Stock Buybacks Aren’t Bad, Just Misused & Abused

I remember in the late 90’s and early 2000’s that I would get regular phone calls and emails asking me about a widely owned equity. The conversation almost always went like this:

“Now that XYZ company is trading at $XX/share do you think they will split the stock soon? They have often done so in the past whenever the price reached this level.”

It was a valid question as companies way back then often split shares for to increase share counts for mergers and acquisitions, lower the price for market participation, and for executive compensation plans.

However, following the financial crisis stock splits disappeared and a new trend emerged – share repurchases. Like stock splits, share repurchases in and of themselves are not necessarily a bad thing, it is just the least best use of cash. Instead of using cash to expand production, increase sales, acquire competitors, or buy into new products or services, the cash is used to simply reduce outstanding share count by removing some shareholders from the pool. Here is a simple example:

- Company A earns $1 / share and there are 10 / shares outstanding.

- Earnings Per Share (EPS) = $0.10/share.

- Company A uses all of its cash to buy back 5 shares of stock.

- Next year, Company A earns $0.20/share ($1 / 5 shares)

- Stock price rises because EPS jumped by 100%.

- However, since the company used all of its cash to buy back the shares, they had nothing left to grow their business.

- The next year Company A still earns $1/share and EPS remains at $0.20/share.

- Stock price falls because of 0% growth over the year.

This is a bit of an extreme example but shows the point that share repurchases have a very limited, one-time effect, on the company. This is why once a company engages in share repurchases they are inevitably trapped into continuing to repurchase shares to keep asset prices elevated. This diverts the ever-increasing amount of cash from more productive investments.

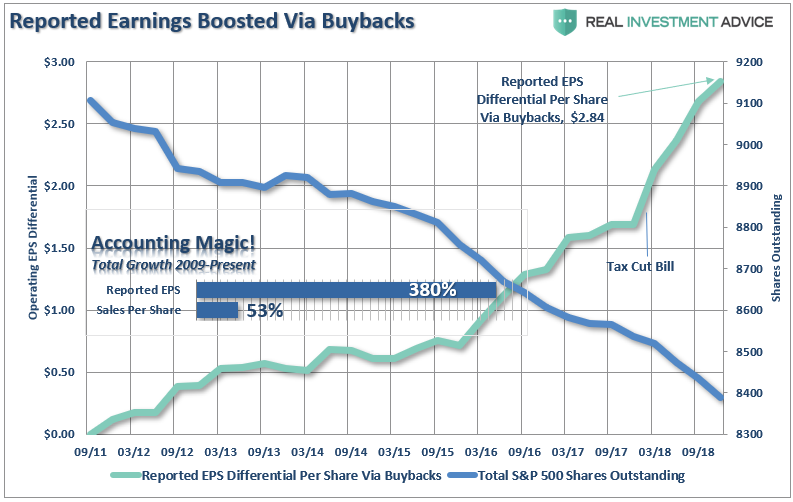

As shown in the chart below, the share count of public corporations has dropped sharply over the last decade as companies scramble to shore up bottom line earnings to beat Wall Street estimates against a backdrop of a slowly growing economy and sales.

(The chart below shows the differential added per share via stock backs. It also shows the cumulative growth in EPS and Revenue/Share since 2011)

(Click on image to enlarge)

The Abuse & Misuse

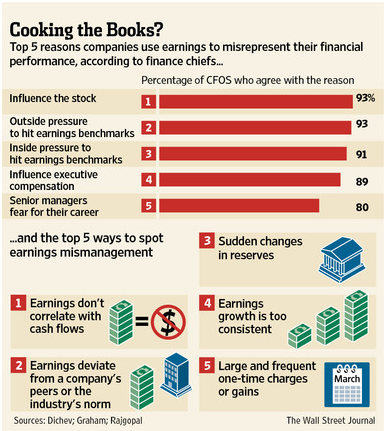

As I stated, share repurchases aren’t necessarily a bad thing. It is just the misuse and abuse of them which becomes problematic. It’s not just share repurchases though. In “4-Tools To Beat The Wall Street Estimate Game” we discussed how companies not only use stock repurchases, but a variety of other accounting gimmicks to “meet their numbers.”

“The tricks are well-known: A difficult quarter can be made easier by releasing reserves set aside for a rainy day or recognizing revenues before sales are made, while a good quarter is often the time to hide a big ‘restructuring charge’ that would otherwise stand out like a sore thumb.

