Reality Versus Market Agitprop: Did Everyone Really Turn Bearish On Wednesday?

I was going to leave well enough alone on Friday when it comes to whether the technical selloff on Wednesday and its less dramatic sequel on Thursday together presage something ominous into year-end.

But reader feedback over the last few hours suggests an appetite for “more cowbell” (as it were) and I can certainly understand why folks might be feeling a bit anxious about the outlook, especially given the fact that market participants are now more attune than ever to the risks posed by liquidity vacuums and, relatedly, forced de-risking from systematic/programmatic strats.

On Friday afternoon, JPMorgan’s Marko Kolanovic – the market’s go-to guy when it comes to assessing the impact of technical flows – released a short, straightforward note that suggested ~70% of the technical unwind was in the books. You can read some excerpts from his note here.

Obviously, opinions are going to vary on whether we’ll get some aftershocks from the Wednesday/Thursday rout and in his piece, Marko does caution that slower-moving vol.-targeting strats are likely to de-risk further over the coming days. But one key point is this:

Flows that may counter selling are buybacks, fundamental buyers attracted by cheap valuation (P/E below historical average), as well as fixed weight portfolio rebalances (e.g. pensions rebalancing on triggers).

While systematic flows are an increasingly important part of the overall market narrative, other things matter too, and don’t forget that buybacks remain the largest source of U.S. equity demand.

There seems to be some misinformation circulating on Friday afternoon.

Three readers have asked whether it’s true that banks have materially altered their constructive view on the S&P into year-end based at least in part on what happened this week. I’m not sure where that idea originated, but the answer is “no”. As far as I can tell, nobody is throwing in the towel on 2018 based on two days of technical selling pressure.

Allow me to elaborate using a series of examples that should definitively shoot down any misinformation you might have been fed on Friday.

On Thursday, we cited some excerpts from a note penned by Nomura’s Charlie McElligott who said that on Nomura’s estimates, CTAs de-risked in equities to the tune of some $88 billion on Wednesday. Here are the actual bullet points from a section in his Thursday note called “Cumulative flow numbers across options greeks and systematic CTA in SPX futures”:

- CTA levels from here—2719 break would see further reduction down to just “9% Long” and would trigger an additional selling of $57B S&P futures

- From the perspective of MUCH slower-moving Risk-Parity (using a 2Y window), the change on global bond vol continues to generate a negligible selling-down in U.S. Equities at just a -$600mm of SPX deleveraging yesterday from Risk-Parity per our model

- SPX and NDX optionspositioning is serious, with SPX net Delta move -$459.2B at a 0.1%ile move since 2013 (was only -$55.4B the day prior)

- SPX Gamma now at $24.2B per 1% move with 2800 and 2750 lines mattering the most

- QQQ positioning walloped, net Delta hits -$32.7B (which is 0%ile net delta since 2013 (and was -$14.1B the day prior)

- QQQ Gamma actually cut in half down to $489mm per 1% move with most of the delta at 180 / 170 / 175 strike

Ok, so again, that was Thursday morning, after the Wednesday rout.

You might be asking yourself whether McElligott is among those who have purportedly become newly “bearish” after this week. The answer to that would be “no”. In fact, the title of his Friday note is: “Making the case for the equities long into year-end.”

Among the factors McElligott cites when making the bullish case for stocks through the end of the year are cleaner positioning after this week’s wash out, buybacks and seasonality. All of those factors were cited by the above-mentioned Kolanovic in his Friday note.

(McElligott’s visuals on seasonality for October 12-November 12 /Nomura)

How about Goldman? On Friday morning, the bank’s Rocky Fishman analyzed Wednesday in the historical context and while he did note that fragility events are happening at a rate that is perhaps disconcerting (he doesn’t use that term, but that’s the gist of it), he also explicitly noted that the reason Wednesday looked so black-swan-ish (if you will), is because Q3 2018 was among “the five least-volatile quarters for the S&P over the past 20 years.”

So is Goldman bearish? Or, to address a rumor that’s apparently circulating, has the bank now suckered enough “retail” clients into buying what the prop desk is selling and is thus free to tell the supposedly “ugly” truth about the S&P into year end?

Hardly.

Here is the title of Goldman’s weekly kickstart note out Friday evening:

“Rotations beneath the surface indicate recent price action has been exacerbated by an unwind of popular positions”, the bank writes, adding that “despite the recent sell-off, equity fundamentals are strong and we remain constructive on the path of the S&P 500. Our year-end 2018 S&P 500 target remains 2850.”

If you read the excerpts posted here from Kolanovic’s Friday note, you might recall that he mentions the buyback blackout doesn’t apply across the board. Specifically, Marko cited ASR programs that aren’t subject to blackouts.

Well, guess what? Goldman’s buyback desk had its biggest day since February on Wednesday and can you guess why? I’ll give you a hint:

Although Corporates remain in the earnings blackout period until 11/6, a lot of companies are on 10b5-1 plans which allow them to buy back stocks through the blackout windows. Many of these plans include scales which get more aggressive the lower stocks go.

What about Barclays’ Maneesh Deshpande? Is he bearish, as some people seem to think? In two words: Not really.

