The Fed minutes have allowed rates markets to rally further, ahead of the US holiday. The focus now shifts to the European Central Bank minutes, which could also deliver dovish headlines.

We think EUR rates hold the most upside in the near term.

Dovish Fed minutes extend market rally, likely to the dismay of officials

Markets got the dovish headlines out of the Federal Open Market Committee minutes they needed to rally further – a “substantial majority” judged that slowing the pace of hikes “would soon be appropriate”. Together with the dismal PMI readings earlier in the session this has helped put a brake to the curve flattening, though, as the front to intermediate maturities caught up.

The overall takeaway looks more nuanced, and not too different than what could be gleaned from recent official statements about the general rate trajectory – “various” Fed officials did see rates peaking at a higher level than previously thought. In their discussion officials also noted that the full effect of tightening financial conditions would take longer to feed through to inflation, though there was great uncertainty about the lags. That itself could well be seen as justifying a slowing pace of further policy tightening after what has been delivered already.

However to the degree that markets are running ahead of themselves and financial conditions have already started to loosen again, it is unlikely this is the broader message the Fed wants to send just yet. While the meeting pre-dates the latest positive surprise in the inflation data, officials since then were quick to note that one CPI reading alone is not yet a trend. Yes the PMIs were bad, but other data is showing more resilience with a clear focus near term on next week's job market data.

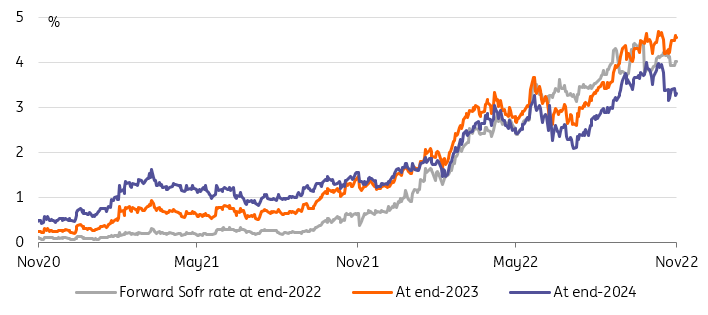

Fed hike discount for 2022 and 2023 has remained stable but more 2024 cuts are now anticipated

Source: Refinitiv, ING

More dovish headline risks from the ECB minutes

The ECB minutes of the October meeting follow hot on the heels of last night's Fed minutes. Here as well the market's main focus is on the pace of rate hikes going forward. The ECB still hiked rates by 75bp last month, but subtle tweaks to the wording of the press statement were already interpreted as a dovish sign. Later background reporting confirmed that the Council was not unanimous on the size of its last hike with three members calling for a smaller hike.

While it was also reported that the Council did not intend to send any specific signal for the size of future rate hikes back then, we could still see some dovish headlines out of the minutes with regards to differing views on the appropriate size of the rate hike. There should also be a more thorough discussion of recessionary risks, even if they should also be balanced by inflationary risks “clearly” on the upside, as Lagarde put it in October’s press briefing.

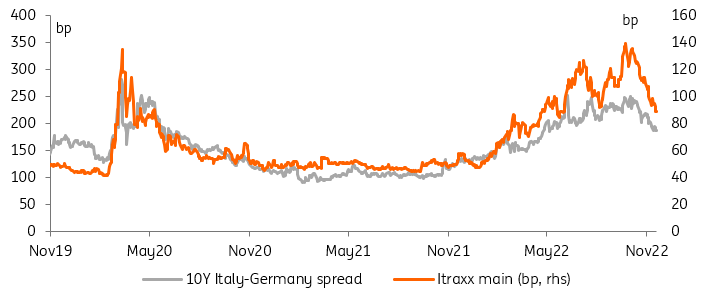

The lack of QT discussion at the October ECB meeting helped to set off a fixed income rally

Source: Refinitiv, ING

Market OIS forwards are pricing c.60bp higher rates for December. This suggests expectations leaning towards a smaller 50bp hike, but the signal is less clear than only a couple of days ago, helped also by less gloomy PMIs just yesterday. Some ECB officials have since suggested there was scope for less aggressive action, such as Italy’s Visco, who is known to lean more dovish. Even some of the better known ECB’s hawks have been less clear on their preference, and their choice between a 50bp or 75bp hike is apparently dependent on the upcoming inflation data, at least Austria’s Holzmann has suggested as much. Only Slovenia’s Vasle was still explicit in saying that the current pace was adequate and would be maintained in December.

However, it remains clear that the ECB is not done hiking. It is this also important to consider what happens beyond December. Smaller hikes are very likely, but the question is for how long. We make out some effort by Chief Economist Lane to direct the discussion away from potentially peaking headline inflation to the more persistent elevation of core inflation. He later also stressed that one should not interconnect quantitative tightening and rate hikes too much, though other officials have strengthened the market’s notion that there could very well be a bargain to be made between the ECB’s hawks and doves, for instance an earlier start to quantitative tightening in return for slower hikes. Going back to the issue at hand – today’s ECB minutes – recall that the clearest dovish signal out of October ECB meeting was actually the absence of a further discussion on QT.

Today's events and market views

Markets will be more eurocentric with US markets heading into today's Thanksgiving holiday and followed by a shortened trading day on Friday. It also means that market liquidity is about to become even thinner than already is. In any case, today's ECB accounts of the October meeting could add to the dovish central bank headlines that have extended the rally in rates yesterday, though less likely the curve flattening we have witnessed until now. In data the German Ifo index follows on the not-as-gloomy-as-expected flash PMI's released yesterday.

If one looks for hawkish risks, then the focus should be on today's ECB speakers, who may well use the opportunity to clarify the message coming out of the ECB accounts. With the ECB's Schnabel we have one of the more influential ECB officials delivering a keynote speech at the Bank of England's watchers conference. That same event has of course also prominent BoE speakers lined up with Ramsden, Hill and Mann.

In secondary markets Italy will reopen two shorter dated bonds for up to €2.75bn.

More By This Author:

U.S. Resilience May Mean The Fed Has To Talk TougherEurozone PMI Remains In Contraction Territory But Inflation Pressures Fade

FX Daily: Glass Half Full

Comments

Log in or sign up to join the conversation.