaring week in the markets? After some wild daily swings in the previous trading week, the S&P 500 (SPX) ultimately decline just over 1% while also greatly exceeding the weekly expected move for a 4th consecutive week.

Alongside the wild, roller-coaster ride last week, the VIX only managed to move roughly 3% for the week. Kind of interesting giving the week also included a 3% drop, on Wednesday, for the S&P 500 and peer indices. With the VIX rising, the weekly expected move for the trading week ahead has moved up slightly to $58/points.

As we look forward to the opening bell on Monday, equity futures are pointing sharply higher. The reason for the momentum from Friday's rally and into Monday morning comes on the heels of China vowing to lower loan rates. The People’s Bank of China (PBOC) said it will improve the mechanism used to establish the loan prime rate (LPR) from this month, in a move to further lower real interest rates for companies as part of broader market reforms.

Analysts say the move, which came after data that showed weaker than expected growth in July and followed a cabinet announcement on Friday, underscores the government’s attempts to use reforms to support a slowing economy.

“By reforming and improving the formation mechanism of LPR, we will be able to use market-based reform methods to help lower real lending rates,” the PBOC said in a statement published on its website.

Goldman Sachs is quick to point out that the new system itself doesn’t guarantee the actual lending rate will be lower. This depends on whether the OMO rates become lower, liquidity conditions and government window guidance. But given the current situation with weak activity growth, heightened trade war risks and a strong desire by the senior leadership to lower rates, we do expect actual lending rates to go down.

Naturally, the news that the PBOC was set to lower borrowing costs sent Asian markets into rally mode overnight. European markets are rallying in kind and global bonds are finally selling-off with yields moving higher.

What has also given rise to renewed equity market optimism on Monday was headlines that suggested the U.S. Commerce Dept. was set to extend licenses to Huawei. According to Reuters, the U.S. Commerce Department is expected to extend a reprieve given to Huawei Technologies that permits the Chinese firm to buy supplies from U.S. companies so that it can service existing customers, two sources familiar with the situation said.

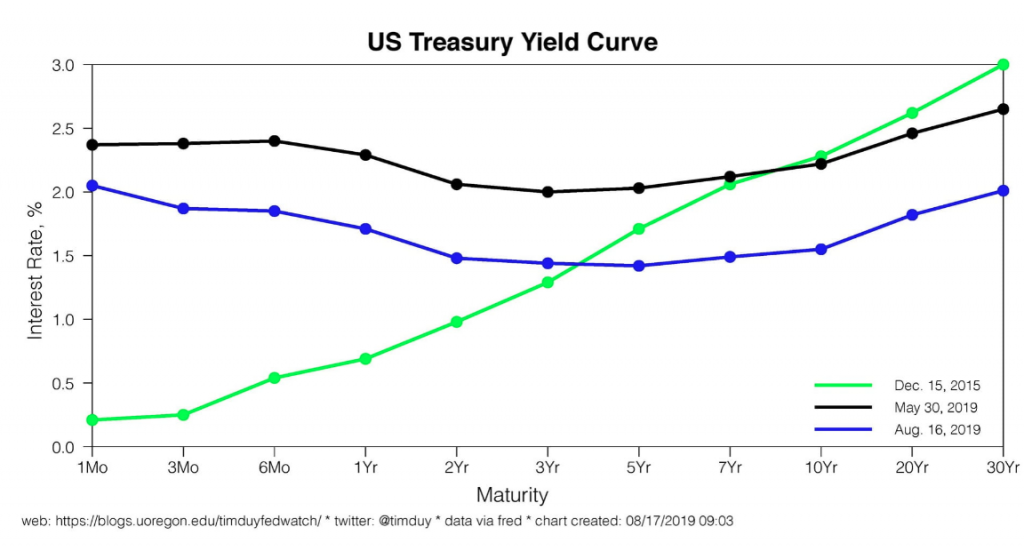

If one chose to step away from the market headlines over the weekend, we couldn't say that we would have blamed them for doing so. The bond market and yield curve were all the craze over the weekend, grabbing headline after headline. This even as the 2s/10s Treasury bonds inverted for all of 5 hours before un-inverting and now steepening on Monday morning to nearly 9 bps. But before we dwell on the yield curve inversion any further, let's take a brief look at where we are in the S&P 500 from a technical perspective and see what Bank of America Merrill Lynch’s Stephen Suttmeier says is heading the benchmark indexes way near-term.

