Political Uncertainty Is A Reminder To Avoid “Home Bias”

Stable laws and competitive markets throughout much of the world go a long way toward providing investors confidence in their ability to size-up potential returns and risks, at least over a longer-term horizon.

The biggest threats to this investment framework are political instability (with global war the most extreme example), a pandemic (think The Black Death that plagued Europe in the 14th century) and famine. All three can be devastating and an economy may be hit by more than one simultaneously. Unfortunately, it is nearly impossible to quantify the risk of these threats.

The best we can do is react to such threats when they present themselves. Presently, political instability is front and center. Nearly every developed economy is dealing with an aging population, slow growth, stagnant wages for lesser-skilled jobs, and mounting levels of fiscal debt. These challenges have led to an increasingly polarized environment in which policies in place may be upended every few years by another election.

The world’s largest market, the United States, has become exhibit A for policy volatility. Take, for example, the country’s health insurance program for low-income households. It was massively expanded by one partisan effort following the 2008 election cycle, and is now under constant threat of being slashed by another partisan push post the 2016 election cycle. These are efforts that have multi-trillion dollar consequences, and it is difficult for anybody to say with confidence what policy will be in place in ten year’s time.

The potential for a trade war between the U.S. and China is simply the latest manifestation of policy uncertainty. We encourage investors to respond to political instability by ensuring their equity holdings are diversified across geographies and free of “home bias”. Our model portfolios are designed with the latitude to allow for higher allocations to foreign developed and emerging markets when appropriate.

Our optimal portfolio for an investor with average risk tolerance includes a 52% allocation to equity, unchanged m/m. The biggest m/m change is a 3 percentage point reduction of short-term bond holdings, funded by higher allocations to intermediate and longer-term bonds. The allocation to TIPS is unchanged m/m.

Optimal Long-Term Asset Allocation for Investor With Average Risk Tolerance

source: ArcPoint Advisor.

Long-Term Equity Market Outlook

Projected Long-Run Annual Real Returns

source: ArcPoint Advisor.

U.S. large-cap equity return projections are slightly higher following a second straight month of stock price declines. The S&P 500 fell 2% in March.

Our forecast for U.S. large-cap equity returns implies average annual mid-cycle earnings of ~$127 for the S&P 500 index companies. This earnings outlook compares to the consensus bottoms-up forecast of ~$158 over the next four quarters for S&P 500 earnings.

Our projected return for small and mid-cap U.S. equity is down slightly m/m following a 1% gain for the Russell 2000 Index in March. We continue to exclude small and mid-cap products from our model portfolios due to our forecast for better returns from larger-cap stocks. This forecast assumes that the historical anomaly of smaller-cap stock outperformance does not persist.

Our model portfolios include a bit more cyclical equity than a month ago due to slightly higher projected returns for U.S. and emerging markets stocks.

But we still continue to favor non-cyclical equity in our model portfolios as there is no return benefit for U.S. cyclical equity and only a modest one for foreign-developed cyclical equity. And much of the remaining premium for foreign-developed cyclical equity is attributable to that sector’s heavier exposure to financials (which adds to the sector’s risk profile).

Difference Between Projected Cyclical and Non-Cyclical Equity Returns

source: ArcPoint Advisor.

The roughly 90 bp premium offered by foreign-developed cyclical equity over U.S. cyclical equity is above the average of 85 bp over the past five years. Our model portfolios continue to modestly favor foreign developed over U.S. cyclical equity, though the preference is smaller than it was to begin 2018.

The premium return offered by emerging market equity has widened again following the recent global stock market correction, and some of model portfolio allocations have flowed from foreign developed stocks into emerging markets.

Cyclical Large-Cap Equity Premia

source: ArcPoint Advisor.

Long-Term Fixed Income Market Outlook

Projected Long-Run Annual Real Returns

source: ArcPoint Advisor.

Projected real fixed-income returns are lower across maturities due to a decline in forward real interest rates. Rates remain above levels at the end of January, but below those experienced following the most recent bout of inflation fear.

The estimated real term premium offered for 10-year U.S. Treasury (UST) bonds is up 4 bp m/m. A 10-year UST note purchased in five years offers 13 bp of additional return over a 52-week UST bill. This level is well below the 10-year average real term premium of 57 bp and reflects the flattening real yield curve.

Risk-Free Real Term Premium

source: ArcPoint Advisor.

The estimated inflation risk premium is effectively zero for a 15-year bond. The inflation premium remains below 20 bp for the 30th consecutive month. We use break-even rates in the U.S. Treasury market to estimate inflation premia. Given the conundrum of no apparent inflation premia despite higher inflation expectations, we also are closing watching the CPI inflation swap market. There too, implied inflation premia are effectively zero.

Inflation Term Premium (15-Year Bond)

source: ArcPoint Advisor.

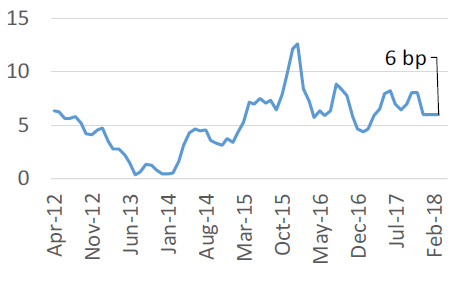

We estimate that investors in investment-grade corporate bonds are receiving ~6 bp of return for every year to maturity as compensation for credit risk, similar to a month ago. The current credit risk premium is consistent with the 5-year average of 5 bp for every year to maturity.

Credit Risk Premium Per Year

source: ArcPoint Advisor.

Disclosure: None.