What is more surprising though is CFOs’ belief that these practices leave a significant mark on companies’ reported profits and losses. When asked about the magnitude of the earnings misrepresentation, the study’s respondents said it was around 10% of earnings per share.“

(Click on image to enlarge)

The reason that companies do this is simple: stock-based compensation. Today, more than ever, many corporate executives have a large percentage of their compensation tied to company stock performance. A “miss” of Wall Street expectations can lead to a large penalty in the companies stock price.

As shown in the table above, it is not surprising to see that 93% of the respondents pointed to “influence on stock price” and “outside pressure” as the reason for manipulating earnings figures.

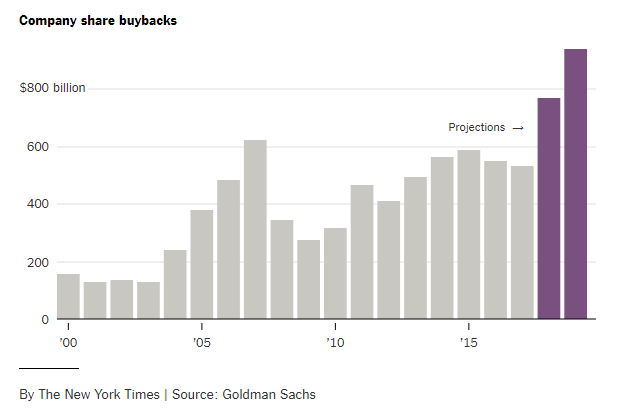

The use of stock buybacks has continued to rise in recent years and literally went off the charts following the passage of tax cuts in 2017. As I wrote in early 2018. while it was widely believed that tax cuts would lead to rising capital investment, higher wages, and economic growth, it went exactly where we expected it would. To wit:

“Not surprisingly, our guess that corporations would utilize the benefits of “tax cuts” to boost bottom line earnings rather than increase wages has turned out to be true. As noted by Axios, in just the first two months of this year companies have already announced over $173 BILLION in stock buybacks. This is ‘financial engineering gone mad'”

Share buybacks are expected to hit another new record by the end of 2019.

(Click on image to enlarge)

“Share repurchases aren’t bad. It is simply the company returning money to shareholders.”

There is a problem with that statement.

Share buybacks only return money to those individuals who sell their stock. This is an open market transaction so if Apple (AAPL) buys back some of their outstanding stock, the only people who receive any capital are those who sold their shares.

So, who are the ones mostly selling their shares?

As noted above, it’s the insiders, of course, as changes in compensation structures since the turn of the century has become heavily dependent on stock-based compensation. Insiders regularly liquidate shares which were “given” to them as part of their overall compensation structure to convert them into actual wealth. As the Financial Times recently penned:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

A recent report on a study by the Securities & Exchange Commission found the same:

- SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks, Yahoo Finance reports.

What is clear, is that the misuse and abuse of share buybacks to manipulate earnings and reward insiders has become problematic. As John Authers recently pointed out:

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.

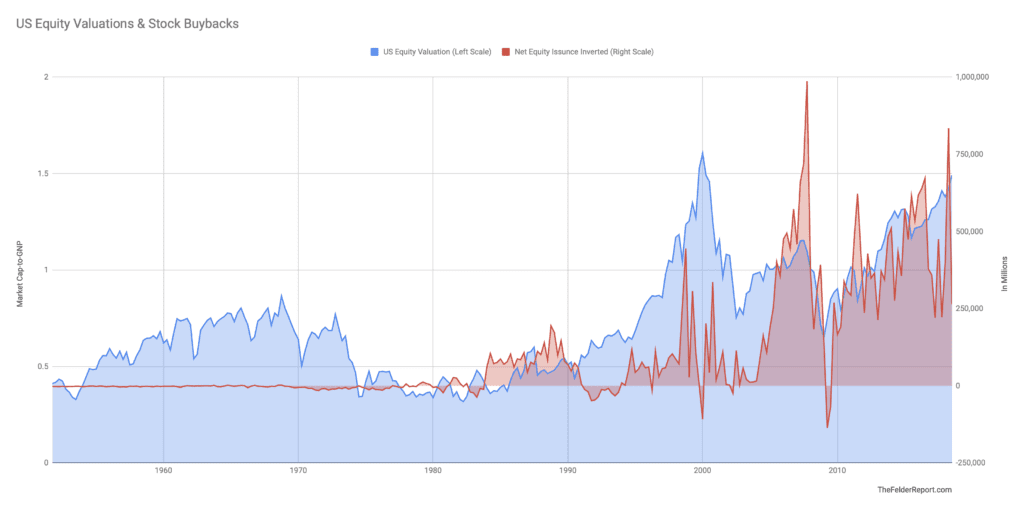

As Jesse Felder wrote:

“Without that $4 trillion in stock buybacks and in a market where trading volume has been falling for decades they never would have been able to soar as high as they have. The chart below plots ‘The Buffett Yardstick’ (total equity market capitalization relative to gross national product) against total net equity issuance (inverted). Since the late-1990’s both valuations and buybacks have been near record highs. Is this just a coincidence? I think it’s safe to say it’s not.”

(Click on image to enlarge)

“Harvard Business Review recently noted there is a statistical relationship between equity-based pay and buyback activity: ‘We find that the more vesting equity the CEO has in a given quarter, the higher the likelihood is of both buybacks and M&A. Like investment cuts, buybacks and M&A could be good rather than bad — but we find that vesting equity leads to the bad type.’

In addition, the Roosevelt Institute found another curious statistic: ‘In the first 8 days after a buyback announcement, insiders sell an average of $500,000 worth of stock per day—a five-fold increase as compared to the normal daily average of $100,000.’ So the history of buybacks over the past several decades show that they are implemented when executives would most benefit from juicing the stock price and they take full advantage by selling heavily back to their own company.”

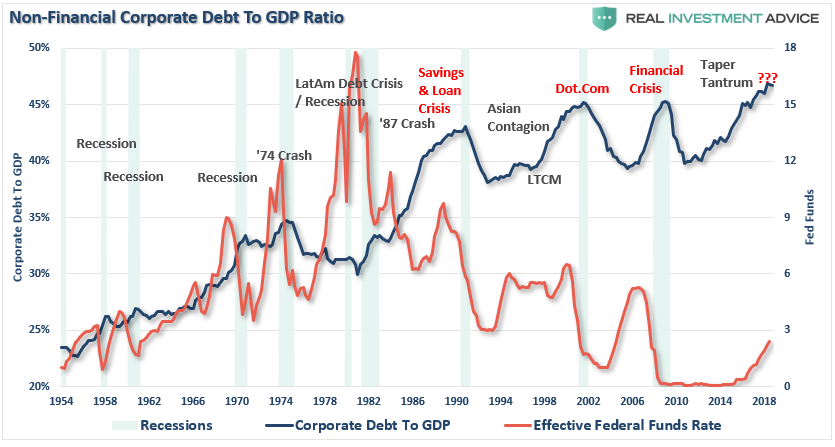

The other problem with the share repurchases is that is has been done through leverage. The ongoing suppression of interest rates by the Federal Reserve led to an explosion of debt held by corporations. Much of the debt was not used for mergers, acquisitions or capital expenditures but for the funding of share repurchases and dividend issuance.

(Click on image to enlarge)

As Michael Lebowitz noted:

While the financial media cheers buybacks and the SEC, the enabler of such abuse idly watches, we continue to harp on the topic. It is vital, not only for investors but the public at-large, to understand the tremendous harm already caused by buybacks and the potential for further harm down the road. Unfortunately, COP is not an isolated case. Hess Oil, for instance, just sold 25 million shares at $39 per share to improve their capital position. Sadly for Hess shareholders, many of whom likely supported buybacks, this shareholder dilution was unnecessary had Hess not bought nearly 63 million shares at a price of nearly $60 per share in the 3 years prior. Money that could have been spent spurring future growth for the benefit of investors was instead wasted only benefitting senior executives paid on the basis of fallacious earnings-per-share.

As stock prices fall, companies that performed un-economic buybacks are now finding themselves with financial losses on their hands, more debt on their balance sheets, and fewer opportunities to grow in the future. Equally disturbing, many CEO’s like James Mulva, who sanctioned buybacks, are much wealthier and unaccountable for their actions.

This article may be best summed up with the closing to our first article on buybacks.

Fraud – frôd/ noun:

Wrongful or criminal deception intended to result in financial or personal gain.