"The S&P 500 needs to fall another 5% and panic needs to get more extreme. The correction is going to continue. You take a measured move of this trading pattern — one leg down, one leg up. It’s gets you right down into that 2,750-2,740 range.”

Suttmeier estimates it’ll take weeks for stocks to find a floor, especially since the volatility is coming during the worst seasonal period of the year: August through October.

“We have plenty of resistance,” he said. “We continue to stall right around this 2,940 level on the S&P.”

Suttemeier’s second chart reflects fear in the market through the 25-day put/call ratio, which follows put volume relative to call volume. According to Suttmeier, panic isn’t widespread enough for stocks bottom.

“Once you get above one in the 25-day put/call ratio, you can see this S&P bottom. And, that happens probably sometime in September,” said Suttmeier. “We had fearful readings to start June. June was an up month, and we came into August very complacent.”

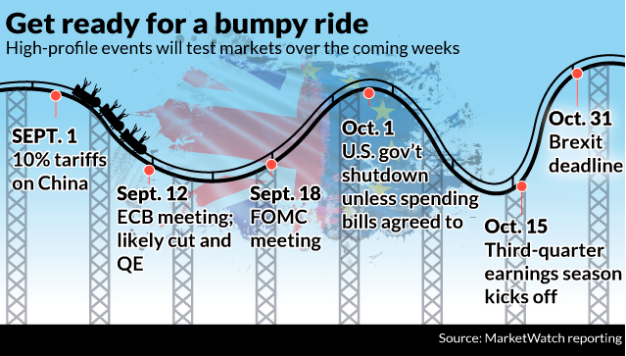

The economic data calendar is pretty light this week, highlighted by Fed minutes on Wednesday and Jackson Hole kicking off on Friday. There was a bit of a quiet period from Fed officials leading up to the Jackson Hole event, but investors are now expecting to hear something out of the FOMC regarding future rate cuts at some point over the coming weekend. Here is what several firms are suggesting about the Jackson Hole event this weekend:

- "No doubt, the risk is high that Fed commentary this week could disappoint the markets by not signaling clearly enough that additional rate cuts are coming.” - Wells Fargo

- "We don't think that the Fed will provide much new information on either front. Jackson Hole is an academic conference and not the appropriate forum to announce a change in policy.” - TD

- “Given the July decision, when the cut was only 25bps and Powell seemed unable to lead the FOMC to a bigger cut, the risk of any speech disappointing market expectations for dovishness is high.” - UBS

- "Hopes are emerging that next week’s symposium will spawn creativity because Europe and Japan require it, but without fiscal or structural commitments, it might be hard to translate Wyoming’s policy papers into transformational policy and market reversals.” - JPM

- “…we expect [Powell] to sound dovish, indicating the Fed is willing and ready to provide accommodation as necessary to support the expansion.” - Citi

- “...we expect Chair Powell (Aug 23.) to indicate that downside risks related to domestic manufacturing and global growth alongside elevated trade tensions remain skewed toward less favorable outcomes.” - Barclays

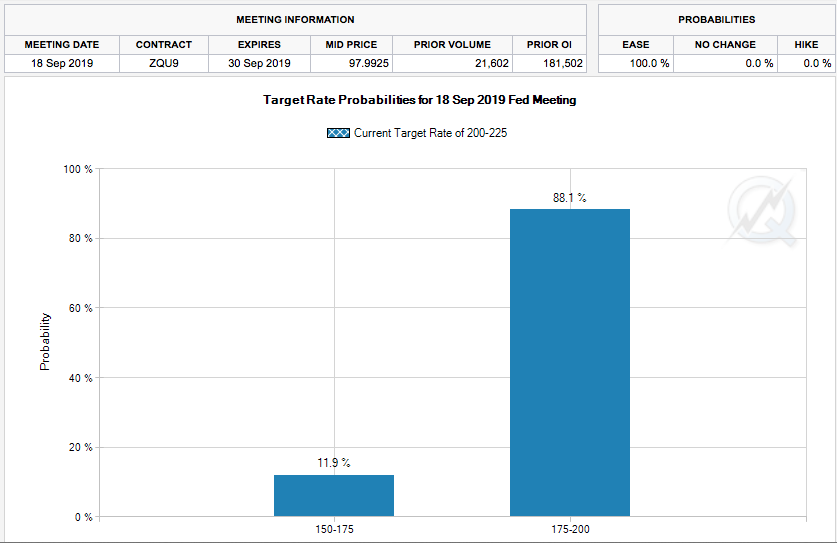

As it pertains to those widely anticipated rate cuts going forward, the Fed is very, very likely to cut rates in September given the issues surrounding the potential signals from the bond yield curve.