It’s true that on October 11 (so, Thursday), Deshpande suggested that more systematic selling might be in the cards. Specifically, he said the following:

The dramatic spike in equity volatility is likely to drive further systematic selling from Volatility Control Funds. We estimate that the AUM in the Volatility control/Targeting strategies is ~$355Bn. These funds decrease their overall leverage to maintain fixed portfolio volatility. Since the forecasted volatility increases during market declines, these funds sell risky assets that would exacerbate the selloff.

Until the past week the allocation… was 100% to equities. With the sell-off the allocation has been reduced to ~65%. We expect further systematic selling to the tune of ~$130Bn from these funds to reduce allocation to equities over the next couple of days.

That is of course just another way of saying what Kolanovic said on Friday, which, again, is that vol.-targeters will likely be selling over the next 3-10 days depending on the model.

To be fair, Deshpande does say there could be “a second leg lower” for the overall market, but in a note dated Friday (i.e., a newer note than the one excerpted above), analysts including Deshpande say a sustained flip in the equity-rates correlation (one of the proximate causes for the midweek malaise at least to the extent the fear of a flip in the sign of that correlation spooked folks into selling) is still “some time off.”

Just to drive the point home about Barclays not being overtly bearish, here is what they say about the outlook in the same Friday note:

On February 7, we took the view that the increase in volatility would be very short lived. The volatility calmed down swiftly in the subsequent weeks. The current episode looks again very similar (probably catalysed by the FED language in conjunction with current 10Y rate levels) and we would again expect the turmoil to be short lived.

You’re also reminded that back in August, Barclays actually tweaked their S&P model in order to avoid cutting their year-end target. Here is the only screengrab you need:

Maybe Maneesh has changed his year-end target in light of this week, but as far as I can tell, that 3,000 target remains in place despite his call for further near-term de-risking from vol.-sensitive strats.

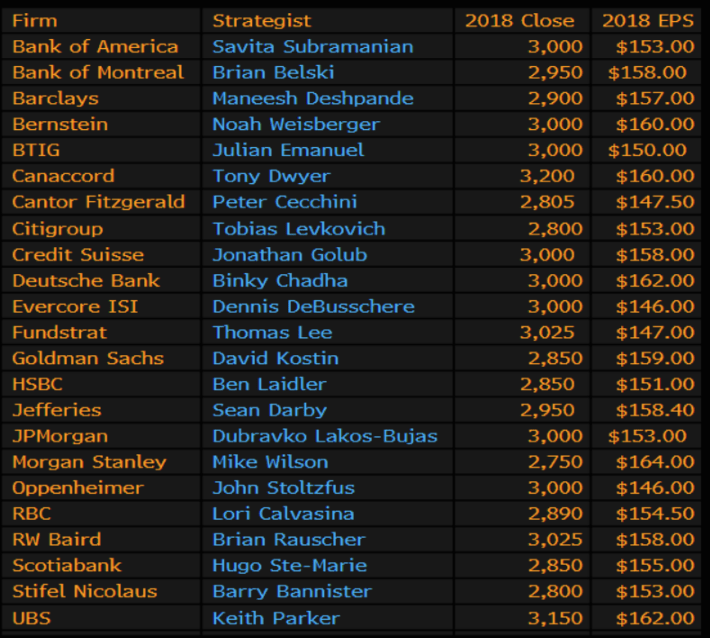

Incidentally, that 3,000 year-end target is the same as JPMorgan’s year-end S&P target and if you’re wondering what the Street in general thinks, you can find a complete rundown below (and please do let me know if you see anybody who seems like they’re panicking):

(Bloomberg)

Now you could very well say that all of these people are wrong, and lord knows you’d be right to suggest that Wall Street isn’t always Johnny-on-the-spot when it comes to getting out ahead of egregious drawdowns.

But that kind of begs the question on Friday, because the whole point here is to dispense with the notion that there’s been some kind of epochal shift in the Street’s opinion vis-à-vis the outlook for U.S. equities in light of what happened on Wednesday/Thursday.

Again (because I feel like I need to make this as clear as absolutely possible), I am not expressing my own opinion here about where U.S. equities go into year-end. Regular readers know I’m unabashedly skeptical about a market that leans heavily on handful of high-flyers and seems increasingly predisposed to suffering the type of fragility events that occurred on Wednesday.

I’m also a big believer in Howard Marks’ “perpetual motion machine” characterization of the current dynamic and how “the logic that says it will work forever always collapses” (to quote Howard’s classic “There They Go Again – Again” memo).

That said, I think it’s important that folks don’t get so wrapped up in pushing their own narrative about markets that they find themselves distorting other people’s analysis or maligning anyone who isn’t perpetually foisting doomsday predictions on the investing public.

That’s why, on Friday evening, I wanted to take a few minutes to i) dispel the notion that Wall Street turned overtly bearish this week and ii) dispense with the idea that somehow Marko Kolanovic is the only one who is constructive. As you can see from the above, pretty much everyone is still relatively upbeat.

Oh, and as far as Friday is concerned, Marko said this at 12:41 PM ET:

For instance, if the market were to hold its gains during the day, it could result in a squeeze higher by end of the day from gamma hedging flows.

Here’s what happened next:

Nothing further.

Disclosure: None of what I write here is to be construed as advice to buy or sell any kind of asset. It is merely my personal and not my professional opinion. Any asset can go to zero.