Here is what Fed Watcher Tim Duy offered over the weekend, discussing the likelihood of the Fed to cut rates at the September meeting and rationale for doing so:

"The Fed is going to cut interest rates in September, even if they as of yet don’t want to admit it. That said, I don’t think they have a unified framework to justify and explain a rate cut and the lack of such a framework makes for a challenging communications situation.One description of Powell’s last press conference was that the rate cut was dressed-up in a “coat of many colors” to gain consensus for the action. It would be helpful for Powell to provide a more consistent policy vision with this week’s speech, “Challenges for Monetary Policy.”

As of last Friday, 30-year treasury rates were less than 1-month rates. That’s not exactly a healthy look for an economy that is supposedly “solid.” Not that the bond markets had much good news to begin with; the 3m10s inversion intensified this week and the 2s10s spread even briefly inverted. In my opinion these things are warning signs that monetary policy is too tight and will eventually crimp economic growth severely.

The basic story would be that the Fed wants to sustain the current near-trend pace of growth and to do so they need to ensure that policy is not restrictive. But falling U.S. interest rates consistent with slowing global growth, low global interest rates, low inflation, and business confidence uncertainty, indicate that the neutral rate of interest, at least in the short-term, has fallen. This in turn leaves U.S. policy rates too high and likely even restrictive. You won’t see this in the data today, which reflects the level of monetary accommodation 6-12 months ago. You will see it, however, in 6-12 months unless the Fed adjusts policy rates accordingly. Hence, the Fed needs cutting interest rates in the months ahead to ensure that policy is sufficiently accommodative to sustain the expansion. Absent such accommodation, the economy will be excessively vulnerable to negative shocks such as trade policy uncertainty.

Bottom Line: The Fed will need to cut rates next month even if they don’t yet know it. The faster they coalesce around the need for multiple rate cuts, the more likely it is that they will steer the economy away from recession.

Certainly, we'd like the ability to invest and manage our portfolios with a bit less emphasis on central bank involvement, but that's just not the way of the markets since the Great Financial Crisis. The Quantitative Easing programs installed and maintained for several years thereafter the GFC have enforced the greater central banks' involvement for the foreseeable future. Something I've said at the onset of QE was quite simple and factual, "No economy of scale has ever entered a cycle of QE without it ending... or ending with bankruptcy." And just because QE officially ended a few years ago and a QT cycle commenced, that' doesn't mean QE ever ended. In fact, QT is just another phase of QE. Look how long QT lasted, and, how quickly we've begotten talks of a return to QE around the globe.

It seems like each passing week there are a great many events to pay attention to, either regarding the domestic or the global economy. The U.S. economy is holding up better than most of its peers, central banks around the world are cutting interest rates, and the consumer is lifting some economies from falling into a recession.

Event risks are likely to remain with investors and the markets through the remainder of the year. Nonetheless, many analysts and strategists are suggesting it is wise to stay invested. In this environment of headline-driven markets, you'll simply have to take a break from the headlines and turn of the business news channels that aim to sensationalize the macro issues of the day and week.

“I wouldn’t be surprised if the second half of the year isn’t characterized by a very, very powerful combination of very loose monetary policy and accelerating growth,” Peter Berezin, chief strategist at BCA Research said. “Central banks are usually reacting to yesterday’s news and monetary policy comes with a lag. That is just a wonderful environment for stocks.”

“If trade tensions continue to escalate and Trump follows through with the 10% tariffs on $300 billion of additional Chinese imports beginning September 1, the economy’s growth engine is likely to downshift considerably,” warned Oxford Economics’ senior economist Bob Schwarz, in a note Friday.

“Either importers would have to absorb the higher tariffs and accept lower profits, which is unlikely, or pass them on to consumers, which would crimp demand.”

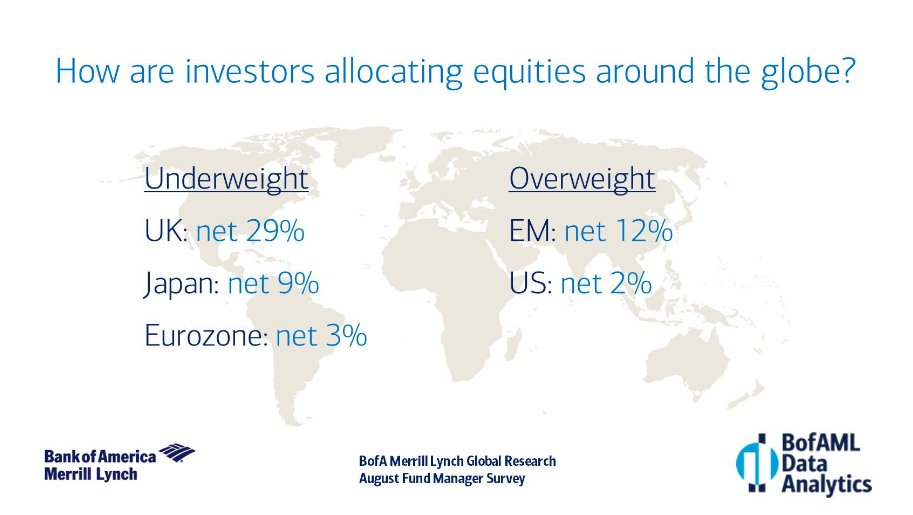

Unfortunately, it seems as though many investors continue to allow event risks and headlines drive their equity market participation. The reality is that the economy is still growing around 2% and earnings are also still forecasted to grow 1-4% in 2019. Nonetheless, according to the latest BofAML fund manager survey, investors continue to deleverage risk. In this month’s Fund Manager Survey, investors’ allocation to global equities fell 12ppt to net 22% underweight; regional allocations vary.

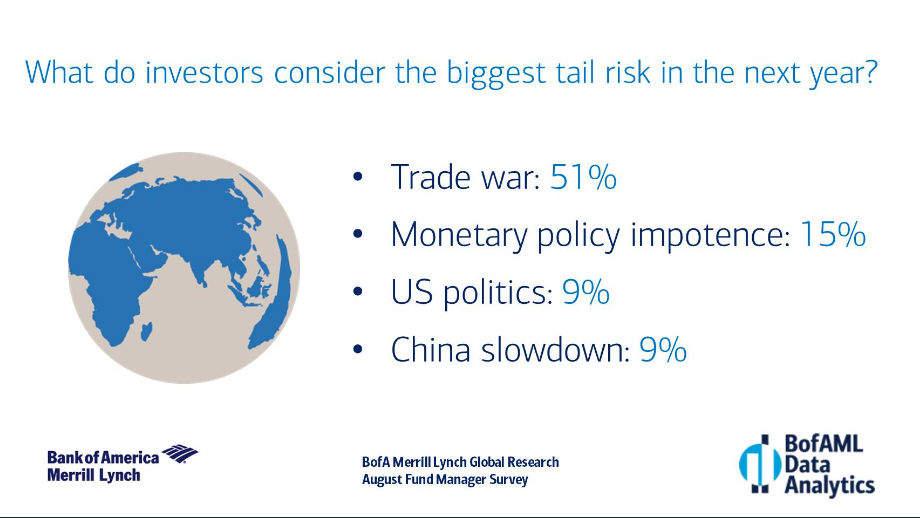

The reality is that there is so much we could worry about on any given day, but trade issues continue to be the largest driver of anxiety amongst investors given the seemingly irrational outbursts on the trade and tariff situation that is now more than a year old.

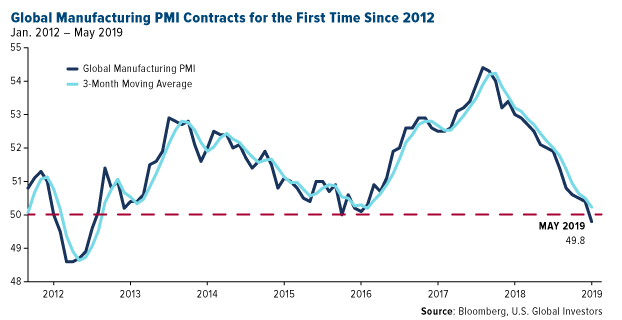

The trade dispute has resulted in global manufacturing spiraling into contraction. It's the one issue of concern, trade, that finds investors unified. Perhaps surprising no one, global manufacturing is now in contraction mode for the first time since 2012. That’s according to the most recent reading of the sector’s health, the purchasing manager’s index (PMI), which headed lower for a record 13th straight month in May. The PMI posted 49.8, down from 50.4 a month earlier. As a reminder, anything above 50.0 indicates expansion; anything below, contraction.

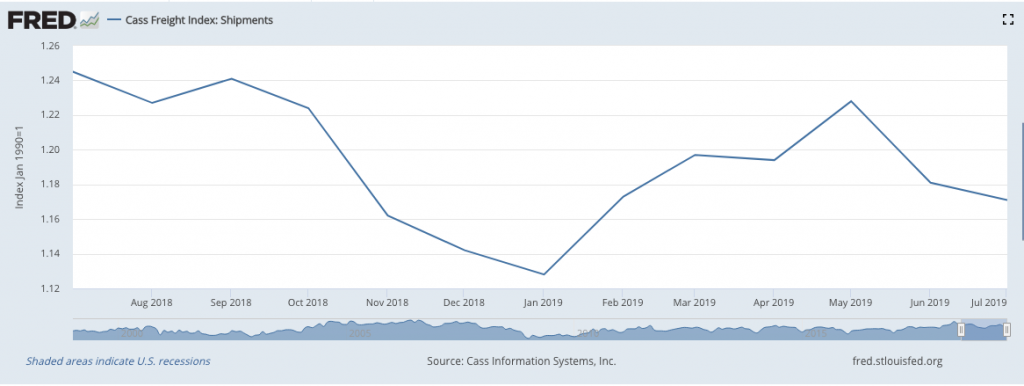

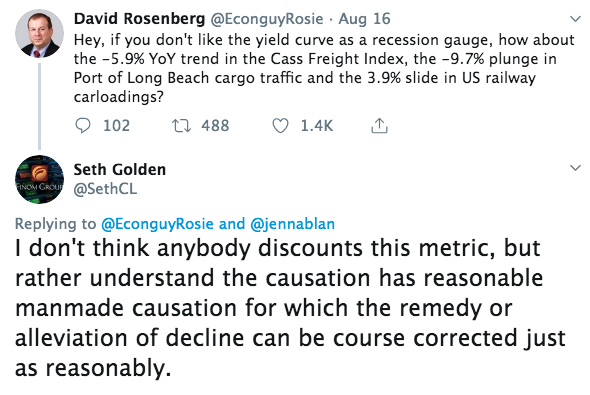

As global manufacturing has fallen, it's proven difficult on the rails, trucking and freight industries. We've seen YoY rail and freight falling as the trade issues continue to weigh on business sentiment around the world. The most recent Cass Freight index reading highlights the both waning manufacturing and business sentiment.

The -5.9% YoY trend in the Cass Freight Index can also be pared with the -9.7% plunge in Port of Long Beach cargo traffic and the 3.9% slide in U.S. railway carloadings, something gleefully pointed out by one of the biggest permabears on Wall Street, David Rosenberg.

The good news in these regards is that the issues surrounding global trade, manufacturing, rails and freight are largely manmade crisis/issues. Just as man created them, they can be found satisfied and remedied for the betterment of the global economy, by man.

Fortunately, the U.S. has reduced its reliance on manufacturing over the last 50 years such that the consumer is the largest portion of economic activity. But what if the consumer falters under the weight of the trade war and its greater impact on the global economy? That's the question that remains front and center, even with continued strength in retail sales domestically.

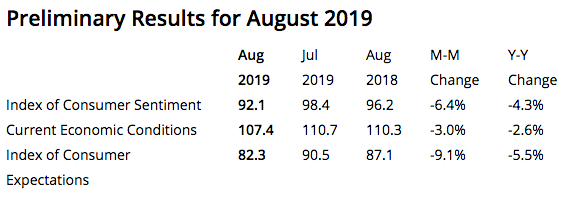

The economy doesn't JUST run on the back of the consumer, but consumer confidence! The consumer has to feel confident about their job and future outlook in order to spend and give back into the economy that feeds the economic cycle. That confidence is measured by a variety of different firms and in a variety of different ways. The latest consumer sentiment survey fell to 92.1 this month from 98.4 in July, according to a preliminary reading from the University of Michigan. Economists surveyed by MarketWatch had forecast a reading of 96.8. Just a year and a half ago, the index touched 101.4 to mark the highest level since 2004.

Monetary and trade policies have heightened consumer uncertainty—but not pessimism—about their future financial prospects. Consumers strongly reacted to the proposed September increase in tariffs on Chinese imports, spontaneously cited by 33% of all consumers in early August, barely below the recent peak of 37%. Although the announced delay until Christmas postpones its negative impact on consumer prices, it still raises concerns about future price increases.

In rounding out today's Daily Market Dispatch I urge investors and active traders to remain focus on the long-term outlook for the U.S. economy and corporate earnings, which move together over time. But in the time being, central bank easing and trade feuds will grab headlines. The toll that trade feuds have taken on the business community are apparent but have yet to curb consumer activity. Hopefully, that is maintained, but the business community is certainly becoming beleaguered by the seemingly never-ending headlines and flare ups.

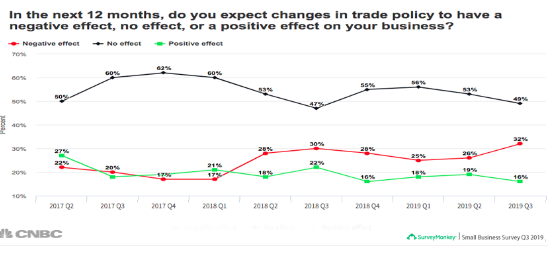

Small business confidence has dropped to a level not seen since 2017, matching the all-time low since CNBC and SurveyMonkey began taking the pulse of Main Street in a quarterly survey three years ago.

Business confidence is now lower than it was amid the major stock market sell-off of late 2018 and equals the way entrepreneurs feWlt in late 2017 when the tax cuts package and its provisions for small business owners were in doubt. The reason this time: President Donald Trump’s trade policy.

Over half of business owners in the CNBC|SurveyMonkey Small Business Survey for the third quarter of 2019 say that business conditions are good. That number was 13 percentage points lower (55% vs. 44%) at the time of the 2017 low. Fifty-eight percent say they expect revenue to increase in the next 12 months, and Trump’s net approval rating is holding strong, at 57%.

“Trade has become the new issue causing volatility for small business owners, as a growing number of small business owners say they expect trade policy to have a negative effect on their business in the next year,” said Laura Wronski, senior research scientist at SurveyMonkey.

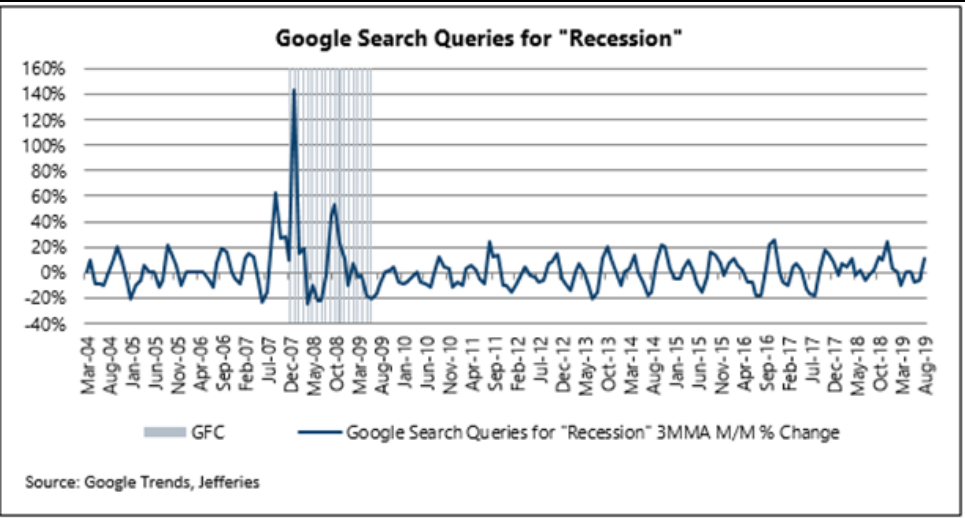

With all that being said, done and done, let's hope to find some of the sensationalistic media headlines surrounding recession risks and the yield curve abating. We may already be seeing it through our ole friend Google. The three-week moving average for “recession” searches on google are up over the last month, but very range-bound.

In fact, they have been range-bound since after the financial crisis and currently sits nowhere near the volume of searches seen pre-financial crisis. But you wouldn't know this absent the YoY chart above and simply by reading headlines. Stay nimble and with a clear mind out there traders and investors!